Closing Cost On 100k House

Hey, so you're thinking about buying a house? Awesome! And a $100k house, even better! (Think of all the ramen you can buy with the savings!). But before you start picturing yourself sipping lemonade on your porch, let's talk about something kinda boring, but super important: closing costs. Ugh, I know, sounds thrilling, right?

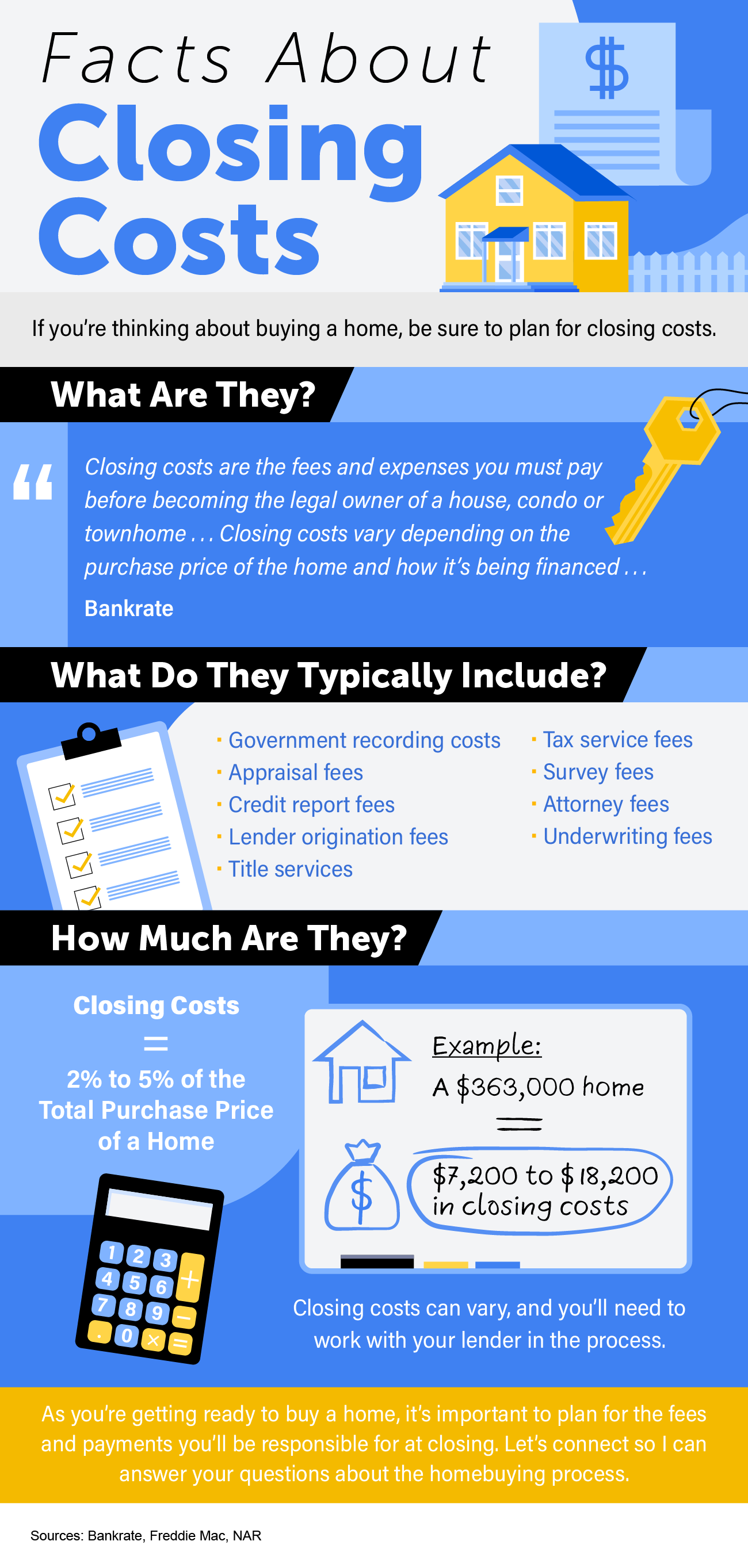

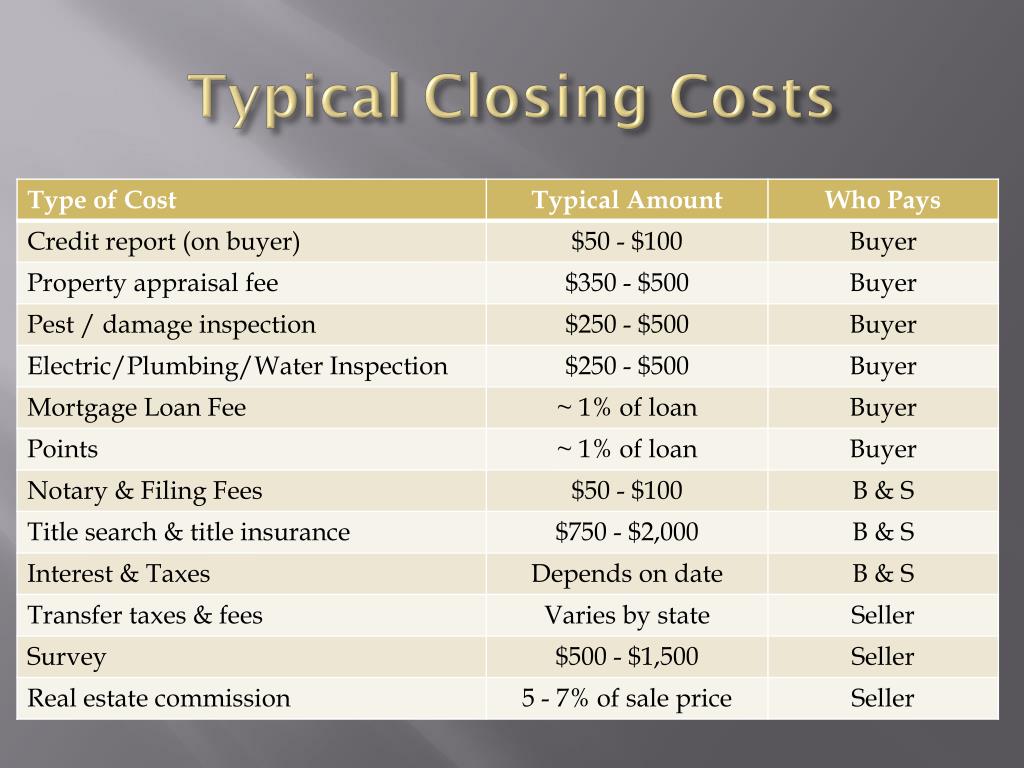

Basically, closing costs are all the extra fees and expenses you pay on top of the actual price of the house when you, well, close the deal. Think of it like the tax and shipping on that online shopping spree... but way more complicated. And often, way more expensive. gulp

So, how much are we talking on a $100k house?

Okay, here's the deal. There's no magic number, unfortunately. It's not like you just punch "$100,000" into a calculator and BOOM! There's your closing cost estimate. It varies, like, a LOT.

Must Read

A good ballpark figure, though? Expect somewhere between 2% to 5% of the loan amount. So, for a $100,000 house, that's roughly $2,000 to $5,000. Whoa, right?

But hold on a sec! Before you start hyperventilating into a paper bag, remember that’s just an estimate. The actual amount can be higher or lower depending on a bunch of factors. Let's dive into some of those fun little details, shall we?

What Makes Up Closing Costs? Buckle Up!

This is where things get a little…dense. But don't worry, we'll break it down. Imagine this is like a recipe. And closing costs are the, um, slightly less delicious ingredients.

Lender Fees: These are the fees your lender charges for processing your loan. Think of it as their "we're doing you a favor" charge. Could include application fees, underwriting fees, and loan origination fees (which can sometimes be negotiated, FYI!). Pro-tip: Shop around for lenders!

Appraisal Fee: This is what you pay to have a professional assess the value of the house. Because you want to make sure you're not overpaying, right? (Unless you really love the pink shag carpet and avocado green appliances... then maybe overpaying is worth it? Just kidding... mostly.)

Title Insurance: This protects you (and the lender) if there are any problems with the title to the property – like, say, someone claiming they actually own the house! It's a one-time fee, and totally worth the peace of mind. Nobody wants unexpected house drama, am I right?

