Is The Discover Fico Score Accurate

Okay, let's talk about something that makes everyone sweat a little: your Discover FICO Score. You know, that number Discover so generously flashes on your statement? The one that makes you either puff out your chest or hide under the covers?

Is it accurate? That's the million-dollar question. Or, more accurately, the "will I get approved for a decent mortgage rate?" question.

Here's my, shall we say, unpopular opinion: It's...mostly fine. But also, maybe don't bet your life savings on it.

Must Read

Think of it like this. Imagine you're trying to guess someone's weight. You eyeball them. You consider their height. You maybe take a peek at what they're wearing. You come up with a number.

Is that number exactly right? Probably not. Is it in the ballpark? Likely. Is it good enough to know if they're going to win a sumo wrestling match against you? Absolutely.

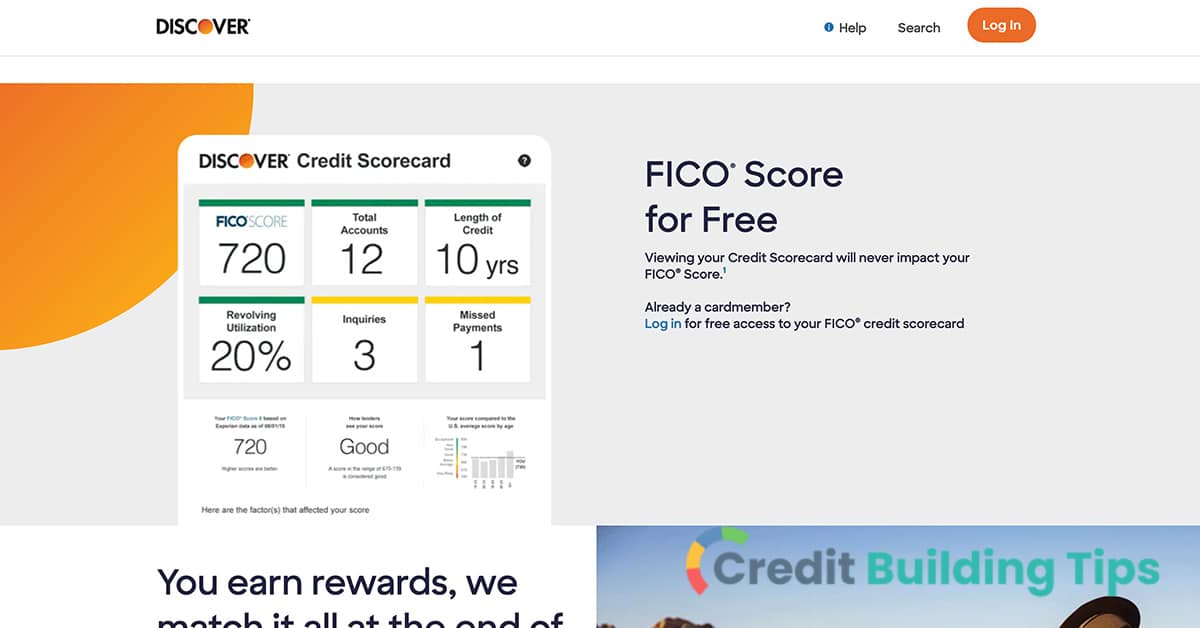

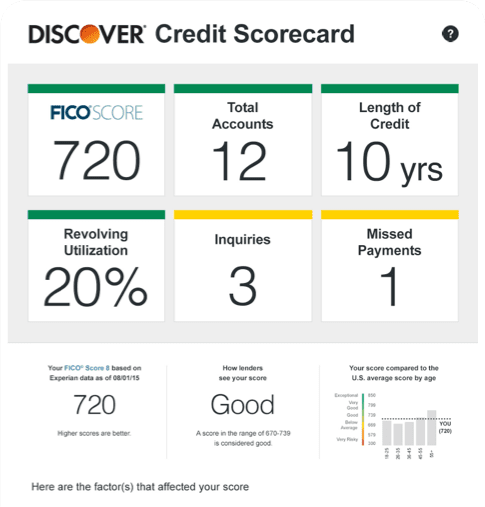

Your Discover FICO Score is kind of like that. It's an estimate. A calculated guess based on a mountain of data. It's a snapshot of your creditworthiness at a particular moment in time.

But Here's the Catch (There's Always a Catch, Right?)

The thing is, there are different FICO scores. Like, a whole family of them. There's FICO 8, FICO 9, and even older versions still kicking around. Each one weighs different factors a little differently.

