Credit Card Due Date Vs Statement Date

Ah, the credit card! It’s often seen as a trusty sidekick, a magic wand for last-minute needs, or even a clever little tool that helps us navigate the world. But deep within its shiny plastic heart lies a mystery for many: the curious case of the Statement Date versus the Due Date.

Don't worry, this isn't a dry lecture! Think of it as uncovering a delightful secret, a bit like finding an extra cookie hidden in the jar, or realizing you have an entire free afternoon you didn't know about.

The Grand Storyteller: Your Statement Date

Imagine your credit card company is a meticulous storyteller. Every month, on a specific day, it takes a deep breath and says, "Right, let's recap everything that happened in the last chapter!"

Must Read

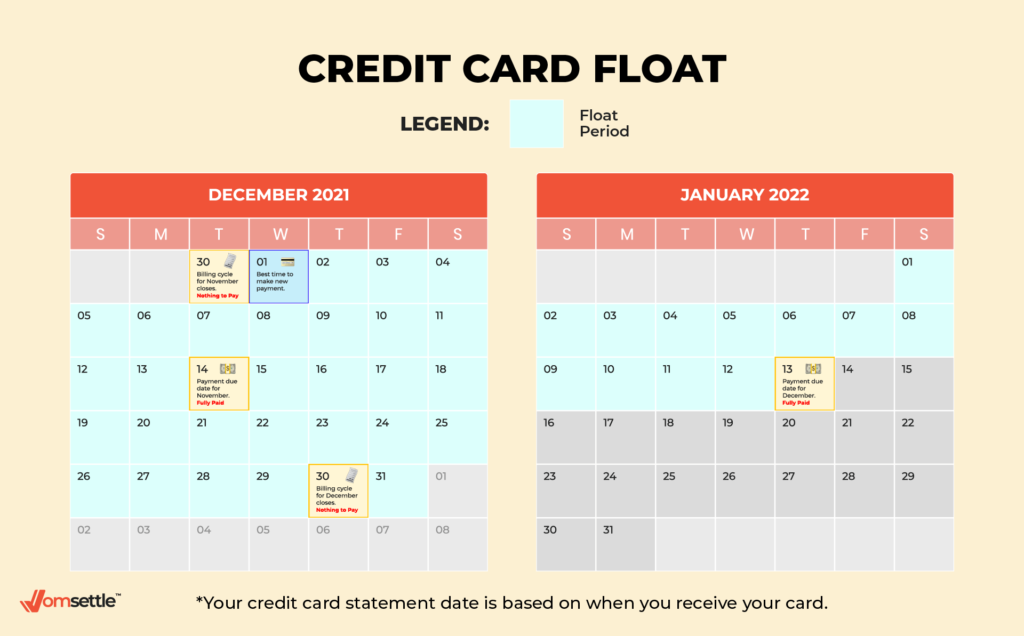

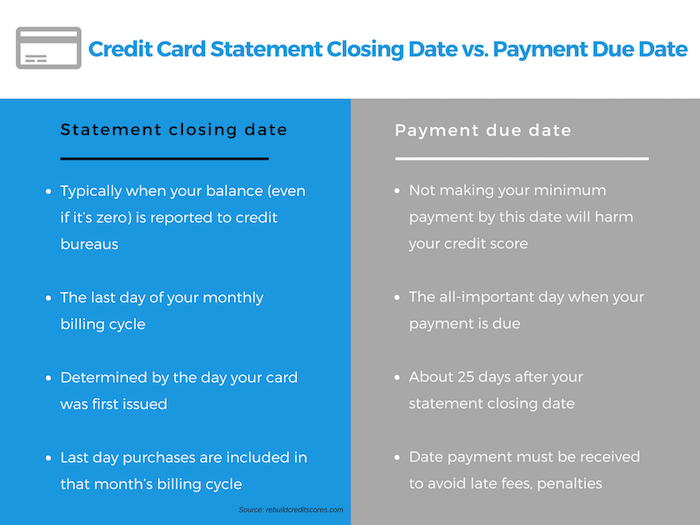

This day is your Statement Date. It's the moment your credit card account takes a snapshot of all your spending since the last statement. Every coffee, every grocery run, every online find – it’s all gathered up.

