How Do I Correct Information On My Credit Report

Hey friend! Ever feel like your credit report is speaking a foreign language? Or maybe it's just… wrong? Don't panic! Correcting errors is totally doable. And hey, it's kinda fun, like detective work!

Why Bother? (Besides the Obvious)

Okay, first things first: why even care? Well, a wonky credit report can mess with your loan applications. Think higher interest rates on your dream car. Or even getting approved for that sweet apartment downtown. Yikes!

But here's a quirky fact: did you know some landlords also check your credit? Yep! Good credit can literally unlock doors. (And not just your front door!)

Must Read

Also, imagine this: you're denied a job because of a mistake on your report. Seriously uncool. Fixing errors can protect your reputation and your future. Plus, it's just plain satisfying to get things right!

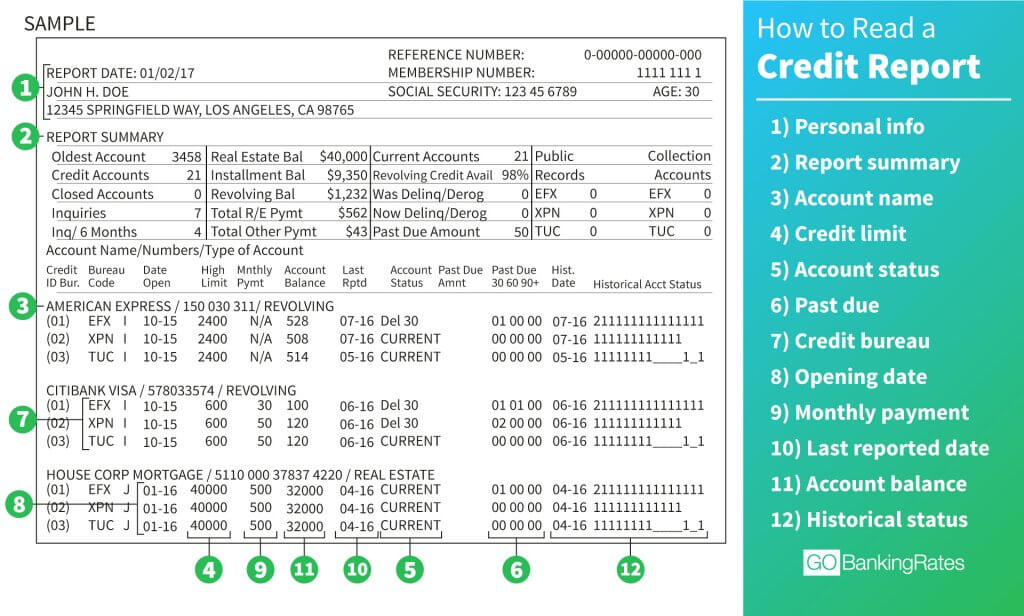

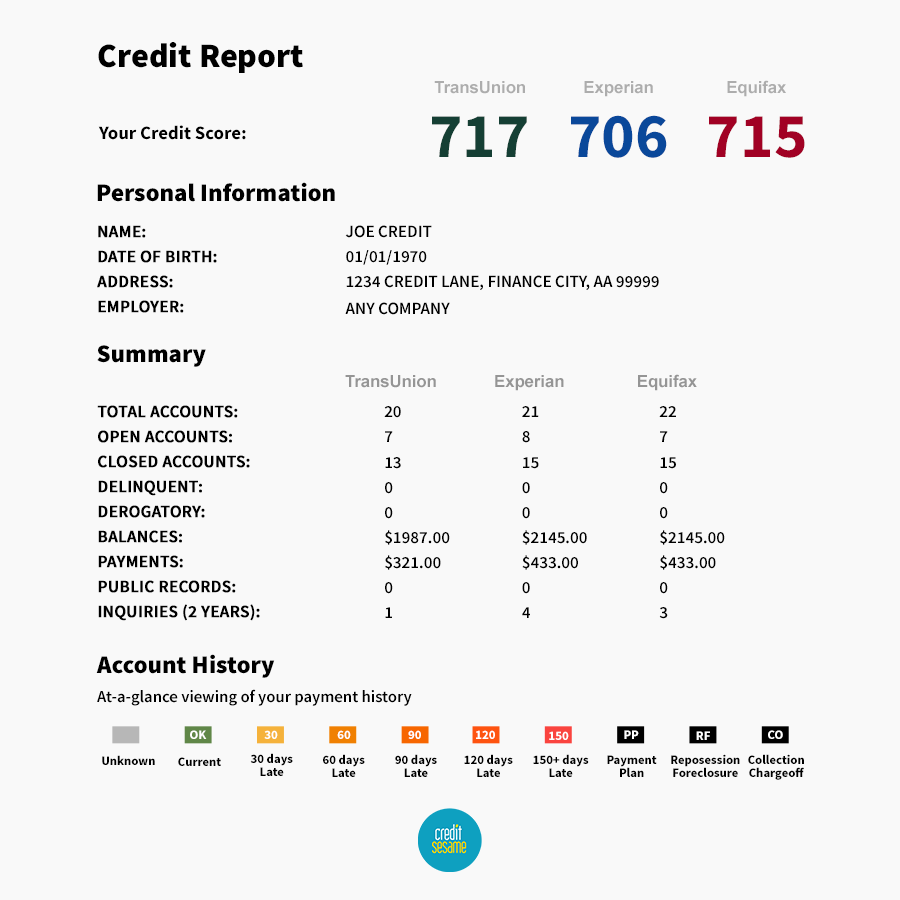

Spotting the Culprit: Your Credit Reports

Time to Sherlock Holmes this thing! You need to snag copies of your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. Why all three? Because they might each have slightly different information. Sneaky, right?

The government actually mandates that you can get a free credit report from each bureau once a year at AnnualCreditReport.com. Mark your calendar! It's like Christmas, but with less glitter and more financial responsibility. Bonus!

Look. Closely. Are there accounts you don't recognize? Addresses where you've never lived? A misspelled version of your name (like "Jonh" instead of "John")? Those are red flags, my friend. Treat them like the villain in a movie – we're about to take them down!

The Battle Plan: Disputing the Error

Found something fishy? Time to dispute it! Think of this as writing a polite but firm "strongly worded letter" to the credit bureau. Be clear and concise.

You can usually file a dispute online, which is super convenient. Each credit bureau has a dedicated page for this. Find it, bookmark it, conquer it! Or, if you're feeling old-school, you can send a letter via snail mail. Make sure to keep a copy for your records.

What should you include? Here's the rundown:

