How Accurate Is Kikoff Credit Score

Let's talk about Kikoff. Specifically, the Kikoff credit score. You've probably seen the ads. Promises of boosting your score without, you know, actually using credit cards.

Sounds too good to be true? Maybe, just maybe, it kinda is. But don't @ me yet!

The Hype vs. The Reality

Kikoff basically works by reporting a line of credit. You make small, regular payments. This, in theory, builds your credit history. Seems simple enough, right?

Must Read

Here's my unpopular opinion: The credit score boost you get from Kikoff might not be exactly what you expect.

Think of it like this. It's like learning to ride a bike with training wheels. You're technically riding, but...it's not the real deal.

The Credit Bureau Lowdown

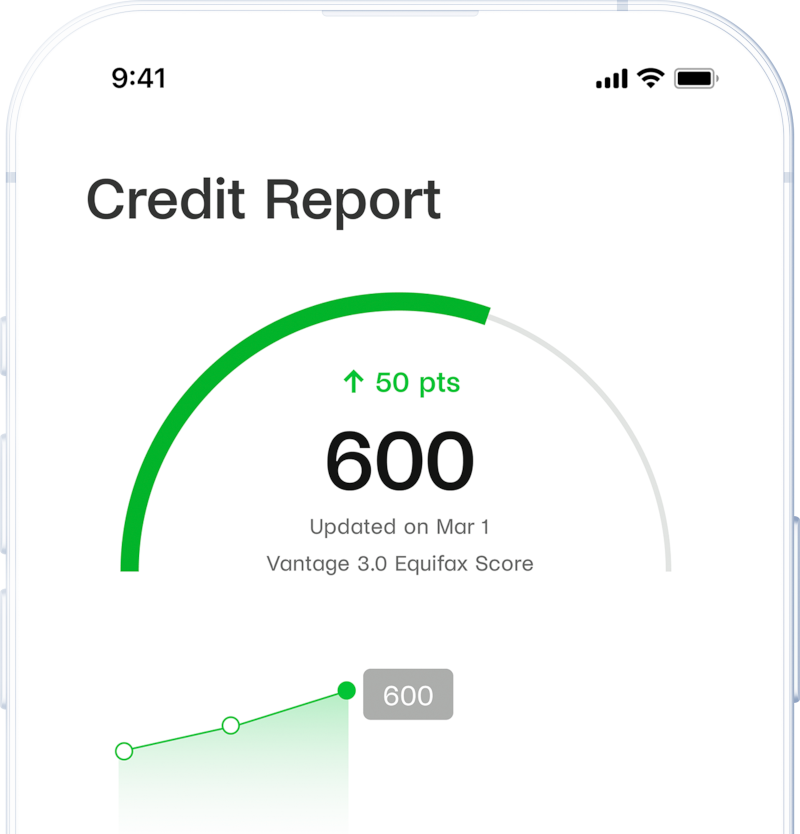

Kikoff reports to Equifax and Experian. Good news, definitely! These are the two of the big three credit bureaus.

But here's the thing. Not all credit scores are created equal. The score Kikoff shows you might not be the exact score a lender sees.

Lenders use different versions of credit scores. They might also weigh factors differently. So that sweet bump you see on Kikoff? It's more like a guideline.

The "Authorized User" Effect

Ever been an authorized user on someone else's credit card? It's similar to the Kikoff effect. Your score might go up, sure. But is it really your credit history?

Think of it like borrowing someone's nice shoes. You look good for the night. But they aren't your shoes, are they?

Kikoff helps build a credit history. It does so by letting you make on-time payments and reports it to the bureaus.

So, Is Kikoff Worth It?

Okay, okay, I'm not saying Kikoff is useless. Not at all! For some people, it can be a good starting point. Especially if you have limited or no credit history.

It's like planting a tiny seed. You need something to start, right?

But let's be realistic. Kikoff alone probably won't get you that dream mortgage. Sorry to burst your bubble. You need to show you can handle real credit.

Beyond Kikoff: The Real Credit Game

Want to really impress lenders? Get a secured credit card. Use it responsibly. Pay it off on time. Every. Single. Month.

That's the magic formula. It's not sexy. It's not instant. But it works.

Building credit is like building a house. You need a solid foundation and a well-thought-out plan. Not just a shiny coat of paint.

The Kikoff Score vs. The FICO Score

Another thing to consider. Kikoff often shows you a VantageScore. While its good to monitor any score you have, most lenders use FICO scores.

So, while your VantageScore might be soaring, your FICO score might be a bit…more grounded.

It's like comparing apples and oranges. Both are fruit, but they taste different. And lenders prefer the taste of FICO apples.

My "Controversial" Conclusion

Kikoff is a tool. A decent tool. But it's not a magic wand. Don't rely on it as your only credit-building strategy.

It's like having a single wrench in your toolbox. Useful for some things, but not everything.

Use Kikoff as part of a broader plan. Be smart. Be responsible. And remember, building credit is a marathon, not a sprint. And consider paying off any credit card debt as soon as possible.

Do your research. Understand the difference between VantageScore and FICO. Don't just rely on the credit score you see on an app. Knowledge is power, my friends!

And maybe, just maybe, get a real credit card. You know, the kind that lets you buy stuff and then pay it back. Wild concept, I know.

Good luck out there in the wild world of credit! Remember to be smart and not just listen to some internet dude's advice.

Think of building credit like leveling up in a game. You need to complete quests (responsible credit use) and defeat bosses (debt). Kikoff might give you a small XP boost, but you still gotta put in the work!