What Is A Billing Cycle On A Credit Card

:max_bytes(150000):strip_icc()/billing-cycle-960690-color-v01-43af5d5ef90e46d6b3484e6900ba827a.png)

Ah, the trusty credit card! For many of us, it’s not just a piece of plastic; it’s a portal to convenience, a key to unlocking travel perks, and a builder of financial futures. Whether you're snagging loyalty points, making a spontaneous online purchase, or simply enjoying the security of not carrying cash, credit cards have woven themselves into the fabric of modern life, offering flexibility and, when used wisely, a powerful tool for managing money.

But behind every swipe and tap lies a fascinating financial rhythm that governs how your card operates: the billing cycle. Think of it as your credit card’s monthly heartbeat, a defined period where all your transactions are tallied up. Understanding this cycle isn't just about avoiding late fees; it's about mastering your money, maximizing benefits, and ensuring your financial health hums along smoothly.

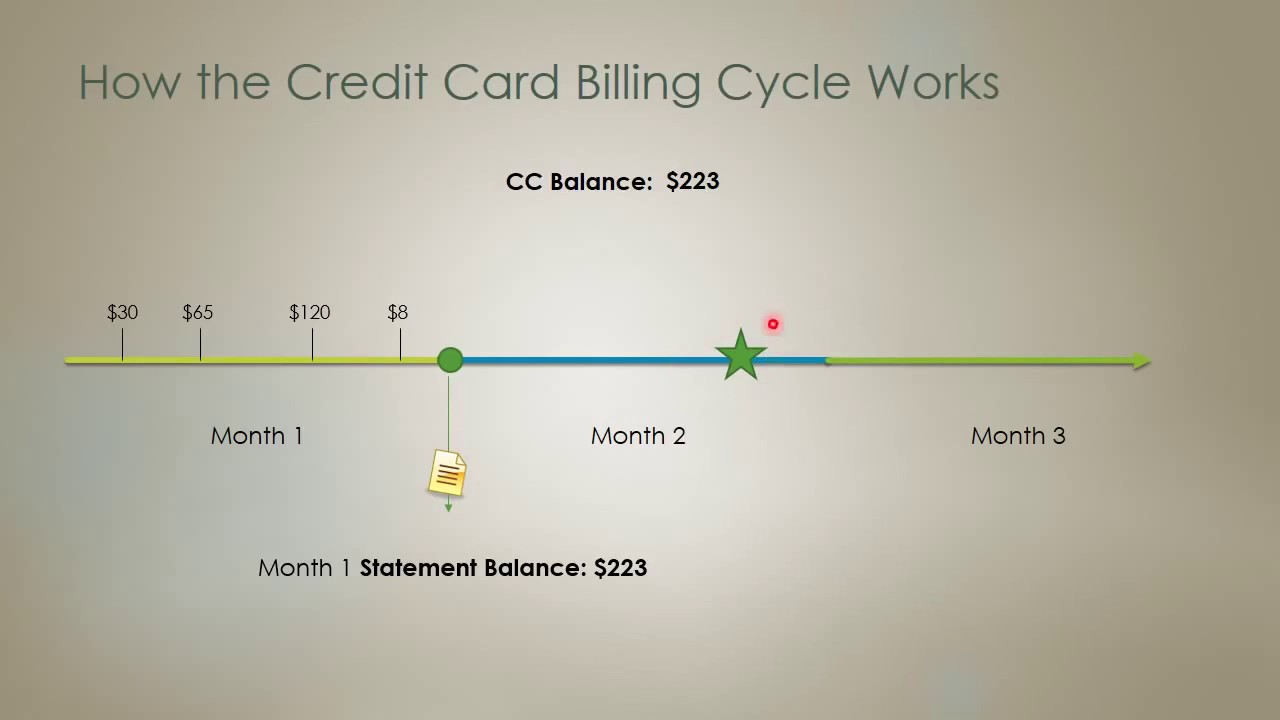

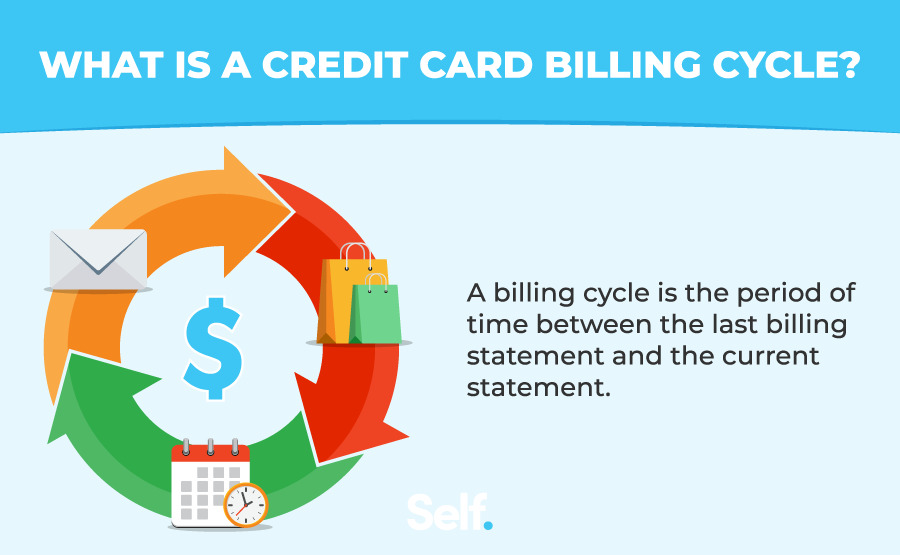

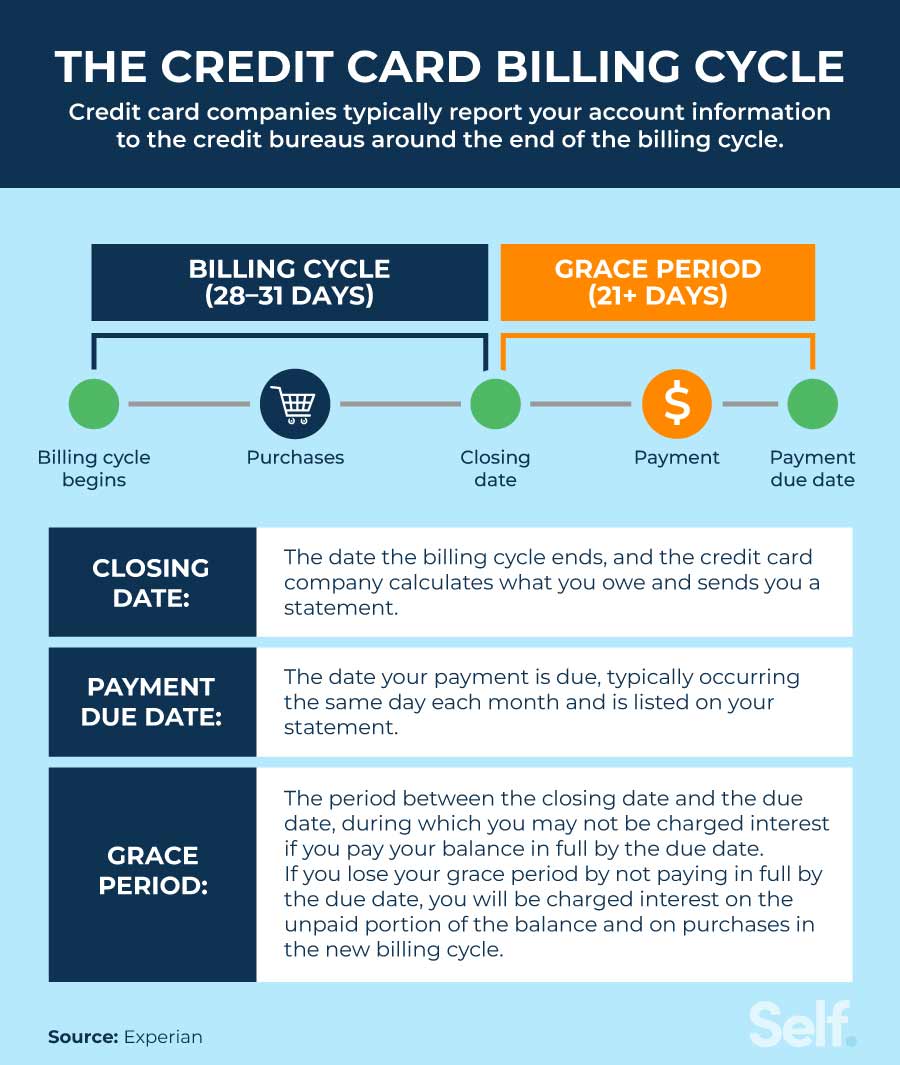

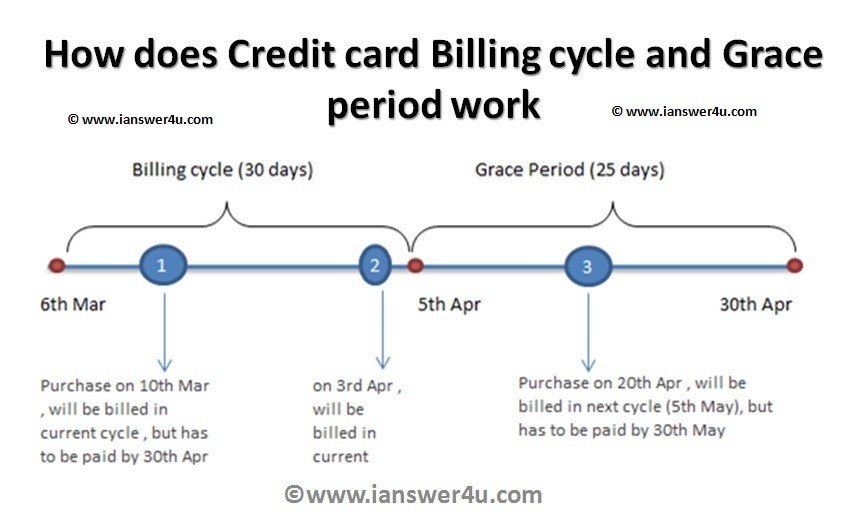

