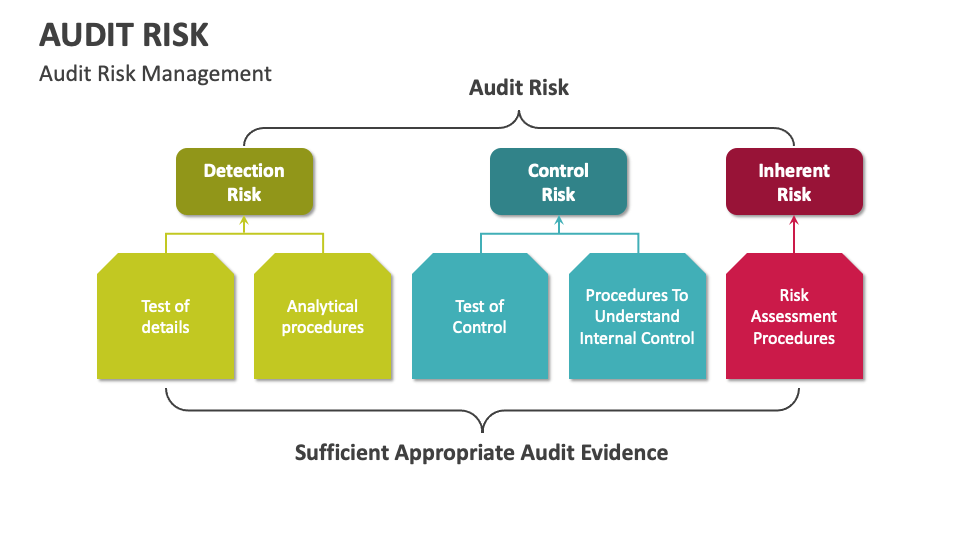

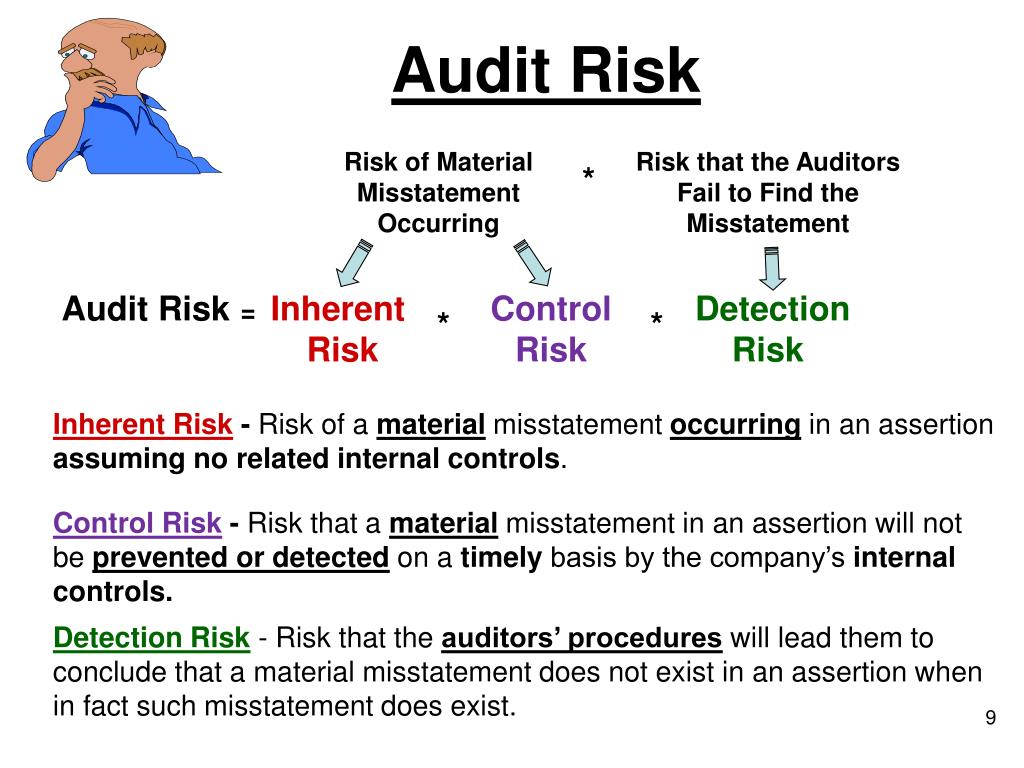

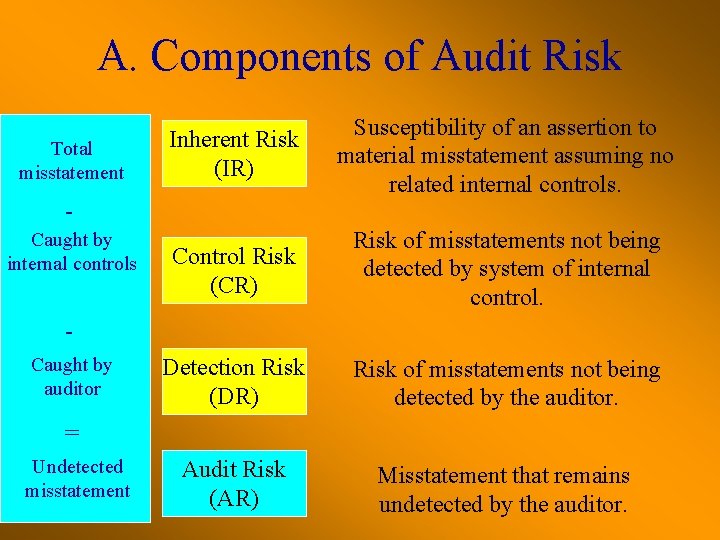

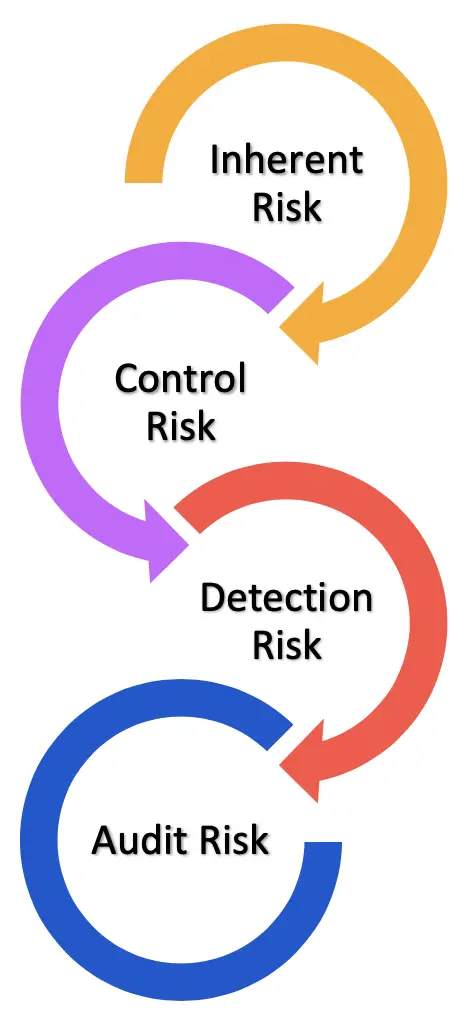

Audit Risk Is Typically Considered And Assessed

Imagine your friend, let's call her Brenda, is famous for her amazing chocolate chip cookies. Everyone raves about them! You, being a supportive friend, decide to "audit" her recipe.

But wait, audit? That sounds scary and serious! Fear not, in Brenda's world it's just a super-friendly fact-checking mission.

The Cookie Calamity: A Tale of Flour, Fear, and Fun

Our mission: ensure Brenda's cookie recipe stays consistent, yielding the same delicious results every time. This is kinda like what happens in the business world.

Must Read

Understanding "Audit Risk" - The Cookie Edition

Now, before we even preheat the oven, we need to think about "audit risk." What's that? In Brenda's case, it's the risk that we might give her recipe a thumbs-up, even if there's something wrong.

Maybe she accidentally used salt instead of sugar one day! Yikes! That's a high audit risk scenario.

Or perhaps, she’s using a secret ingredient (unicorns tears) that she doesn’t want us to know about. Okay, maybe not unicorn tears, but you get the gist.

The Inherent Cookie Chaos

First, there's "inherent risk." This is the risk that exists before we do any checking. With Brenda's cookies, this could be because she's a naturally chaotic baker.

