What Happens If You Dont Use Your Credit Card

So, you've got a credit card, huh? That shiny piece of plastic promising rewards and convenience. But what if it just sits there, gathering dust in your wallet? What happens if you decide to completely ghost it?

The Great Credit Card Hibernation: A Hilarious Look

Let's dive into the (slightly dramatic) world of the unused credit card. We'll explore the potential outcomes, from the mildly annoying to the surprisingly beneficial. Prepare yourself, because it might not be as simple as you think!

The "Eh, Nothing Much" Scenario

In the best-case scenario, absolutely nothing dramatic happens. Your card simply remains inactive. Think of it like a tiny plastic bear going into hibernation – waiting for its chance to shine again.

Must Read

You might still receive statements, showing a big, beautiful balance of $0.00. It's kind of like winning a participation trophy, isn't it?

The Case of the Vanishing Credit Limit

Now, things can get a little spicier. The most common consequence? The dreaded credit limit reduction. Imagine this: you signed up for a card with a $5,000 limit, picturing yourself buying that giant inflatable flamingo for the pool. Then, poof, it's shrunk to $2,000!

Why? Because the issuer figures you don't need all that credit if you're not using it. They might reallocate it to someone who will actually swipe that card with gusto!

It’s like having a gym membership you never use. Eventually, the gym might wonder if you're still committed. (Spoiler: they probably won't cancel you, but your credit card issuer might!).

The Account Closure Calamity!

Okay, this is where things get serious (but still kind of funny in a morbid way). If your card remains unused for a very long time, the issuer might just close the account. Consider it the ultimate form of credit card ghosting – they're ghosting you back!

This typically happens after a year or more of inactivity. You'll get a notice beforehand, so it's not like they'll just pull the plug without warning.

Imagine your credit card company sending a breakup text. "It's not me, it's you. We need someone who's actually going to use us." Ouch!

The Credit Score Conundrum

Here's the part everyone worries about: your credit score. Will your score plummet into the abyss if you don't use your credit card? The answer is nuanced, but generally, probably not catastrophically.

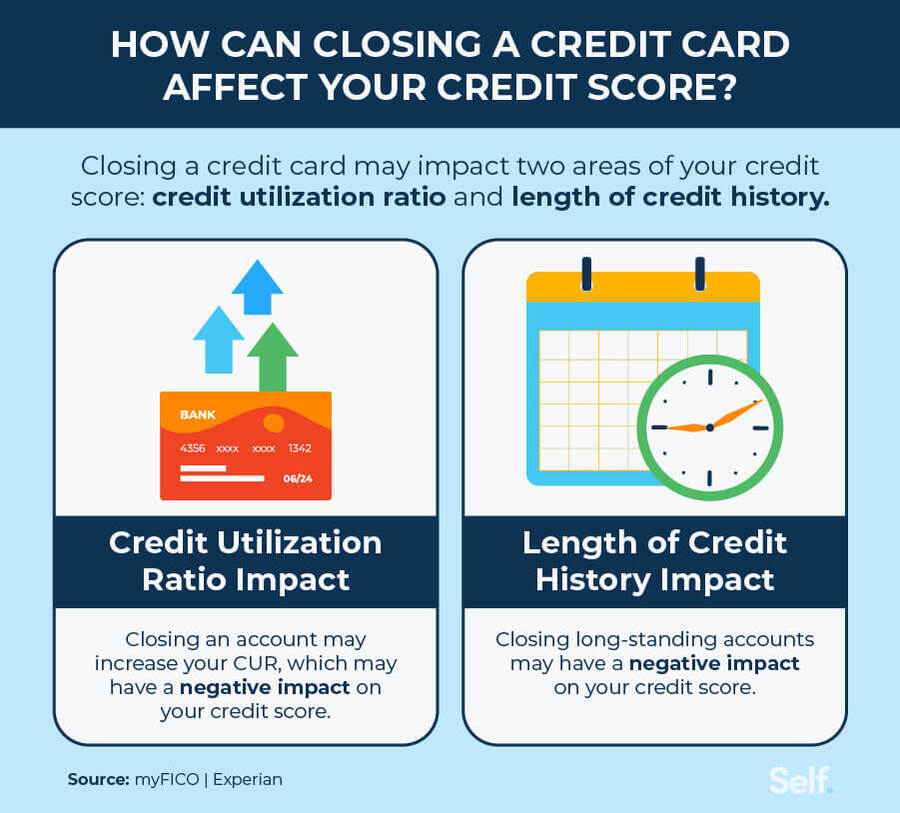

Closing a credit card can impact your credit utilization ratio, which is a significant factor in your credit score. Let's say you have two cards, each with a $5,000 limit. That's $10,000 of available credit. If one card is closed, you're down to $5,000.

