Is Capital One Good To Build Credit

Hey, so you're wondering if Capital One is any good for building credit, huh? Like, is it a secret weapon or just another piece of plastic cluttering your wallet? Let's spill the tea (or, you know, the coffee).

First things first: building credit is like training for a marathon. It takes time, patience, and maybe a few blisters (metaphorically speaking, of course! Unless you’re really into marathons). There's no magic wand, no instant "Credit Score: Awesome!" button.

Capital One: The Contender

Capital One does have a reputation for being friendly to people who are just starting out or trying to rebuild their credit. Think of them as the approachable, supportive coach in your credit-building journey. But are they the best? Well, that depends on you, doesn't it?

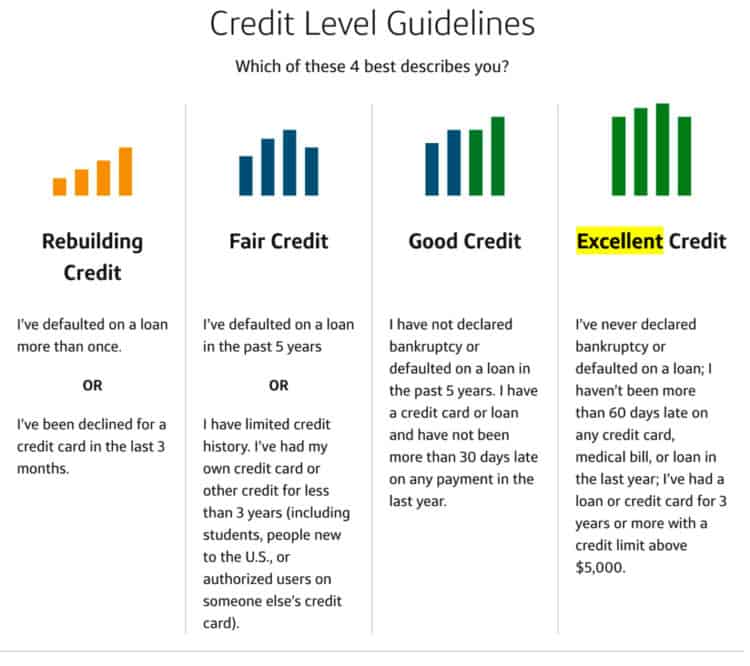

Must Read

Here's the lowdown: Capital One offers a range of cards designed for different credit levels. We're talking secured cards, cards for students, and even cards for those with "fair" credit (which basically means you've stumbled a few times, but you're getting back up!).

Secured cards are usually the easiest to get approved for. You put down a security deposit (like, say, $200), and that becomes your credit limit. It's like telling Capital One, "Hey, I promise I'll pay, here's some collateral!" They feel safer, you get a chance to prove yourself, and everyone wins… hopefully.

But here’s the kicker: using a secured card responsibly is KEY. I mean, seriously, SUPER KEY. Pay your bills on time, every time. Don't max out your credit limit (keep it way below, like under 30%). Treat it like real money, because, well, it is real money! And it directly impacts your credit score.

The Perks (and Potential Downsides)

One awesome thing about Capital One (and many credit card companies, to be fair) is that they often report your payment activity to the three major credit bureaus: Experian, Equifax, and TransUnion. This is crucial. It's like shouting your good credit habits from the rooftops so everyone knows how responsible you are!

Now, for the potential downsides. Not all Capital One cards are created equal. Some have higher interest rates than others. And some of their beginner cards, while easy to get approved for, might not offer the fanciest rewards or perks. So, shop around, compare offers, and read the fine print (yes, I know, it's boring, but trust me on this!).

Are you comparing apples to apples? A fancy rewards card with sky-high interest is pretty useless to you if you carry a balance all the time, right? It's like buying a Ferrari and then realizing you can't afford the gas.

So, Is It a Good Idea?

Okay, let's cut to the chase. Can Capital One help you build credit? Absolutely. Is it the only option? Nope. There are plenty of other fish in the sea (or, you know, credit card companies in the financial world).

Here's my advice:

- Do your research. Compare different Capital One cards and other credit card options.

- Know your credit score. This will help you understand what kind of cards you're likely to be approved for.

- Be responsible. Pay your bills on time and keep your credit utilization low. It's the golden rule of credit building!

Think of a Capital One card (or any credit card for that matter) as a tool. Used wisely, it can help you achieve your credit goals. Used irresponsibly, it can… well, you know. Credit card debt is no fun. Believe me.

Ultimately, building credit is a marathon, not a sprint. But with a little knowledge, some discipline, and maybe a decent cup of coffee (because who can function without caffeine?), you'll be well on your way to a better credit score. You got this!