Par Value Of A Stock Refers To The:

Alright, gather 'round, folks! Let's talk about something thrilling! Something that makes Wall Street bankers sweat (maybe not, but let's pretend it does). I'm talking about... par value! Now, before your eyes glaze over, let me assure you, this isn't as boring as your uncle's stamp collection. (Sorry, Uncle Steve, but stamps? Really?).

So, what is this "par value" thing? Well, imagine you're starting a lemonade stand. (Stick with me, it gets better!). You need capital, right? You decide to sell little "shares" of your lemonade stand dream to your friends. These shares are, in essence, stock in your delicious, citrus-fueled empire.

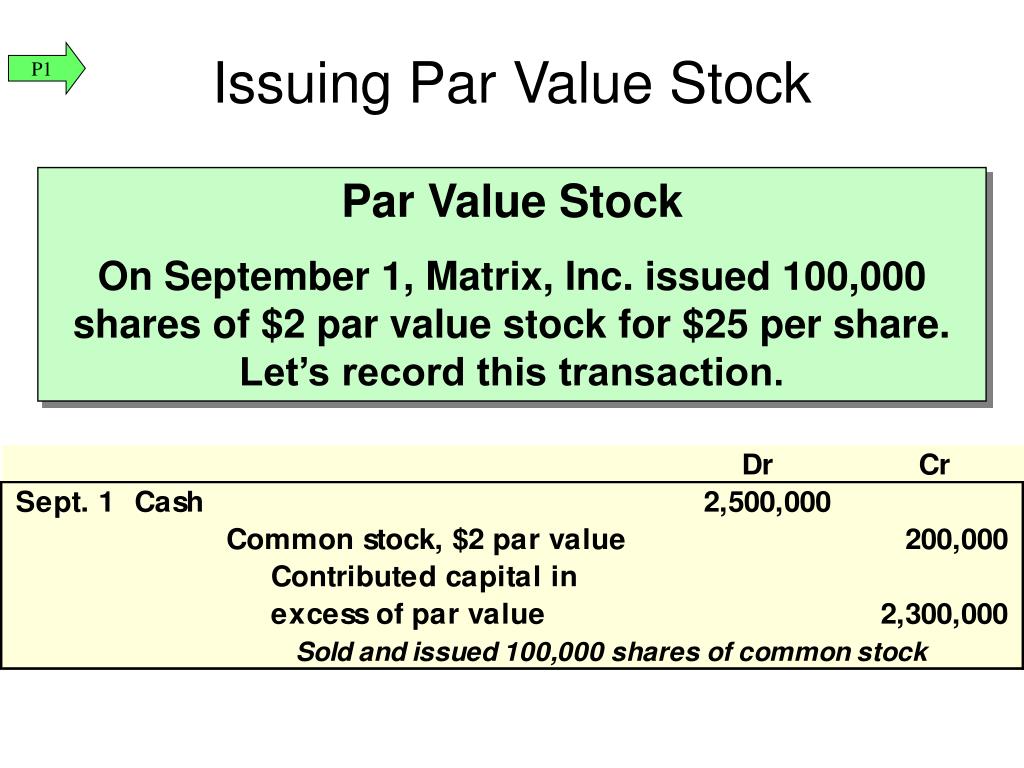

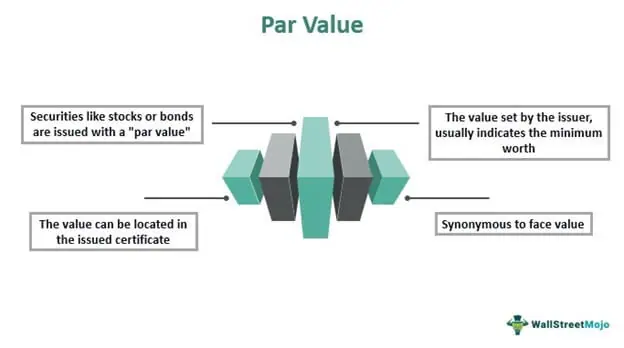

Now, let's say you decide that each share has a face value of, oh, let's say…50 cents. That, my friends, is essentially the par value. It's the minimum amount a share is supposed to be worth when the company initially issues it. I say "supposed" because things get a little…quirky.

