Does Homeowners Insurance Cover Theft

Ever had that sudden, gut-wrenching thought: "What if someone breaks in?" It’s a fear most homeowners face, a fleeting image of your cozy sanctuary disrupted. Beyond the emotional stress, there's the very practical question of what happens to your precious belongings. Does your homeowners insurance actually have your back when sticky fingers pay an unwelcome visit? Let's dive in, because understanding this can truly offer some much-needed peace of mind.

Good News First: The Short Answer is Usually Yes!

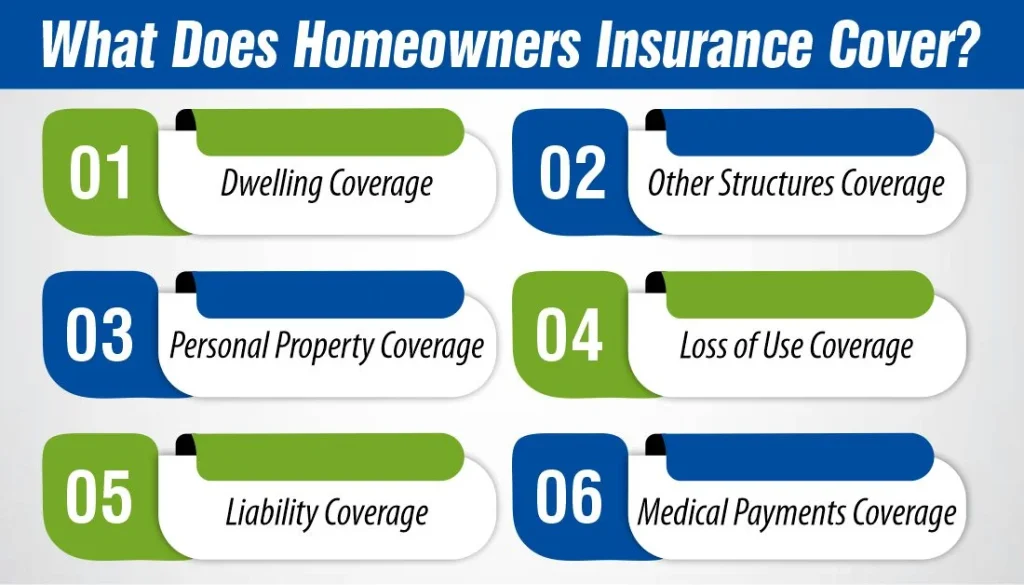

Here’s the deal: for most standard homeowners insurance policies (often called HO-3 policies, for those who like the nitty-gritty), coverage for theft of personal property is a pretty standard inclusion. So, breathe a sigh of relief! Whether it’s a smash-and-grab at your front door or a sneaky break-in while you're away on that dreamy vacation, your policy typically covers the loss of your personal stuff due to theft.

Where Are Your Treasures Covered? You Might Be Surprised!

This isn't just about what's inside your four walls. Homeowners insurance often extends its protective umbrella further than you might think:

Must Read

- Inside Your Home: This is the obvious one. Your TV, laptop, those vintage vinyl records – all generally covered if stolen from inside your house.

- Outside Your Home (on your property): Think about that fancy new grill or your kids' bikes nabbed from the yard or shed. Yep, often covered too!

- Away From Home: This is the fun fact many people miss! If your laptop is swiped from your hotel room in Rome, or your purse disappears at your favorite coffee shop across town, your homeowners insurance might actually step in. It’s like a little security guard that travels with you, quietly looking out for your belongings. How cool is that?

The Nitty-Gritty: What's Covered & What's Not-So-Simple

While the coverage is broad, it’s not a magic wand for everything. Here are a few important considerations:

Personal Property is Key: We're talking about items like furniture, electronics, clothing, jewelry, and sporting equipment. Things that belong to you and your family.

Deductibles and Limits: Just like with car insurance, you'll have a deductible – an amount you pay out-of-pocket before your insurance kicks in. So, if your deductible is $1,000 and your stolen items are worth $1,500, the insurance company would pay you $500. There are also coverage limits for certain categories (like jewelry or firearms) and an overall limit for all personal property.

Actual Cash Value vs. Replacement Cost: This is where it gets interesting. Some policies pay out the actual cash value (ACV), which is the item's value minus depreciation (like a used car). Others offer replacement cost (RCV), meaning they'll pay to replace the item with a brand-new one. Guess which one is usually better? Yep, RCV! It typically costs a bit more in premiums but can save you a bundle if you ever need to file a claim.

High-Value Items & Other Special Scenarios

Got a family heirloom diamond necklace, a valuable art collection, or a high-end bicycle that cost more than your first car? Standard policy limits for these items can be surprisingly low. This is where scheduled personal property endorsements (or riders) come into play. You specifically list and insure these items for their full appraised value, giving them dedicated VIP protection.

Things Your Homeowners Policy Won't Cover:

- Car Theft: Your vehicle itself is covered by your auto insurance (specifically the comprehensive part).

- Business Inventory: If you run a home business and your stock gets stolen, that usually falls under business insurance, not homeowners.

- Roommate Drama: If your roommate "borrows" your vintage comic book collection permanently, your homeowners policy might not cover it, as it's typically for theft by non-residents or criminal acts.

Practical Tips for a Savvy Homeowner

Don't just assume; be prepared!

- Inventory, Inventory, Inventory! Think of it as your personal treasure map. Take photos or videos of your belongings, especially high-value items. Keep receipts. Use an app or a simple spreadsheet. This makes filing a claim so much easier.

- Read Your Policy! Yes, it's boring, but it's your security blanket. Understand your specific deductibles, limits, and exclusions.

- Beef Up Security: While insurance helps after the fact, preventing theft is always better. Smart home cameras, robust locks, and alarm systems (even a good old "Beware of Dog" sign) can be excellent deterrents. Plus, some insurers offer discounts for security features!

- Report It Immediately: If you do experience a theft, call the police right away to file an official report. Your insurance company will need this for your claim.

A Little Reflection on Your Haven

Our homes are more than just bricks and mortar; they're where memories are made, where we recharge, and where our cherished possessions reside. While the thought of theft is unsettling, knowing that your homeowners insurance generally has your back for your personal property can provide a huge sense of relief. It’s not just about replacing stuff; it’s about restoring a sense of normalcy and security to your personal haven. So, take a moment to understand your policy, maybe snap a few photos of your valuables, and then go enjoy that peace of mind knowing you’re well-covered.