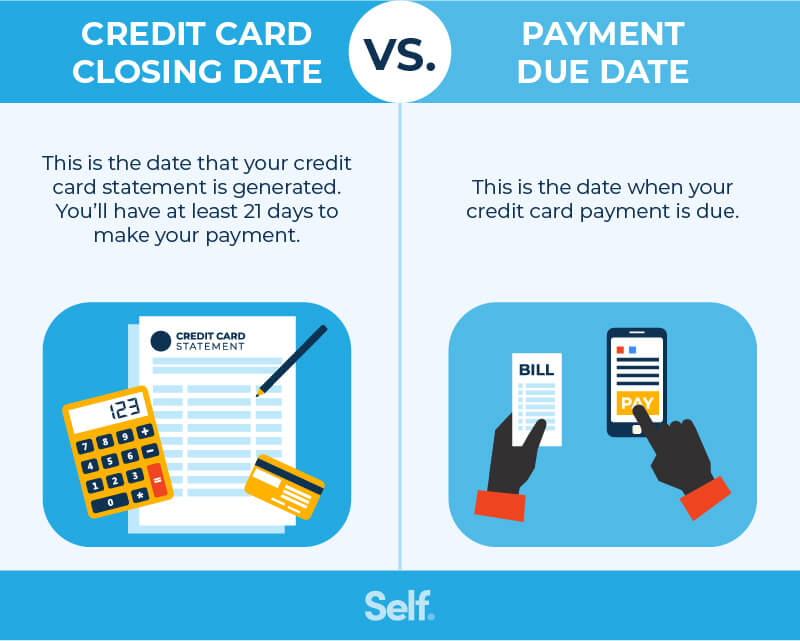

Think of it as the grand finale of your spending period. It’s when your bill is officially generated, showing you exactly what you owe for that particular chapter of your financial story.

"The Statement Date is like the final page of your monthly spending diary. It closes one chapter and prepares for the next."

It’s not a day to panic and pay immediately. Oh no, that’s a common misconception that causes so much unnecessary stress! Instead, it’s a moment of reflection, a summary of your delightful adventures with your card.

It’s like receiving a beautifully compiled photo album of your recent travels. You don't have to pack your bags again right then; you just get to enjoy the memories and see where you've been.

This date marks the end of your billing cycle. It’s the point where all transactions up to that specific day are tallied up and presented to you in one neat package.

For many, this date is a secret source of anxiety, mistakenly believed to be the deadline itself. But discovering its true role is like finding out your favorite book has a bonus chapter!

The Graceful Messenger: Your Due Date

Now, meet the Due Date, the polite and patient messenger who arrives a little later. This is the date by which your payment needs to be received by your credit card company.

It’s typically a generous 20 to 25 days after your Statement Date. Isn't that a lovely surprise? You have a whole chunk of time, a financial breathing room, between knowing what you owe and actually paying it.

"Your Due Date is the friendly reminder, the gentle nudge, saying, 'No rush, but let's settle up by this day, shall we?'"

This period, this glorious gap between the Statement Date and the Due Date, is your grace period. It's like finding a lovely bench to rest on during a marathon, or an extra hour of sleep on a Sunday morning.

It’s specifically designed to give you time to review your statement, make sure everything looks right, and then send your payment without feeling rushed or stressed.

Imagine getting an invitation to a party (your Statement Date), and then having a few weeks to pick out the perfect outfit and plan your arrival (your Due Date). You don’t have to show up the moment the invitation lands in your mailbox!

Understanding this distinction is key to a harmonious relationship with your credit card. It’s the difference between feeling constantly behind and feeling wonderfully in control.

The "Aha!" Moment: Connecting the Dots

The biggest misunderstanding, and often the source of so much financial tension, is confusing these two dates. Many people mistakenly believe they need to pay their bill on or very soon after the Statement Date.

But when you realize the grace period is there, patiently waiting for you, a little lightbulb often goes off. It’s like finding a secret path in a maze you thought was dead-ended.

This realization empowers you. It means you don't have to scramble to move funds or feel panicked the moment your statement pops into your inbox. You have a window, a buffer, a friendly space.

Consider Leo, who used to dread his credit card statements. He'd open them with a sigh, feeling the immediate pressure to pay. Then, a friend gently explained the grace period.

Leo’s relief was palpable. "You mean I actually have time?" he exclaimed. It was a simple piece of information, but it transformed his financial outlook from stressed to serene.

This isn't about procrastination; it's about smart planning. It's about letting your money work for you, even for a few extra weeks, instead of rushing it off prematurely.

The humorous side is often found in the shared experience of this revelation. "I can't believe I didn't know this!" is a common refrain, usually followed by a chuckle of relief.

Harmony in Your Wallet: Making Dates Work for You

When you understand the beautiful dance between the Statement Date and the Due Date, you unlock a hidden power. You can synchronize your payments with your paychecks, ensuring you always have funds ready.

It’s like a conductor leading an orchestra, ensuring every instrument comes in at the right time. You are the conductor of your own financial symphony.

This newfound clarity can be surprisingly heartwarming. It replaces apprehension with assurance, worry with wisdom. Your credit card becomes less of a mysterious beast and more of a predictable, helpful friend.

No more midnight dashes to pay a bill you thought was due. No more nervous glances at your bank balance right after seeing your statement balance. Just calm, cool, collected control.

The "surprise" benefit isn't just about avoiding late fees, although that's a fantastic perk. It’s about cultivating a healthier, less stressful relationship with your money.

It gives you the psychological advantage. Instead of reacting to deadlines, you are proactively managing your finances, like a seasoned captain navigating clear waters.

So, take a moment to find your own Statement Date and Due Date. Mark them on your calendar, set a reminder, or even give them fun nicknames like "The Accountant's Day" and "Payment Party Day."

Embrace the grace period. Use it wisely. It's a gift of time, a buffer against financial hurries, and a testament to the fact that even seemingly complicated financial matters can have a simple, easy-to-understand rhythm.

In the end, understanding these two simple dates transforms your credit card from a potential source of confusion into a clear and helpful tool. It gives you peace of mind, and isn't that a truly wonderful feeling?