Fannie Mae Freddie Mac Fees Legislation

Okay, folks, let's talk mortgages! I know, I know, usually the word "mortgage" is enough to send shivers down your spine, but trust me, this is actually… well, not thrilling, but definitely something you should know about. We're diving into the world of Fannie Mae, Freddie Mac, and some shiny new legislation that could affect your wallet when you're buying a home!

Fannie, Freddie, and the Fee Fiesta

So, picture this: Fannie Mae and Freddie Mac are like the friendly giants of the mortgage world. They don't actually give out loans directly. Instead, they buy mortgages from banks and other lenders, which keeps those lenders happy and flush with cash to, you guessed it, lend to more people! It's like a mortgage merry-go-round that keeps spinning (hopefully not too fast!). To make this merry-go-round work, they charge fees. Think of them as admission tickets to the housing amusement park. These fees help them cover their costs and ensure they can keep buying mortgages, keeping the whole housing market humming along.

The Fee Frenzy: What Are We Talking About?

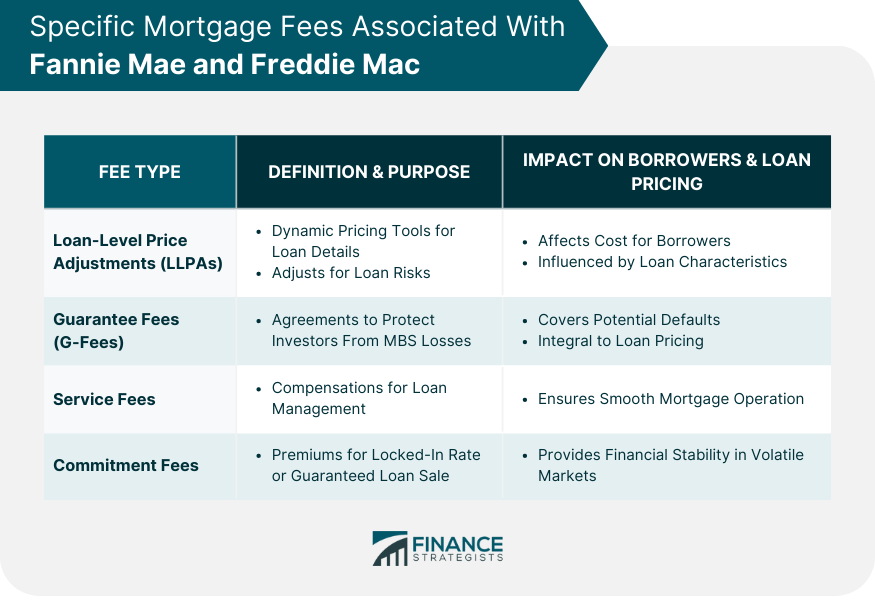

Now, these fees, they go by different names, like guarantee fees (or "g-fees" for short – because everything needs an abbreviation, right?). They're basically a percentage of your loan amount. Even a tiny percentage can add up to a pretty penny over the life of a 30-year mortgage. We're talking potentially thousands of dollars! Imagine finding that extra cash – maybe a vacation to Fiji, a new jacuzzi, or enough pizza to feed a small army. Okay, maybe not a whole army, but definitely a squad!

Must Read

Legislation to the Rescue? Maybe…

Here's where things get interesting. The government, in its infinite wisdom, has been tinkering with these fees. There's talk of new legislation aimed at making homeownership more affordable. The goal? To help more people, especially first-time homebuyers, achieve the dream of owning their own little slice of paradise (or, you know, a condo in the suburbs).

But here's the thing: like a perfectly cooked soufflé, balancing the mortgage market is a delicate art. Some people argue that tinkering with these fees too much could have unintended consequences. Raising fees on some loans could make them more expensive, while lowering them on others could benefit some buyers at the expense of others. It's a real "robbing Peter to pay Paul" situation, and nobody wants to be Peter! (Unless Peter really likes being robbed, which, let's be honest, is unlikely).

What Could This Mean for You?

So, what does all this fee-talk mean for you, the aspiring homeowner? Well, if the legislation leads to lower fees, you could save a significant amount of money on your mortgage. That's money that could go towards decorating your new digs, buying a really, really big TV, or, you know, responsibly paying down your mortgage faster. But remember, the mortgage landscape is constantly shifting, so it's crucial to stay informed. The best thing you can do is talk to a qualified mortgage professional who can explain the current fees and how any new legislation might affect you.

Think of it like this: navigating the mortgage world is like trying to bake a cake without a recipe. You might end up with something edible, but it's probably going to be a bit of a mess. A good mortgage professional is like having a master baker guiding you through the process, ensuring you end up with a delicious and financially sound result.

The Bottom Line (and a sprinkle of optimism!)

The future of Fannie Mae, Freddie Mac, and their fees is still a bit uncertain. But one thing is for sure: this is something to pay attention to. Keep an eye on the news, talk to your lender, and don't be afraid to ask questions. After all, buying a home is a huge investment, and you deserve to be well-informed. And who knows, maybe this new legislation will be the key to unlocking the door to your dream home, filled with sunshine, laughter, and maybe even that jacuzzi you've always wanted!

So, chin up, buttercup! The housing market can be a wild ride, but with a little knowledge and a dash of optimism, you can navigate it like a pro. Now go forth and conquer that mortgage mountain!