What Is Included In The Post Closing Trial Balance

Hey there, curious minds! Ever felt like your financial statements are speaking a language you only sort of understand? Don't worry, you're not alone! Accounting can seem like a beast, but once you break it down, it’s surprisingly… well, not scary. Today, we're tackling something called the Post-Closing Trial Balance. Trust me, it's less intimidating than it sounds, and understanding it can actually make your financial life a whole lot smoother (and maybe even more fun!).

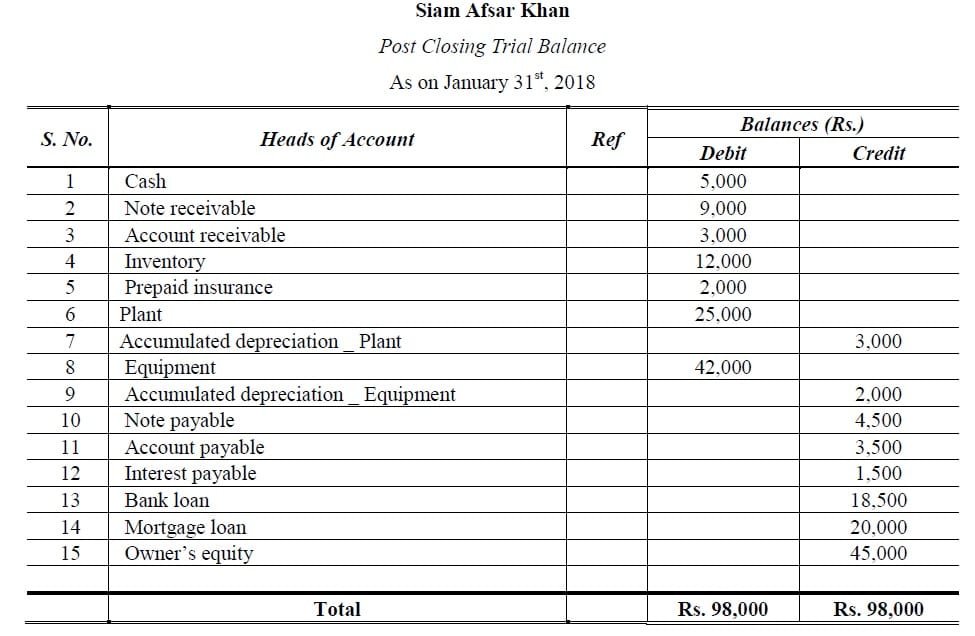

So, what is this mysterious document? Think of it as a snapshot – a quick check-up for your books at the end of an accounting period (usually a month, quarter, or year). It's basically a list of all your permanent accounts and their balances, neatly organized into debits and credits. Debit on the left, credits on the right – it's accounting's left and right, like your hands!

But before we dive into the specifics, let's talk about why this thing even exists. The post-closing trial balance is all about ensuring that your accounting equation (Assets = Liabilities + Equity) is still in balance after you've closed out the books. In simple terms, it helps you catch any errors before you start a new accounting period. Because nobody wants to start a race with a flat tire, right? It validates all your transactions are recorded properly and that your permanent accounts are ready to go for the new accounting period.

