How Many Payday Loans Can I Get

Let's be honest, nobody wants to be thinking about payday loans. But life happens! Unexpected bills pop up, car repairs loom, and sometimes you just need a little help to bridge the gap until your next paycheck. So, if you're here wondering, "How many payday loans can I actually get?" you're in the right place. We're going to break down the rules (or, rather, the lack thereof in some places) surrounding multiple payday loans in a straightforward and easy-to-understand way.

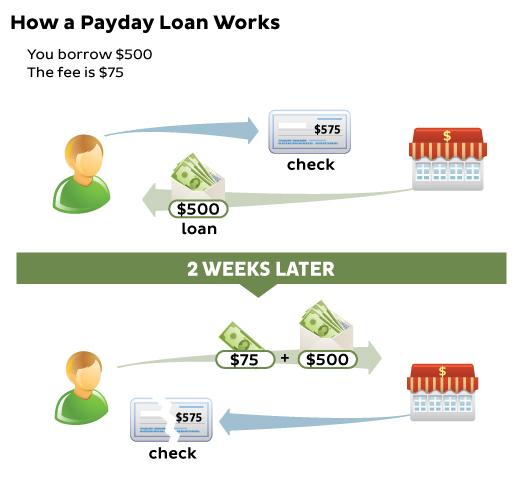

First, let's clarify the purpose of a payday loan. It's a short-term, high-interest loan designed to cover immediate expenses. The idea is that you borrow a relatively small amount and repay it when you receive your next paycheck. Think of it as a quick fix, not a long-term financial strategy. Benefits? Accessibility and speed. They are typically easier to get than traditional loans, especially if you have less-than-perfect credit, and the funds can often be available very quickly.

Now, the big question: how many can you snag? The answer? It depends! There's no one-size-fits-all rule. The number of payday loans you can have simultaneously is largely dictated by the laws of your state. Some states have strict regulations, limiting you to just one outstanding payday loan at a time. They might use a state-wide database to track borrowing and prevent people from taking out multiple loans from different lenders. The goal here is to protect consumers from getting trapped in a cycle of debt.

Must Read

Other states are far more lenient. They may have no specific laws restricting the number of payday loans you can have. In these states, you could theoretically take out as many loans as lenders are willing to give you. However, just because you can doesn't mean you should!

Even in states without specific limits, individual lenders might have their own policies. They'll assess your ability to repay the loan based on your income and other factors. They might be hesitant to approve you for a loan if they see you already have several outstanding payday loans, as this significantly increases the risk that you won't be able to repay them.

So, what's the takeaway? Do your research! Before you even consider taking out a payday loan, understand the laws in your state. A quick online search for "payday loan laws in [your state]" should give you the information you need. Contact your state's banking or financial regulation authority if you need more clarification.

Ultimately, remember that while payday loans can be a tempting solution for immediate financial needs, they come with significant risks. The high interest rates and short repayment periods can easily lead to a cycle of debt. It's crucial to explore other options first, such as negotiating with creditors, seeking assistance from local charities, or exploring personal loan options from banks or credit unions. If you do choose to use a payday loan, borrow only what you absolutely need and have a clear plan for repayment. Financial wellness is the goal!