So, Discover might be showing you your FICO Score 8, powered by TransUnion. Cool. But the car dealership might be using FICO Auto Score 5, which, let's be honest, sounds like something from a vintage video game. And the mortgage lender? Who knows! They might be using a mystical, ancient algorithm passed down through generations. Just kidding (mostly).

And that's where things get a little…fuzzy. The number Discover shows you can be a helpful indicator, but it's not the be-all and end-all. It's not the one true score to rule them all.

So, What's a Credit-Conscious Person to Do?

First, don't obsess over the number. Seriously. Stressing about your credit score will give you wrinkles, and wrinkles are bad for your credit... just kidding (again!).

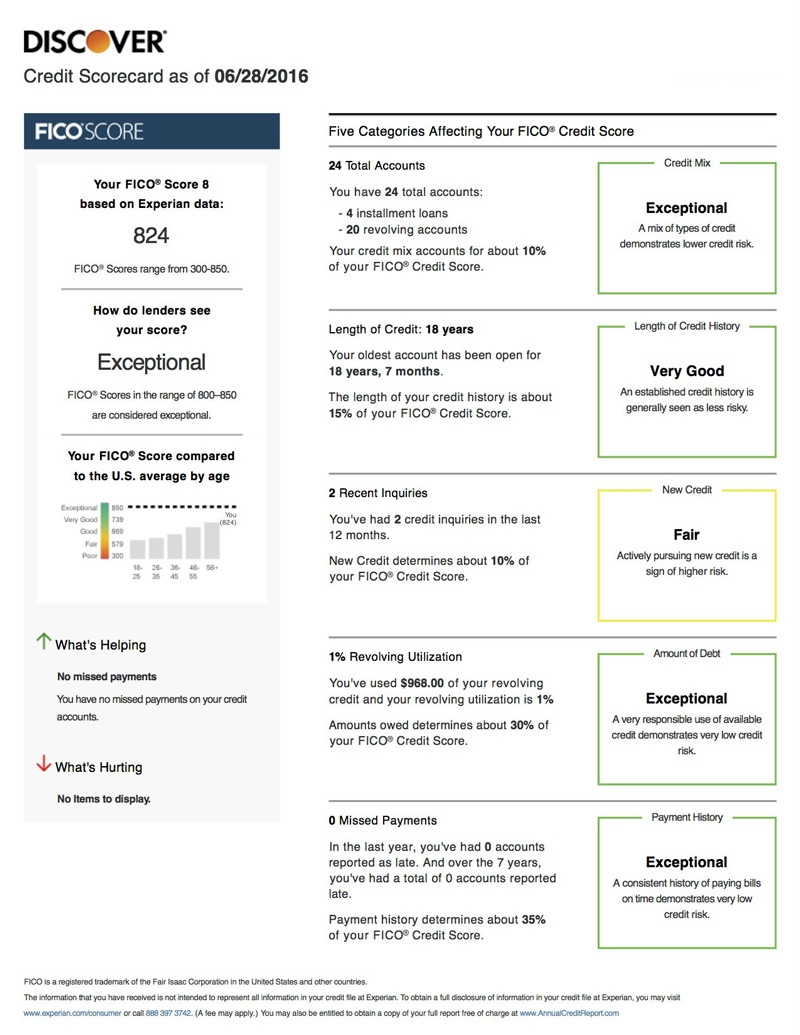

Second, understand what goes into your credit score. Things like payment history (pay your bills on time!), credit utilization (don't max out those cards!), and length of credit history (patience is a virtue!) all play a role.

Third, check your actual credit reports from all three major bureaus: Equifax, Experian, and TransUnion. You're entitled to a free report from each one annually at AnnualCreditReport.com. Look for errors and dispute anything that looks fishy. It's like spring cleaning for your financial life!

Fourth, treat the Discover FICO Score as a general guide. It's a helpful tool for understanding where you stand. If it's in a good range, awesome! If it's not, use it as motivation to improve your credit habits.

My Totally Unsolicited (But Hopefully Helpful) Advice

Don't get too hung up on one specific number. Your creditworthiness is a complex and ever-evolving thing. The Discover score is simply an approximation of where you stand. Use it wisely, but don't let it define you.

Instead of obsessing over the score, focus on building good credit habits. Pay your bills on time, keep your credit utilization low, and be patient. A good credit score will naturally follow.

And finally, remember that a good credit score is a marathon, not a sprint. It takes time and consistent effort to build a solid credit history. So, relax, breathe, and keep making smart financial choices. You got this!

The Discover FICO Score: It's not perfect, but it's perfectly adequate... sometimes.

Now, if you'll excuse me, I'm going to go check my own score. Just kidding... mostly.