How Long It Takes To Get A Loan Approved

So, you're thinking about getting a loan? Maybe it's for that adorable fixer-upper with the overgrown rose bushes and questionable plumbing. Or perhaps it's to finally conquer that mountain of student debt. Whatever the reason, a tiny voice in the back of your head is probably whispering, "How long is this going to take?"

The truth? Getting a loan approved can feel like watching paint dry...sometimes. Other times, it's like a rollercoaster – a thrilling, stomach-dropping ride with unexpected twists and turns. There's no one-size-fits-all answer, but let's break down the journey and sprinkle in some humor along the way.

The "I Want It Now!" Stage (aka Application)

First, you need to apply. Think of this as the opening act in your loan approval drama. You're essentially telling the lender, "Hey! I'm a responsible adult (mostly), and I need some cash!" This usually involves filling out forms – online or in person – that ask about your income, employment history, credit score (gulp!), and what you plan to do with the money.

Must Read

This part can be quick. If you're organized and have all your documents ready (pay stubs, bank statements, driver's license – the whole shebang), you can zip through the application in an hour or two. However, if you're like me and your "organized" system involves a stack of papers threatening to topple over, well, grab a coffee. You'll need it.

Expect a lender to ask you for a million documents just to prove that you are who you are. They need the original birth certificate (with a note from your mother stating that she confirms that it's your birth certificate) plus a notarized letter from your dog. Ok, maybe not that much.

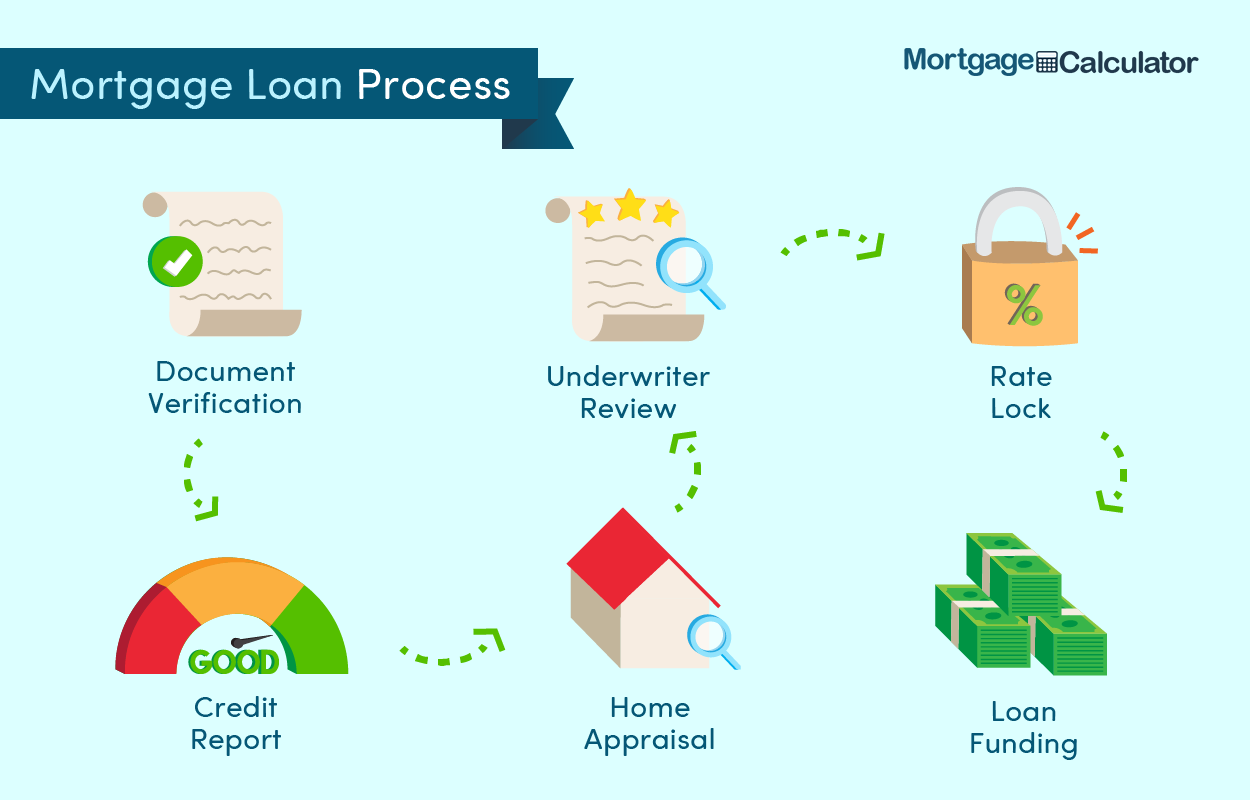

The Waiting Game (aka Underwriting)

Once you've submitted your application, it vanishes into the mysterious land of underwriting. This is where the lender's team of financial detectives scrutinizes your information, verifies your employment, and assesses your creditworthiness. They're basically trying to figure out if you're a good risk or if lending you money is like throwing it into a bonfire.

This stage is often the biggest time suck. For a simple personal loan, it might take a few days to a week. For a mortgage? Buckle up. We're talking weeks, maybe even a month or more! Home buying can be stressful. So you might want to invest in some stress balls or a punching bag.

During underwriting, be prepared for the dreaded "Request for More Information" email. This usually comes at the worst possible time, like when you're on vacation or stuck in a meeting. They might need clarification on a small detail, an extra document, or even just a signed statement explaining why you bought a year's supply of gummy bears last month. (Hey, no judgement!)

The "All Clear!" (aka Approval)

Finally, the moment you've been waiting for! The lender says, "Yes! We approve your loan!" Cue the confetti (optional, but highly encouraged). You'll receive a loan agreement outlining the terms, interest rate, and repayment schedule. Read it carefully! This is where you discover if you're actually getting a decent deal or if you're about to be paying back your loan until the next ice age.

Once you sign the agreement, the funds are usually disbursed within a few business days. And just like that, you have the money you need!

Things That Can Speed Things Up (or Slow Them Down)

Several factors can affect the loan approval timeline. A squeaky-clean credit history and a stable income will make the process smoother. On the other hand, a messy credit report, frequent job changes, or a large amount of debt can raise red flags and cause delays.

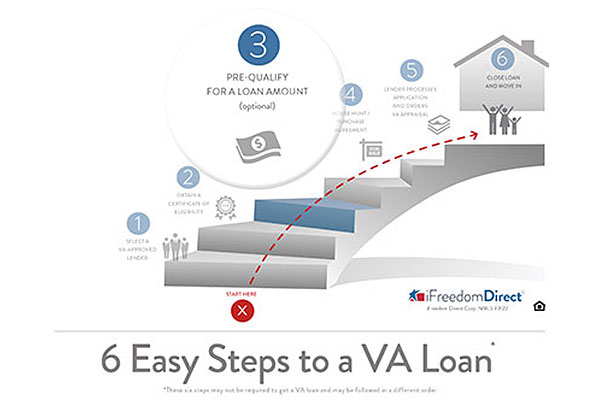

The type of loan also matters. Simple personal loans are typically faster to approve than mortgages, which involve appraisals, title searches, and a whole host of other complexities. Also, the lender's workload can impact processing times. A small, local credit union might be quicker than a large, bureaucratic bank.

Ultimately, getting a loan approved is a waiting game. But with a little patience, a healthy dose of humor, and a willingness to provide the lender with whatever information they need (even that explanation for the gummy bears), you'll eventually reach the finish line. And who knows? Maybe you'll even learn a thing or two about your own finances along the way.