Title Search Fee: This is the cost to research the history of the property to make sure the title is clean and clear. Think of it as a deep dive into the house's past. (Hopefully, no skeletons in the closet…literally or figuratively!)

Recording Fees: These are fees charged by the local government to officially record the transfer of ownership. Basically, it’s like paying to make it official-official.

Property Taxes: You'll likely have to pre-pay some property taxes at closing. This depends on when the closing happens during the year. Taxes, taxes, who loves taxes? (Nobody. The answer is nobody.)

Homeowners Insurance: Same as property taxes, you'll probably have to pay for the first year of homeowners insurance upfront. Gotta protect that sweet new (to you) house from, you know, falling pianos and rogue squirrels.

Location, Location, Location! (And Taxes)

Where you buy the house seriously impacts your closing costs. States and even counties have different tax rates and regulations. High property tax areas will naturally have higher closing costs. So, if you're choosing between two similar houses, consider the property taxes!

Can You Lower Those Pesky Costs?

Actually, yeah! There are a few things you can try:

Negotiate: Some closing costs are negotiable, especially lender fees. Don't be afraid to haggle! (Think of yourself as a super-savvy negotiator. Even if you're not. Fake it 'til you make it!)

Shop Around: Get quotes from multiple lenders and title companies. Comparison shopping can save you serious money. It might feel like a pain, but your wallet will thank you.

Ask About Lender Credits: Sometimes, you can get a lender credit to cover some of your closing costs in exchange for a slightly higher interest rate. Weigh the pros and cons to see if it makes sense for you.

Look into First-Time Homebuyer Programs: Many states and local governments offer programs that can help with down payments and closing costs. Do your research!

The Bottom Line? Be Prepared!

Buying a $100,000 house is awesome, but don't forget to factor in those closing costs. Understanding what they are and how they work is key to avoiding any surprises. So, do your homework, shop around, and don't be afraid to ask questions! Good luck, future homeowner! You got this!