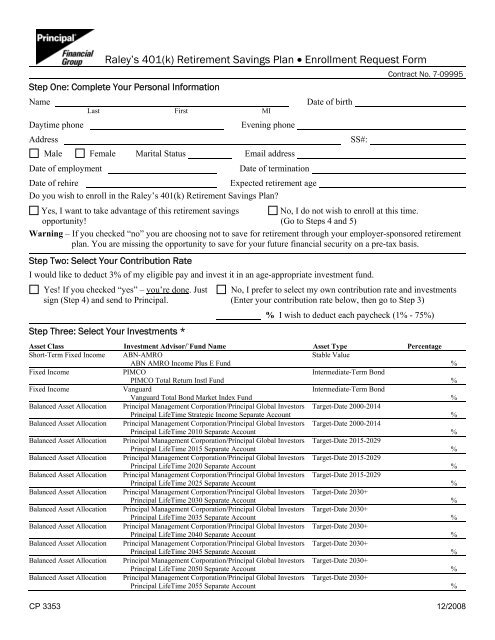

Raley 401k Retirement Savings Plan

So, you're working at Raley's, huh? That means you've probably heard whispers about the Raley's 401(k) Retirement Savings Plan. But what is it, really? Besides, like, the key to early retirement (maybe?). Let's spill the beans, shall we?

Think of it as your personal, super-powered savings account... but for the really long haul. We're talking about those golden years, the ones where you're sipping margaritas on a beach somewhere, hopefully not remembering what a "price check on aisle five" sounds like.

What's the Deal with This 401(k)?

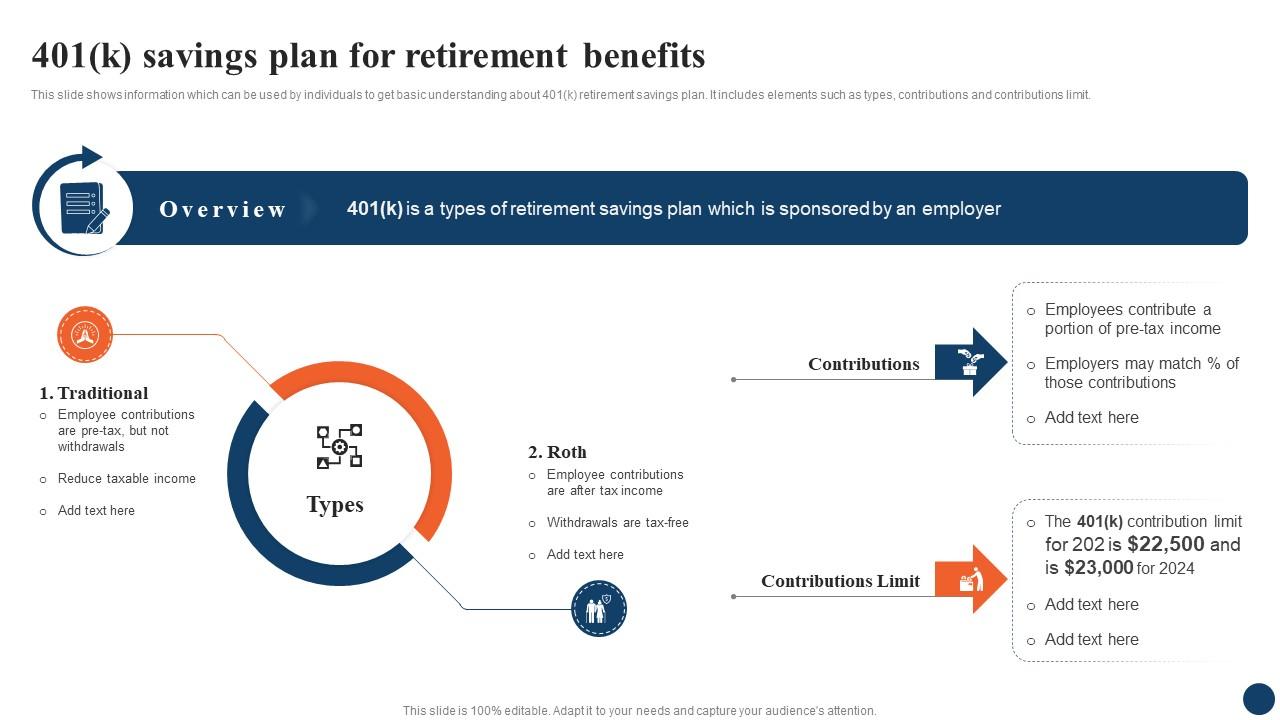

Okay, so the basic idea is this: you contribute a portion of your paycheck before taxes are taken out. Yes, you read that right! Lowering your taxable income now? Talk about a win-win. It’s like getting a mini-raise, only you can't spend it on that new gadget...yet. Think of it as delayed gratification on steroids.

Must Read

And then? The magic happens. That money gets invested (more on that later) and hopefully grows, thanks to the power of compound interest. It’s basically your money making more money. Like planting a money tree... a very, very slow-growing money tree.

Raley's might even match a portion of your contributions! That’s essentially free money! Seriously, who turns down free money? It's like finding a twenty dollar bill in your old jeans, but way better, because it’s for your future self. Check with HR for the exact matching details, because, you know, fine print and all that jazz.

Investing: Not as Scary as it Sounds (Probably)

Now, here comes the part where some people glaze over. Investing. But hold on! Don't run away screaming. It's not as complicated as it seems. (Okay, maybe it can be, but we're keeping it simple here.)

Basically, your 401(k) offers a range of investment options, usually mutual funds or target-date funds. A mutual fund is like a basket of different stocks and bonds. Diversification, baby! A target-date fund is even simpler – you pick the fund closest to your estimated retirement year (e.g., 2055), and the fund automatically adjusts its investments over time to become more conservative as you get closer to retirement. Easy peasy.

Not sure where to start? Don't feel bad! Many 401(k) plans have resources and tools to help you choose investments based on your risk tolerance and how long you have until retirement. Seriously, explore those resources. They're there to help you not mess things up (too badly, anyway!).

The Nitty-Gritty: Things to Keep in Mind

Alright, let's talk about the less-fun stuff, but still important!

Early withdrawals: Generally, if you take money out of your 401(k) before age 59 ½, you'll face penalties and taxes. Ouch! So, try to resist the urge to raid your retirement savings for, say, that yacht you've always wanted (unless, you know, you're already retired, then go for it!). Think of it as a savings account you can’t touch... until you really need it. Or, more accurately, deserve it after decades of hard work.

Vesting: This refers to how long you need to work at Raley's to be fully entitled to the employer matching contributions. If you leave before you're fully vested, you might forfeit some of that sweet, sweet free money. Make sure you understand the vesting schedule. It's like knowing when the cookies are finally done baking – you don’t want to pull them out too early!

Fees: Yep, there are fees associated with managing your 401(k). They can eat into your returns over time, so pay attention to what they are. Knowledge is power (and, in this case, potentially more money in your pocket!).

So, Should You Do It?

Honestly? Probably, yes! Especially if Raley's offers a matching contribution. It's like turning down free ice cream. Why would you do that? It's a powerful tool for building long-term financial security. Future you will thank you – probably while sipping that margarita on the beach.

Just remember to do your homework, understand your investment options, and don't be afraid to ask questions! Your future self depends on it!