Emergency Loans For 500 Credit Score

Okay, so picture this: you're humming along, life is good, maybe you just splurged on that limited-edition avocado toaster you've been eyeing (we've all been there, don't judge!), and then… BAM! The car decides it's had enough. Engine light brighter than a supernova, and the mechanic's quoting you a price that makes your eyes water. Happened to me. Twice. (Okay, maybe three times. I have terrible luck with cars).

Suddenly, that avocado toast feels like a luxury you can't afford, and the reality of needing fast cash sets in. And then the dreaded question pops up: what if my credit score is, well, let’s just say not stellar? Like, hovering around the 500 mark? Panic mode: activated.

Don’t worry. Take a deep breath. You're not alone, and there are options. Maybe not the most amazing options, let's be real, but options nonetheless. We're talking about emergency loans for the credit-challenged, the fiscally-ambitious-but-currently-down-on-their-luck. Let's dive in.

Must Read

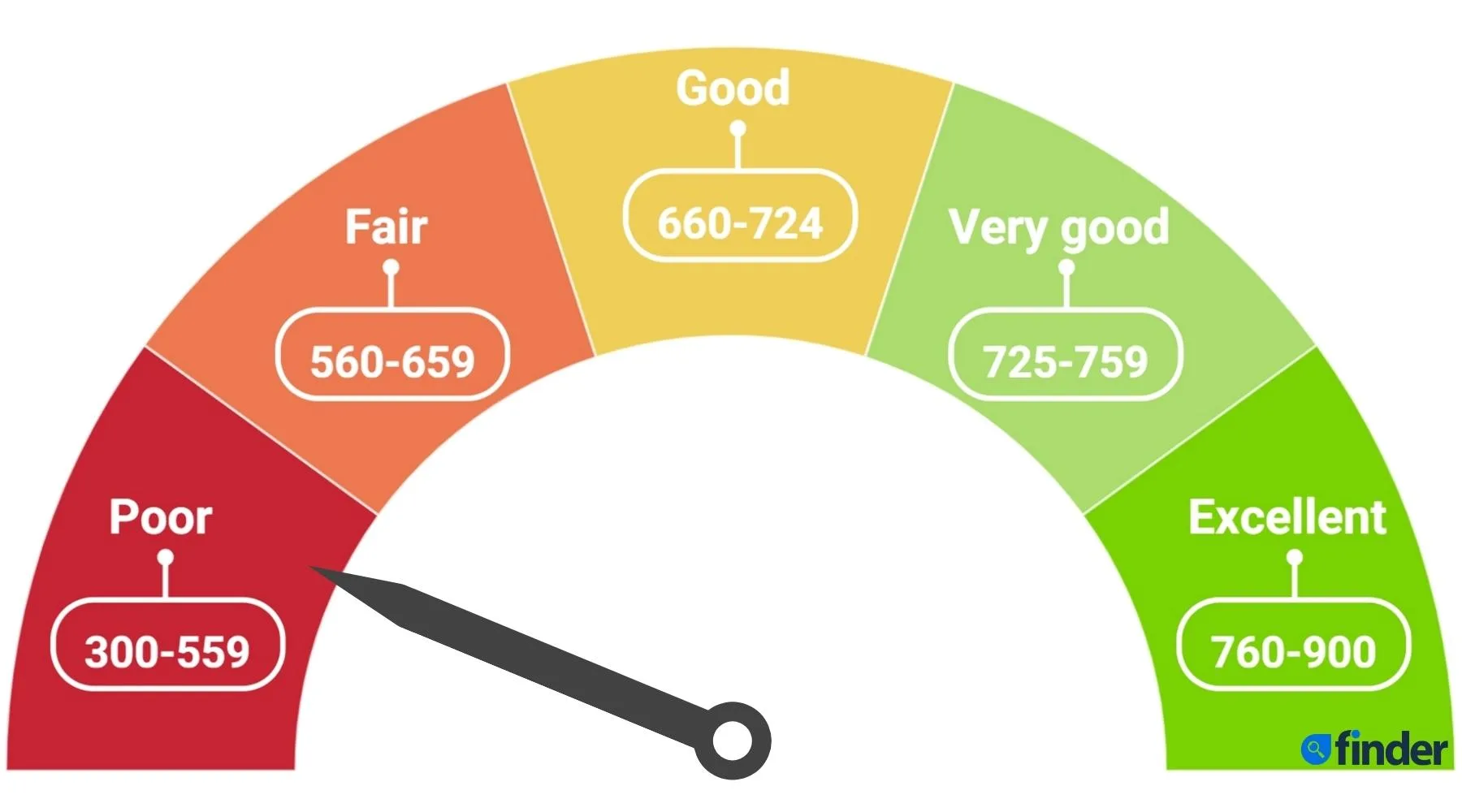

Understanding the Landscape: 500 Credit Score & Loans

First things first: a 500 credit score is generally considered “poor.” Lenders see it as a sign that you're a risky borrower. They worry you might not pay them back. (And let's be honest, maybe they have a point? No judgement!). That's why it's harder to get approved for traditional loans with low rates.

But “harder” doesn't mean impossible. It just means you need to be smarter about where you look and what to expect. Think of it as a financial scavenger hunt. The prize is the loan, the clues are your research, and the obstacles are… well, the lenders.

So, what are your potential lifelines?

Potential Loan Options (with a Big Asterisk)

Alright, let's explore some avenues you might consider. But remember that asterisk I mentioned? It's important! These options usually come with higher interest rates and fees. Because, you know, risk.

- Payday Loans: These are short-term, high-interest loans designed to be repaid on your next payday. While tempting for their quick access, they are notoriously expensive. Think hundreds of percentage points in interest. Seriously, proceed with extreme caution (like, HAZMAT suit caution). I'm not a financial advisor (disclaimer!), but these are generally considered a last resort.

- Pawn Shop Loans: You bring in something of value – jewelry, electronics, your grandmother's antique teapot (maybe reconsider that one) – and they give you a loan based on its value. If you don't repay the loan within the agreed timeframe, they keep your item. This can be a quick solution, but you risk losing your belongings.

- Credit Union Loans: Credit unions often have a more community-focused approach and may be more willing to work with individuals with less-than-perfect credit. Especially if you're already a member. It’s worth checking out their offerings and seeing if they have any programs for borrowers with lower credit scores.