Must Read

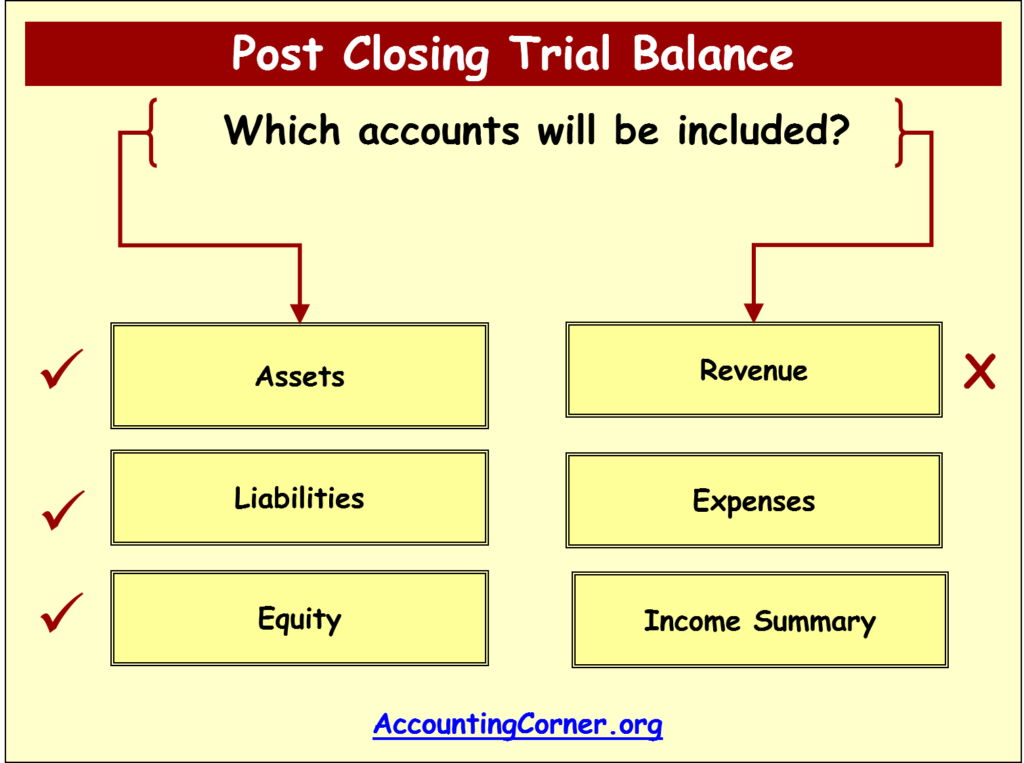

What Actually Shows Up on a Post-Closing Trial Balance?

Okay, now for the nitty-gritty. What exactly are these "permanent accounts" we're talking about? These are accounts that carry their balances forward from one accounting period to the next. They're the foundation of your financial picture.

Assets: Think of these as everything your company owns. It can be cash in the bank (the lifeblood!), accounts receivable (money people owe you), inventory (stuff you plan to sell), equipment (the tools of your trade), and buildings (if you have them, lucky you!). They're all the things you use to make money.

Liabilities: These are your company's obligations – what you owe to others. Accounts payable (bills you need to pay), loans (money you borrowed), and deferred revenue (money you've received for services you haven't yet provided) all fall into this category.

Equity: This is the owner's stake in the company. It represents the residual interest in the assets of the entity after deducting liabilities. Common components include common stock (if it applies), and retained earnings (the accumulated profits that haven't been distributed to owners).

Important Note: Notice anything missing? That's right! Revenue and expense accounts are not included! These are temporary accounts that get "zeroed out" at the end of each accounting period as part of the closing process. Think of it like clearing the table after a feast – you start fresh for the next meal.

So, after the closing entries are done, the only accounts left with balances are your assets, liabilities, and equity – hence, these are the ones that show up on the post-closing trial balance. Simples!

Why Bother? It's Actually Pretty Cool!

I know, I know, accounting doesn't exactly scream "thrilling adventure." But think of it this way: understanding the post-closing trial balance is like having a secret decoder ring for your business finances. When you know what's going on beneath the surface, you can make better decisions, spot potential problems early, and sleep soundly at night knowing your books are (most likely) accurate. Peace of mind is priceless, right?

Plus, it's a great way to impress your accountant (or your boss, or your friends at a dinner party – okay, maybe not at a dinner party… unless your friends are really into accounting!). And who knows, maybe you'll even discover a hidden talent for financial analysis! The possibilities are endless!

Seriously, understanding the basics of accounting, including the post-closing trial balance, empowers you. It gives you control over your financial destiny. Instead of feeling lost in a sea of numbers, you can navigate your way with confidence.

So, go forth and conquer your financial statements! Don't be afraid to ask questions, seek out resources, and keep learning. Every little bit of knowledge you gain brings you closer to financial mastery. And who knows? Maybe you'll even start to enjoy it (a little bit!).

The world of finance awaits! Embrace the challenge, unlock your potential, and make your financial dreams a reality. You got this!