Primary Paid More Than Secondary Allowed Amount

Hey everyone! Ever looked at a medical bill and thought, "Wait, what even IS this?!" Don't worry, you're not alone. Healthcare billing can be seriously confusing. Today, let's dive into something that might sound like a typo at first: when the primary insurance actually pays more than the secondary insurance allowed. Sounds weird, right? Let's unravel this mystery!

What's "Allowed Amount" Anyway?

First things first, let's get our terms straight. The "allowed amount," also known as the "contractual adjustment" or "negotiated rate," is the amount your insurance company has agreed to pay a doctor or hospital for a specific service. Think of it like this: you wouldn't just walk into a car dealership and pay whatever price they slap on the window, would you? No way! You'd expect them to negotiate, right? Insurance companies do the same thing. They bargain with providers to get a better price for their members.

This allowed amount is often lower than the doctor's initial charge. So, your insurance company pays this lower agreed-upon price, and you're usually responsible for your deductible, copay, or coinsurance – the portion you agreed to pay. Makes sense, right?

Must Read

Primary vs. Secondary Insurance: The Tag Team

Now, imagine you have two insurance plans. This isn't as rare as you might think! Maybe you're covered under your own plan and also your spouse's, or perhaps you have Medicare and a supplemental plan. In these cases, one plan is designated as "primary" and the other as "secondary."

The primary insurance pays first. They process the claim as if they were the only insurance involved. Then, whatever's left over gets sent to the secondary insurance. The secondary insurance is supposed to pick up some or all of the remaining costs, depending on the plan.

Think of it like a relay race. The primary insurance runs the first leg, and then hands off the baton (the remaining bill) to the secondary insurance to finish the race.

The Plot Thickens: Primary Pays MORE?

Okay, so here’s where it gets interesting. How can the primary insurance pay more than the secondary insurance's allowed amount? Isn't that backwards?

The key lies in the contracts each insurance company has with the healthcare provider. Each insurance company negotiates its own rates. It's entirely possible, even common, for one insurance company to have negotiated a better rate than another for the same service.

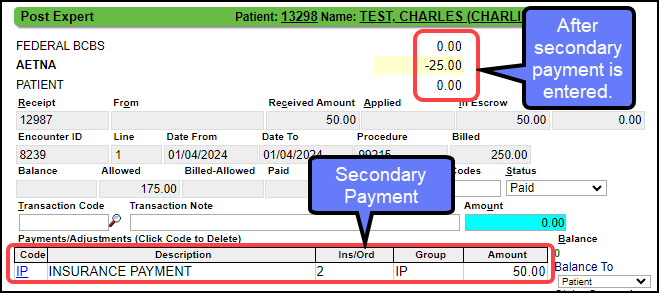

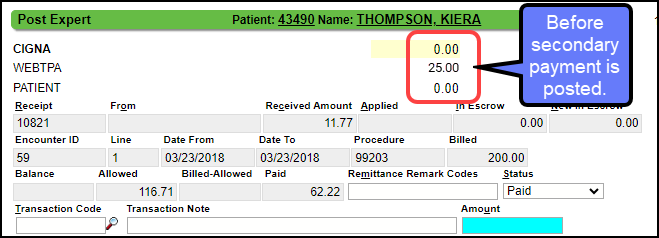

Let's say you go in for a check-up. Your primary insurance (let's call them "Insure-Awesome") has a fantastic deal with your doctor. They've negotiated an allowed amount of $100. Your secondary insurance ("Medi-Meh"), on the other hand, has a less stellar deal; their allowed amount for the same check-up is $80.

Insure-Awesome pays the $100 (minus your copay, of course). Then, the remaining balance gets sent to Medi-Meh. Medi-Meh can't pay more than their allowed amount of $80. In this scenario, the remaining balance might be small enough that Medi-Meh only pays a tiny bit or even nothing!

Why This Isn't a Problem (And Might Even Be Good!)

At first glance, this might seem like the system is broken. But it's not necessarily a bad thing. Here's why:

*You're still protected. Even though the secondary insurance might not pay much (or anything), you're not on the hook for the difference between the primary insurance's payment and the doctor's original charge. That's because of the negotiated rates. The provider has agreed to accept the allowed amount from each insurance company.

It highlights the complexity of healthcare pricing. This situation shines a light on how different insurance companies negotiate different rates. It's a reminder that healthcare pricing isn't always straightforward.

*It could save you money. Depending on your plan's coordination of benefits, the primary insurance covering more upfront could result in a lower out-of-pocket cost for you. Every plan is different!

Decoding Your EOB

So, how can you spot this on your Explanation of Benefits (EOB)? Look for these clues:

Compare the "Allowed Amount" on both EOBs. See if the primary insurance's allowed amount is indeed higher.

*Check the "Patient Responsibility" section. This is the most important part! As long as this number is reasonable and aligns with your plan's cost-sharing provisions (deductible, copay, coinsurance), you're likely in the clear.

The Takeaway? Stay Curious!

Healthcare billing is definitely a maze, but understanding even a little bit can empower you. Don't be afraid to ask questions! Call your insurance company if something doesn't make sense. Remember, knowing what to look for can save you time, stress, and potentially even money. And who doesn't want that?

So, next time you see the primary insurance paid more than the secondary's allowed amount, don't panic. It's just another quirky piece of the healthcare puzzle. And now, you’re one step closer to solving it!