Do I Need Life Insurance After Retirement

Okay, so picture this: you're finally retired! You’ve traded in spreadsheets for sunbathing, conference calls for cat naps, and that soul-crushing commute for, well, nothing much. You’re free! But a nagging thought creeps in between rounds of golf and early bird specials: “Do I still need life insurance? Am I paying for something I don’t even need anymore?”

Let's be honest, thinking about life insurance isn’t exactly a barrel of laughs. It’s like discussing funeral arrangements while simultaneously planning your dream vacation. Morbid, right? But hear me out. This doesn't have to be depressing! We can tackle this financial "adventure" together.

The "I'm Rich, Btch!" Scenario (And Why It Might Not Be Enough)

Maybe you’re thinking, "I'm loaded! I’ve got more money than Croesus! My heirs will be swimming in gold coins like Scrooge McDuck!" Fantastic! But even Scrooge had to worry about leaky roofs and unexpected goblin attacks (okay, maybe not goblin attacks, but you get the idea). Even with a mountain of cash, life insurance can still be useful.

Must Read

Think of it this way: Estate taxes are like vultures circling your hard-earned fortune. They can swoop in and take a *significant bite out of your assets. Life insurance can provide the funds to cover these taxes, ensuring your heirs actually inherit what you intended.

And speaking of heirs, are they all financially responsible? I mean, are we talking diligent savers or folks who'd blow it all on a solid gold toilet and a lifetime supply of artisanal cheese puffs? (No judgment, I love cheese puffs too). Life insurance can help protect their inheritance from… well, themselves.

The "I'm On a Fixed Income, Help Me!" Scenario

On the other hand, perhaps you’re living on a fixed income. The idea of shelling out more money for anything, even something as potentially valuable as life insurance, makes you break out in a cold sweat. Totally understandable!

The good news is, you might be able to reduce your coverage. If your kids are grown, independent, and have successful ferret grooming businesses (hey, it could happen!), you might not need as much insurance as you did when they were toddlers eating paste. Less coverage typically means lower premiums. Win-win!

Consider this: what debts will your loved ones be stuck with when you're gone? Mortgage? Credit card bills that mysteriously keep appearing even though you swear you only use them for emergencies (like that limited-edition gnome garden set)? Life insurance can provide a safety net to cover these expenses and prevent them from having to sell your prized collection of porcelain thimbles.

The "But I Have Social Security Survivor Benefits!" Argument

Okay, yes, Social Security does offer survivor benefits. But let's be real, those benefits are often a drop in the bucket. Think of it as a starter kit for grieving, not a full-blown financial bailout. They might help cover immediate expenses, but they probably won't fund a lifetime of therapy and gourmet ice cream.

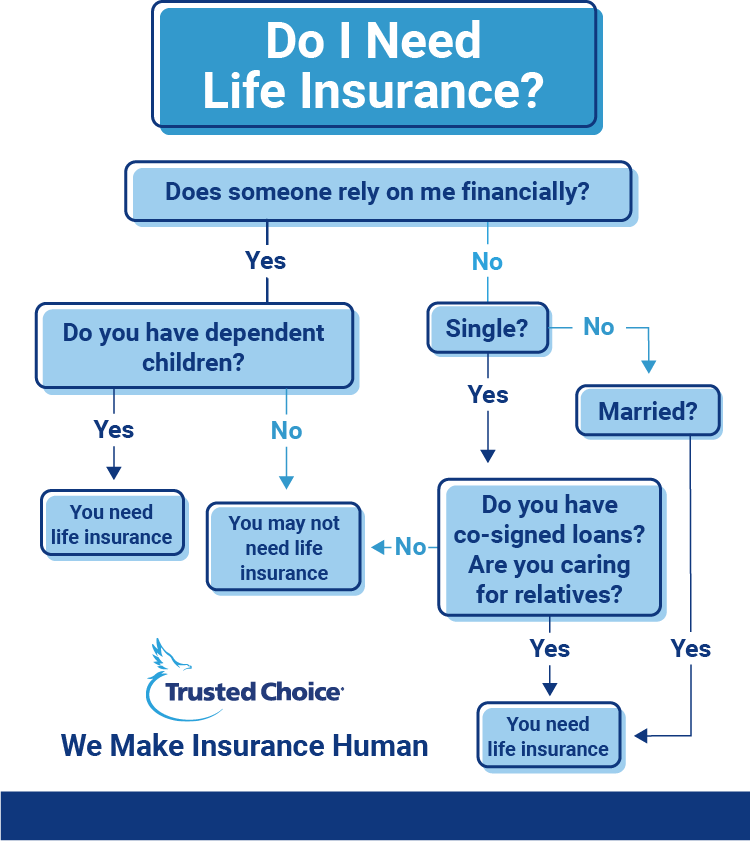

So, Do You Need It or Not? The Million-Dollar (or Maybe Just a Few Thousand-Dollar) Question

The answer, as with most things in life, is a resounding "it depends!" It’s like asking if you need a squirrel-proof bird feeder. Some people have no squirrels. Some people enjoy the squirrel chaos. And some people wage elaborate wars against the furry bandits. (I am firmly in the latter category).

Here are a few questions to ask yourself:

- What debts will my loved ones inherit? (Mortgage, loans, etc.)

- Will my spouse be financially secure without my income? (Even if they have their own retirement savings)

- Are there estate taxes to consider? (Talk to a financial advisor about this one – it can get complicated!)

- Do I want to leave a legacy for my family or a favorite charity? (Life insurance can be a tax-efficient way to do this)

- Am I currently paying for term or whole life insurance? (Term life insurance will eventually expire. Whole life insurance builds cash value and can be used later)

Ultimately, deciding whether to keep, reduce, or cancel your life insurance after retirement is a personal decision. There's no one-size-fits-all answer. It's best to sit down with a financial advisor (not your Uncle Bob who claims to be an expert after watching one YouTube video) and discuss your specific situation.

Get a professional opinion! They can help you assess your needs, weigh the pros and cons, and make an informed decision that will give you (and your loved ones) peace of mind. So go forth, conquer your finances, and maybe even buy yourself that gold toilet. You deserve it!