Must Read

Think of it like this: it's the legal equivalent of declaring, "Hey, world, this share is at least worth 50 cents!" It's the company giving itself a participation trophy before the race even starts. It’s like saying, "I promise to pay you 50 cents if I ever liquidate."

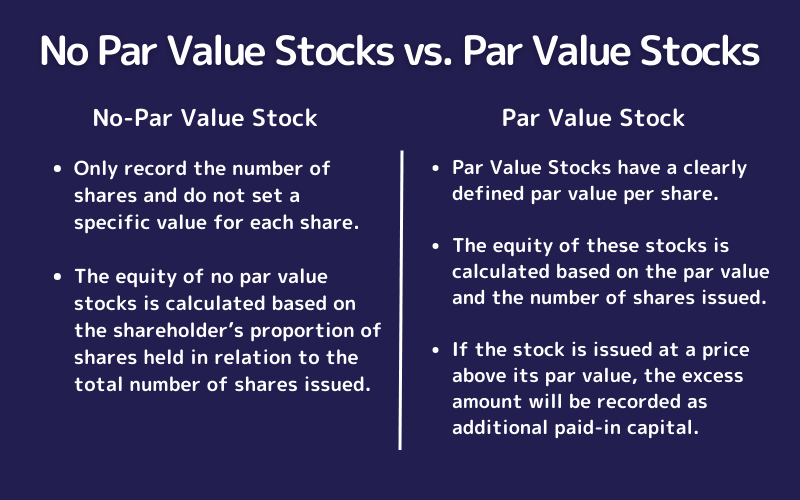

Why 50 cents? Why not a dollar? Or a million dollars?! Well, usually, par value is kept ridiculously low – like, a penny, or even a fraction of a penny. Why so low? Because back in the day, and even still today in some places, you couldn't sell stock for less than its par value. So, if your par value was a dollar, and nobody wanted your stock, you were stuck. Lowering it means the company has more flexibility to raise money, even if the market is skeptical about their new line of cat sweaters.

Par Value: More Like "Rarely Relevant Value"

Here's the kicker: par value is almost entirely irrelevant in the grand scheme of stock market things. I know, I know. I built it up, and now I'm tearing it down. But it's true! It's like the appendix of the financial world – it's there, but nobody really knows what it's for anymore. And sometimes it causes problems (like lawsuits when companies sell stock below par value in the past, though that's rare now).

The actual market value of a stock – what people are willing to pay for it on the open market – is determined by a whole bunch of factors: the company's earnings, its growth prospects, the overall economy, the CEO's hair gel situation… okay, maybe not the hair gel, but you get the idea. The par value is just a tiny, almost insignificant footnote in the company's financial history. Think of it as the company’s birth certificate: technically important, but not a reflection of how well they're actually doing right now.

Imagine Beyonce starting a company. Do you think anyone would care what the par value of her stock is? No way! People would be throwing money at her just to own a piece of the Beyonce empire, regardless of whether the initial "face value" was a penny or a potato.

So, Why Bother Knowing About It?

Okay, okay, fair question. If it's so unimportant, why are we even talking about it? Well, knowledge is power, my friend. And, occasionally, you might see it pop up on a company's balance sheet, usually under the "common stock" section. It's more for accounting purposes than anything else, helping to track the amount of capital the company has raised from issuing stock.

Plus, knowing about par value is like knowing the capital of Uzbekistan – it's a great conversation starter at parties! (Okay, maybe not, but at least you can impress your finance-obsessed friends.)

The reason it still exists is a mix of historical reasons and legal requirements. It’s a holdover from a time when regulating stock sales was a bit more Wild West. Now, it’s more of a quirky formality.

So, next time you hear someone mention "par value," you can confidently nod your head and say, "Ah yes, that largely irrelevant but historically interesting metric! A relic of a bygone era!" Then, quickly change the subject to something more exciting, like the stock market's latest meme stock craze or the ongoing debate about pineapple on pizza. (Personally, I'm pro-pineapple!).

Just remember: Don't base your investment decisions on par value! Focus on the real stuff: the company's fundamentals, its industry, and whether or not the CEO looks like they actually know what they're doing (and maybe, just maybe, their hair gel situation).