- Secured Loans: This is where you offer something as collateral – like your car or a savings account – to secure the loan. Because the lender has something to fall back on, they might be more willing to lend to you, even with a 500 credit score. But be warned: if you can't repay, they can take your collateral!

- Online Lenders: There are numerous online lenders that specialize in loans for people with bad credit. Be very careful here. Do your research! Read reviews! Make sure they are legitimate and not predatory lenders trying to take advantage of your situation.

Boosting Your Chances of Approval

Okay, so you’ve picked your poison (metaphorically speaking, of course. Choose wisely!). Now, how do you increase your odds of getting approved?

- Have a Co-Signer: A co-signer is someone with good credit who agrees to be responsible for the loan if you can't repay it. This significantly reduces the lender's risk and improves your chances of approval. Maybe Mom or Dad can help? (But don't ruin Thanksgiving dinner over it).

- Show Proof of Income: Even with a low credit score, proving you have a stable income source is crucial. Pay stubs, tax returns, bank statements – gather everything you can to demonstrate your ability to repay the loan.

- Consider a Smaller Loan Amount: Asking for a smaller amount reduces the lender's risk and might make them more willing to approve your application. Do you really need to borrow the full amount?

- Shop Around and Compare Rates: Don't just accept the first offer you receive. Compare rates and terms from multiple lenders to ensure you're getting the best possible deal. Seriously, this is crucial! A little bit of research can save you a lot of money in the long run.

Beyond the Emergency: Building Better Credit

Okay, you've secured the loan, fixed the car (or whatever the emergency was), and breathed a sigh of relief. But this isn't the end of the story. Now's the time to focus on improving your credit score so you don't find yourself in this situation again (or at least not as often!).

Here are a few quick tips:

- Pay your bills on time, every time. Seriously, this is the biggest factor in your credit score.

- Keep your credit utilization low. Don't max out your credit cards. Aim to keep your balances below 30% of your credit limit.

- Check your credit report regularly for errors. Dispute any inaccuracies you find.

Dealing with a financial emergency when you have a low credit score is stressful, but it's not insurmountable. By understanding your options, boosting your chances of approval, and focusing on building better credit, you can navigate this difficult situation and emerge stronger on the other side. Good luck! (And maybe think twice before buying that next avocado toaster… just kidding!).