Which Credit Bureau Does Navy Federal Use For Home Loans

Alright, gather 'round, folks! Let’s talk about the super-secret, top-level intel… okay, maybe not that dramatic. But we are diving into the mysterious world of credit bureaus and, specifically, which one Navy Federal Credit Union (NFCU) prefers when you're trying to snag that dream home.

Imagine this: You’re finally ready to buy a house. You’ve been saving diligently, eating ramen every other night (okay, maybe most nights), and you’re picturing yourself sipping lemonade on your porch. Then comes the dreaded credit check. Dun dun DUNNN! Suddenly, your credit score is the star of a high-stakes drama.

And that leads us to the big question: Which credit bureau is playing judge, jury, and executioner (of your home-buying dreams, hopefully not!) when you apply for a mortgage with Navy Federal?

Must Read

The Credit Bureau Lineup: A Rogues’ Gallery (Sort Of)

First, a quick refresher. There are three major credit bureaus: Experian, Equifax, and TransUnion. They’re like the Three Musketeers, but instead of fighting for justice, they’re collecting data about your financial life. Think of them as friendly, but slightly nosy, accountants.

Each bureau keeps a separate record of your credit history, and sometimes those records disagree! It's like they're gossiping about you behind your back, and they can't even get the story straight. This is why it's super important to check your credit reports regularly. You wouldn't want some inaccurate parking ticket from 2008 ruining your chances of owning a castle (or, you know, a modest bungalow).

So, Which One Does Navy Federal Favor? The Big Reveal!

Here's the thing: Navy Federal, like most lenders, doesn't typically stick to just one credit bureau. They're not playing favorites! They usually pull your credit reports from all three – Experian, Equifax, and TransUnion. It's called a "tri-merge" credit report. Think of it as a three-way financial interrogation. (Don't worry, they're not that scary).

Why do they do this? Simple. They want the most complete picture of your creditworthiness. They want to see if you’re a responsible borrower or if you have a secret collection of late payments lurking in the shadows. It's like they're trying to solve a financial mystery, and they need all the clues they can get.

The Mortgage Credit Score: Not Just Any Old Score!

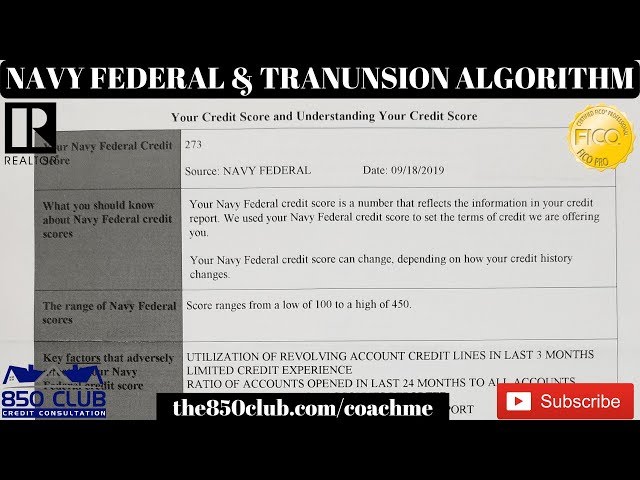

Now, this is where it gets a little…interesting. The credit score used for mortgages isn't usually the same one you see on Credit Karma or Mint. Those are often VantageScore models. Mortgage lenders usually use a FICO score, and specifically a different version of FICO than the ones you typically see. They are looking at older FICO scoring models. I know, it’s like a secret handshake only mortgage lenders know!

Pro-tip: Don't freak out if your FICO score from your credit card app doesn't match what the lender shows you. Mortgage lenders use specific FICO scoring models that consider their specific needs. It's like each industry has its own secret recipe for calculating your creditworthiness.

Why This Matters to You (Besides the Obvious House Thing)

Knowing that Navy Federal (and most lenders) pulls from all three bureaus is vital for a few reasons:

- Check all three reports: Make sure you check all three credit reports for errors before you apply for a mortgage. A single error can significantly impact your score. Think of it as weeding your financial garden before the inspector arrives.

- Address errors promptly: If you find any errors, dispute them immediately with the credit bureau. This can take some time, so start the process well in advance of your mortgage application. It’s like filing a formal complaint about the squirrels eating your petunias.

- Be patient: Credit scores fluctuate. Don't panic if your score dips slightly before you apply. Focus on maintaining good credit habits and avoid making any major financial moves that could negatively impact your score. Just keep calmly watering the plants (aka, making on-time payments).

The Bottom Line (And a Few Extra Giggles)

Navy Federal, like most mortgage lenders, pulls credit reports from all three major credit bureaus: Experian, Equifax, and TransUnion. They do this to get the most comprehensive view of your credit history. Make sure you check all three reports for errors and address any issues promptly.

And remember, don't let the credit check stress you out too much! Just imagine the lender is a friendly robot trying to help you achieve your dream of owning a house. (A robot who really, really cares about your credit score).

Now go forth and conquer the mortgage application process! And maybe treat yourself to some takeout. You deserve it after all that ramen.

Disclaimer: This information is for general knowledge and entertainment purposes only and should not be considered financial advice. Always consult with a qualified financial professional for personalized guidance.