So, what exactly is a billing cycle? It's simply the time frame, usually between 28 and 31 days, during which your credit card issuer records all your purchases, payments, and other account activity. At the end of this cycle, a statement closing date arrives, signaling that your current statement (your bill!) is about to be generated. All activity up to this point will appear on that statement, and any transactions made after this date will roll over into your next billing cycle. A few weeks after your statement closes, you'll have your payment due date, which is the deadline to pay at least the minimum amount, or ideally, your full balance.

Must Read

The primary benefit of the billing cycle is to provide clarity and organization. Imagine having to pay for every single coffee or online shopping spree individually! Instead, the cycle consolidates everything into one neat monthly summary. More importantly, it provides the magical grace period. This is the precious window, typically from your statement closing date until your payment due date, where you can pay your entire balance without incurring a single cent of interest. This is crucial for using your credit card effectively as an interest-free period for short-term borrowing.

In everyday life, this means if your cycle runs from the 1st to the 30th of the month, your statement generated around the 30th will list all purchases made within those dates. If you buy a concert ticket on the 31st, it won't appear until your next month's statement. Common applications include planning large purchases. For example, buying new furniture early in your cycle gives you maximum time before the bill is due, potentially pushing the payment well into the next month.

To truly enjoy your credit card more effectively, become a billing cycle ninja! Here are some practical tips:

- Know Your Dates: Memorize your statement closing date and payment due date. Knowing when your cycle ends allows you to anticipate your bill.

- Pay in Full, Always: To fully leverage the grace period and avoid interest, aim to pay your full statement balance before the payment due date.

- Time Large Purchases: If you're planning a big expense, making it at the beginning of your billing cycle gives you the longest possible time to pay it off interest-free.

- Monitor Your Spending: Don't wait for the statement! Check your online account regularly within the cycle to track your spending and avoid surprises.

- Set Reminders: Use calendar alerts or set up auto-pay for your statement due date to ensure you never miss a payment and incur late fees or interest charges.

By understanding and strategically managing your credit card's billing cycle, you transform it from a mere payment tool into a powerful instrument for financial control, helping you save money, build credit, and enjoy all the perks your card has to offer.