If you're carrying a balance on the remaining card, your credit utilization ratio just increased. Higher utilization can negatively affect your score. Think of it as carrying all your eggs in one basket – a bit risky, right?

However, if you have other active credit accounts and keep your overall credit utilization low, the impact might be minimal. It's like losing one sock in the laundry – annoying, but not the end of the world.

The Rewards Redemption Regression

Many credit cards offer tempting rewards – cash back, travel points, airline miles, the whole shebang! If you're not using your card, you're missing out on these sweet perks.

Imagine all those missed opportunities for free flights, discounted hotels, or just plain old cash in your pocket. It's like having a winning lottery ticket and forgetting to cash it in! Tragic, I tell you, tragic!

Those rewards could be funding your next vacation, upgrading your gadgets, or treating yourself to something special. Don't let them go to waste!

The Annual Fee Fiasco

Some credit cards come with annual fees. If you're paying an annual fee for a card you're not using, you're essentially throwing money away. It's like subscribing to a magazine you never read – a total waste!

Consider canceling the card or downgrading to a no-fee version. There are plenty of great no-annual-fee cards out there that can still help you build credit and earn rewards.

Do a cost-benefit analysis! If the fees outweigh the perks, it's time to ditch the dead weight.

The Missed Opportunity Mayhem

Beyond rewards, using a credit card responsibly can help you build a solid credit history. A good credit score opens doors to better interest rates on loans, mortgages, and even insurance.

By not using your card, you're missing out on the chance to demonstrate your responsible credit management skills. It's like skipping class – you might miss out on valuable lessons.

Think of it this way: a healthy credit score is like a superpower that unlocks financial opportunities. Why wouldn't you want that?

The Fraudulent Activity Fun

Okay, this might seem counterintuitive, but not using your card can actually make you more vulnerable to fraud. Why? Because you're less likely to check your statements regularly.

If someone steals your card information and makes unauthorized purchases, you might not notice it right away. The longer it goes unnoticed, the more damage they can do.

Even if you're not using your card, make it a habit to check your statements online or through your bank's app. It's a quick and easy way to spot any suspicious activity.

The Card Network Cancellation Caper

In rare cases, the card network itself (Visa, Mastercard, American Express, Discover) might discontinue the card program. This is usually due to low usage rates or changes in the issuer's strategy.

You'll be notified if this happens, and you'll likely be offered a replacement card. However, it's still a hassle to deal with.

Think of it like your favorite restaurant closing down – disappointing, but there are always other options.

The Grand Finale: Credit Card Comeback Strategies

So, what if you've realized your credit card has been neglected? Fear not! There are ways to revive it and avoid the negative consequences.

The Small Purchase Solution

The easiest way to keep your card active is to use it for small, recurring purchases. Think your morning coffee, your streaming subscriptions, or your weekly groceries.

Just make sure you pay off the balance in full each month to avoid interest charges. It's like giving your credit card a little workout to keep it in shape.

The Automatic Payment Power-Up

Set up automatic payments for bills you already pay each month. This ensures your card is used regularly without you having to think about it. It's like putting your credit card on autopilot!

Just be sure to monitor your account to ensure the payments are going through correctly. And, you know, that you actually have the money to cover the bill.

The Rewards Redemption Ritual

Don't let those hard-earned rewards expire! Make it a ritual to redeem them regularly. Whether it's for cash back, travel points, or gift cards, treat yourself!

It's like celebrating your financial success with a little reward. You deserve it!

The Communication Consideration

If you're planning on not using your card for a while, consider contacting the issuer and letting them know. This might help prevent them from closing your account due to inactivity.

It's like telling your friend you're going off the grid for a bit – they'll appreciate the heads-up.

The Closure Consideration

If you're not using your card and don't plan to use it in the future, consider closing the account. Just be mindful of the potential impact on your credit score, especially if it's one of your oldest accounts.

It's like Marie Kondo-ing your wallet – if it doesn't spark joy (or provide value), let it go!

The End (But Your Credit Card Journey Isn't!)

So, there you have it – a humorous (and hopefully informative) look at what happens if you don't use your credit card. Remember, responsible credit card usage can be a powerful tool for building wealth and achieving your financial goals.

Don't let your credit card turn into a forgotten relic. Give it some love (and responsible spending), and it will reward you in return!

Now go forth and conquer your credit card kingdom! Just don't buy that giant inflatable flamingo... unless you really, really want it.