Think flour explosions, spilled milk, and a general disregard for measuring spoons. It's not her fault; she's an artist! But it makes our "audit" a bit trickier.

Maybe her handwritten recipe is smudged and hard to read. Or perhaps she's prone to improvising, adding extra chocolate chips "for good luck." These are inherent risks!

Control Catastrophes!

Next, we look at "control risk." These are the risks that Brenda's own baking habits might fail to prevent errors. Does she double-check her measurements? Does she have a system for making sure she doesn't use expired ingredients? Probably not!

If Brenda doesn't have any real "controls" (like a clear, organized recipe or a habit of tasting the dough before baking), the control risk is high. Which means our audit has to be even more thorough.

Perhaps, she relies on her memory which isn't that great. Or she let her toddler assist with the baking!

Detection Disasters!

Finally, we have "detection risk." This is the risk that we, as the "auditors," might not catch a mistake, even if it exists. Maybe we're too easily swayed by Brenda's charm (and the aroma of freshly baked cookies).

Or maybe we're just too hungry to focus properly! Maybe we sample too many cookies (totally plausible!) and our judgment becomes clouded by sugar.

Even if Brenda's measurements are off, if we don't pay close attention, we might miss it. That's detection risk in action!

Assessing the Cookie Calamity

So, how do we assess all this risk? We ask Brenda lots of questions about her baking process. We observe her in action. And, of course, we taste the cookies. (Quality control, you know!)

We need to figure out just how likely it is that something could go wrong with the recipe. And how big a deal it would be if it did.

A little too much vanilla? No biggie. A whole cup of salt instead of sugar? Cookie Armageddon!

The "Materiality" of Molasses

In auditing-speak, we talk about "materiality." In Brenda's world, this means how much of a difference a mistake would make. A little extra molasses? Probably not material.

But forgetting the eggs entirely? That's a material misstatement! The cookies would be flat, sad puddles of goo.

Materiality is all about impact. Would the mistake change someone's mind about the cookies? Would it make them inedible?

Gathering the Crumbs of Evidence

To reduce our "audit risk," we need to gather evidence. We watch Brenda measure ingredients. We compare her recipe to other chocolate chip cookie recipes online. We even ask her grandma for tips!

We want to be reasonably sure that Brenda's recipe is on the up-and-up. We don't need to be absolutely certain (that would require baking every batch of cookies ourselves for the rest of eternity!).

Reasonable assurance is key! It's like saying, "We're pretty darn confident these cookies are gonna be delicious."

The Grand Finale: A Cookie Audit Success!

After all our investigation, we conclude that Brenda's cookie recipe is, indeed, amazing and consistently produces delicious results. Hooray!

We've successfully navigated the world of "audit risk" and emerged victorious (and slightly sugar-crazed). We helped Brenda ensure that her cookie empire remains strong and tasty.

And best of all, we've learned that even potentially dry topics like audit risk can be made fun and relatable with a little bit of imagination (and a whole lot of cookies!).

Lessons Learned From the Cookie Caper

So, the next time you hear the words "audit risk," don't panic! Just think of Brenda's cookies. Remember that it's all about understanding the potential for things to go wrong, and taking steps to minimize that risk.

And hey, maybe offer your own services as a friendly auditor for a friend's amazing recipe. You might just learn something new (and get to eat some delicious treats in the process!).

Even if it's not cookies, think about auditing other things in your life, like your budget, or your exercise plan. Think about inherent risk, control risk, and detection risk. And always remember to have fun!

Disclaimer: No Actual Audits Were Harmed in the Making of This Article

This article is for illustrative purposes only and should not be taken as professional auditing advice. Real-world audits are far more complex and involve serious responsibility.

But the basic principles are the same: understanding risk, gathering evidence, and making informed judgments. Just, you know, with less cookie dough.

So, go forth and conquer your own audit risks, whether they involve flour, spreadsheets, or anything in between. And remember to always keep a healthy dose of humor handy!

The End (and Time for a Cookie Break!)

We hope you enjoyed this sweet journey through the land of "audit risk." Now, if you'll excuse us, we're off to find Brenda and sample another batch of those amazing chocolate chip cookies.

After all, quality control is a never-ending process! Especially when delicious cookies are involved.

Happy "auditing," everyone!