Financial Markets And Services Act 2000

Ever heard of the Financial Services and Markets Act 2000? Yeah, the name sounds about as exciting as watching paint dry, right? But trust me, underneath that bureaucratic-sounding title lies a piece of legislation that's actually pretty darn important. Think of it like the secret sauce that keeps the UK's financial engine humming along nicely. So, grab a cuppa, and let's dive in, shall we?

Basically, this Act, often shortened to FSMA 2000, is the rulebook for the financial services industry in the UK. We're talking banks, insurance companies, investment firms – the whole shebang! Imagine a bustling city filled with all sorts of vendors and shops. FSMA 2000 is like the city council, setting the rules to make sure everyone plays fair and no one gets ripped off. Makes a bit more sense now, doesn't it?

Why Should I Care?

Okay, okay, you might be thinking, "So what? I'm not a banker or an investor." But here’s the thing: this Act touches pretty much everyone’s life. Got a bank account? Insurance policy? Pension? Then FSMA 2000 is working in the background, protecting your interests. Without it, the financial world would be a bit like the Wild West – chaotic, unregulated, and potentially full of cowboys looking to make a quick buck at your expense.

Must Read

Think of it this way: imagine you're buying a car. You'd want to know it's safe, reliable, and that the salesperson isn't trying to pull a fast one, right? FSMA 2000 helps ensure the same level of protection when you're dealing with financial products. It sets standards for how financial firms operate, how they treat their customers, and how they manage risks. Pretty crucial stuff, wouldn’t you agree?

The Key Players: FCA and PRA

FSMA 2000 established two key watchdogs: the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA). Think of them as the police force and the health inspectors of the financial world. The FCA is all about protecting consumers, ensuring that financial firms are behaving honestly and fairly. They're the ones who'll step in if a bank is charging excessive fees or mis-selling products. In simple terms, they ensure firms treat their customers fairly.

The PRA, on the other hand, is focused on the stability of the financial system as a whole. They keep an eye on banks and insurers to make sure they're financially sound and won't go bust, causing a domino effect across the economy. They are particularly interested in the resilience of firms, especially the big ones that could cause systemic risk. Remember the 2008 financial crisis? The PRA is there to try and prevent something like that from happening again!

Cool Things FSMA 2000 Does

So, what are some of the cool (or at least, potentially cool) things that FSMA 2000 does? Well, it gives the FCA and PRA a lot of power. They can investigate financial firms, impose fines, and even ban individuals from working in the industry. Think of it as the ultimate power to put naughty banks in the corner.

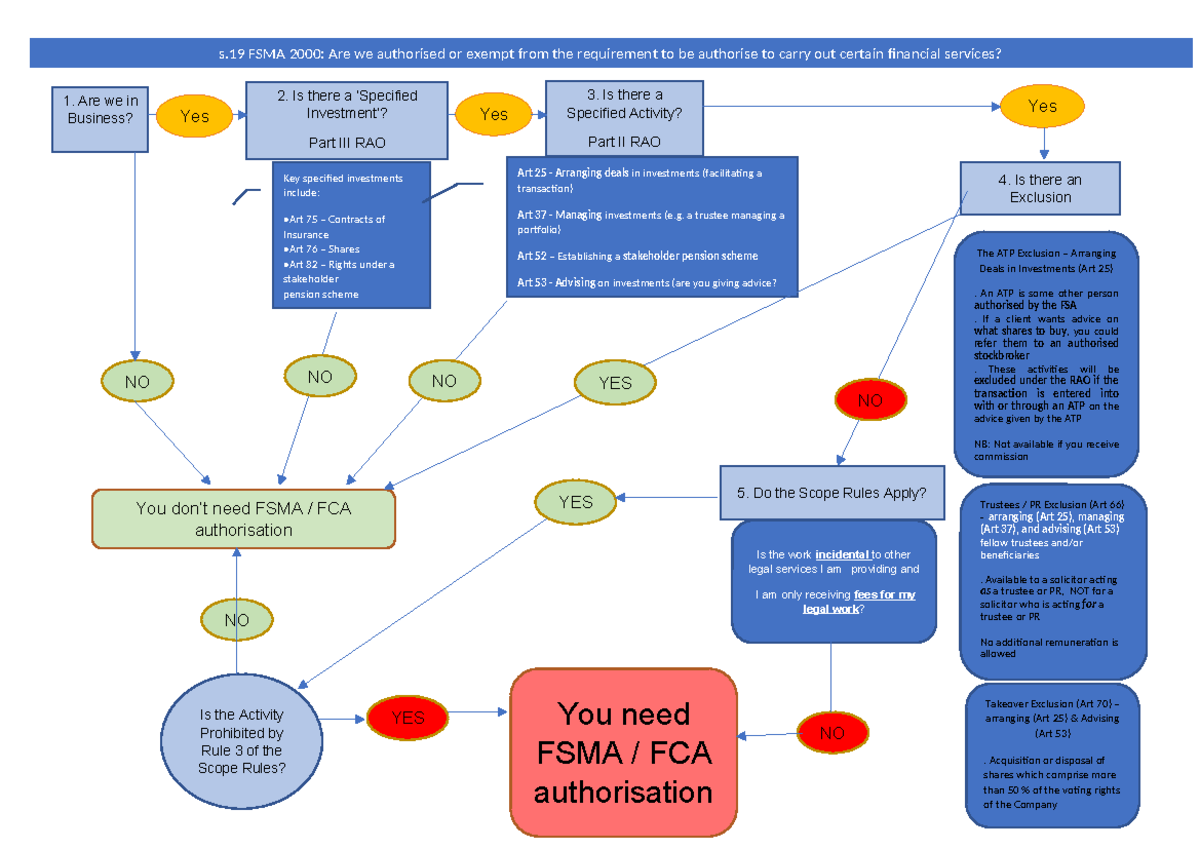

It also introduced a concept called "authorised persons." Only firms that are authorised by the FCA or PRA can carry out regulated financial activities. This means that if someone is offering you investment advice or selling you insurance, they need to be properly authorised. You can check the FCA's register to make sure they are legit. This is all about weeding out the dodgy dealers and ensuring that you're dealing with reputable firms.

Furthermore, FSMA 2000 has provisions for compensating consumers who have been mis-sold financial products. If you've been given bad advice or sold a product that wasn't suitable for you, you may be able to claim compensation. It's not a guaranteed win, but it gives you a fighting chance to get your money back. Like a little "get out of jail free" card for financial mishaps.

Is It Perfect?

Now, is FSMA 2000 a perfect piece of legislation? Of course not! Like any law, it has its critics and its flaws. Some argue that it's too complex, too bureaucratic, and that it stifles innovation. Others argue that it doesn't go far enough to protect consumers and prevent financial crises. There's always room for improvement, right?

But overall, FSMA 2000 has played a vital role in shaping the UK's financial landscape. It’s provided a framework for regulating the industry, protecting consumers, and promoting financial stability. It’s the unsung hero, working quietly in the background to ensure that our financial system is (relatively) safe and sound. Pretty neat, huh?

So, the next time you hear someone mention FSMA 2000, don’t just glaze over. Remember that it’s more than just a bunch of legal jargon. It’s a cornerstone of the UK economy, and it affects all of us in ways we might not even realise. And hey, maybe you even learned something new today! Now, back to that cuppa…