- Your full name (as it appears on your credit report).

- Your address (current and any previous ones).

- Your date of birth.

- The specific error you're disputing. (Be precise! "Incorrect account" isn't enough. Say "Account number 123456789 shows a balance of $500, but it's actually been paid off.")

- Why you believe the information is incorrect. ("I paid this account in full on January 1, 2024, and I have attached a copy of my bank statement as proof.")

- Copies of any supporting documents (bank statements, cancelled checks, etc.).

Pro tip: Don't send originals! Send copies and keep the originals safe and sound. You never know when you might need them again.

The Waiting Game (Ugh!)

Okay, you've sent your dispute. Now comes the hard part: waiting. The credit bureaus have 30 days (sometimes 45, depending on the situation) to investigate. I know, it feels like forever! But trust me, it's worth it.

During this time, they'll contact the creditor (the company that reported the information) to verify the details. The creditor will then have to provide evidence to support their claim. It's like a financial showdown at the OK Corral!

The Verdict: Success or Round Two?

Finally! The moment of truth. The credit bureau will notify you of the results of their investigation. Hooray! If they agree with you, they'll update your credit report. Victory is yours!

But what if they disagree? Don't despair! You have options.

- You can ask the creditor directly to correct the information.

- You can add a 100-word statement to your credit report explaining your side of the story. It's your chance to set the record straight!

- You can even consider filing a complaint with the Consumer Financial Protection Bureau (CFPB). They're like the superheroes of consumer finance!

Repeat as Needed!

Remember, your credit report is a living document. It's constantly changing as you use credit. So, it's a good idea to check it regularly – at least once a year. Think of it as a financial health check-up.

Correcting errors on your credit report might seem daunting, but it's an important part of taking control of your financial life. Plus, who doesn't love a good detective story? So go forth, be vigilant, and conquer those credit report gremlins!