What Is A Dp3 Insurance Policy

Alright, gather 'round, friends! Let's talk about DP3 insurance. Now, I know, insurance sounds about as thrilling as watching paint dry, but trust me, we can make this fun. Think of it as understanding the secret language of grown-ups... a language spoken in deductibles and coverage limits!

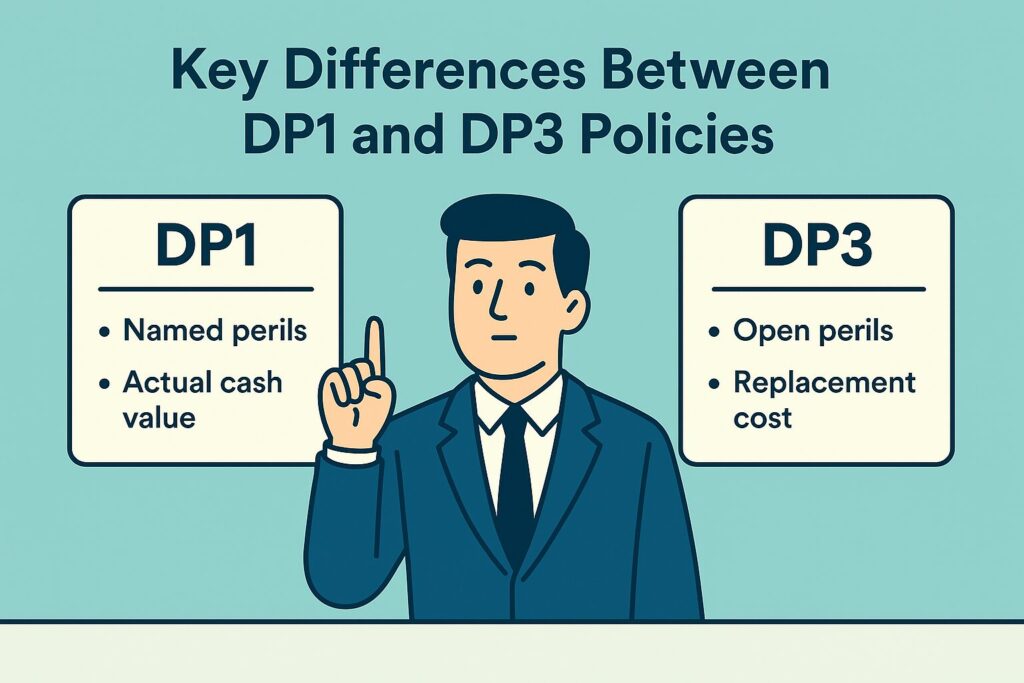

So, what is a DP3 policy? Well, the "DP" stands for Dwelling Property. Clever, right? It's insurance specifically designed for, get this... dwellings! Shocker, I know. But here’s the kicker: unlike some of its more restrictive cousins (we're looking at you, DP1 and DP2), DP3 offers the coveted "all-risks" coverage. Or, as I like to call it, "blame-it-on-anything-but-purposeful-destruction" coverage.

Basically, unless it’s specifically excluded in your policy (and believe me, those exclusions are listed out like the ingredients on a ridiculously complicated energy bar), it's covered. Think of it this way: if a rogue flock of pigeons, possessed by the spirit of a disgruntled architect, decides to dismantle your roof, DP3 might cover that. (Okay, probably not. Check your policy exclusions, folks!) But you get the idea!

Must Read

The Upside-Down Cake of Coverage: What's Included?

Imagine your insurance policy as an upside-down cake. The bottom layer, the foundation of everything, is the dwelling itself. That's the main building, the four walls, the roof, the whole shebang. DP3 is there to protect it from… well, pretty much everything that isn't nailed down in the "exclusions" section.

Then comes the middle layer: other structures. This covers things like detached garages, sheds, fences, or even that ridiculously elaborate birdhouse you built during your brief but intense carpentry phase. Remember that time you accidentally set the garden shed on fire while trying to deep-fry a turkey? (Don’t worry, we've all been there… some of us more than others). DP3 could help with that! (Again, check your policy. Deep-frying turkeys probably falls under 'negligence'.)

And finally, the delicious, sugary top layer: fair rental value. This is the sweet icing on the cake! If your property becomes uninhabitable due to a covered loss (like, say, the aforementioned pigeon-architect conspiracy actually coming to fruition), DP3 can help cover the rental income you lose while it's being repaired. It's like insurance for your insurance! Mind. Blown.

Important Note: DP3 policies generally do NOT cover your personal belongings. That’s where a separate policy, like an HO4 (renter's insurance) or an HO3 (homeowner's insurance) comes in. So, if your antique collection of porcelain cats gets destroyed in a fire, you'll need a different policy to cover that particular catastrophe. (Unless, of course, the fire was started by a rogue porcelain cat possessed by a vengeful spirit. In that case, you might need an exorcist, not insurance.)

Who Needs This Fancy-Pants Insurance?

DP3 is a popular choice for landlords renting out properties. It offers broader coverage than DP1 or DP2 policies, which can provide greater peace of mind when you're not physically there to monitor your investment (and prevent rogue pigeon architectural conspiracies). It's also a good option for homeowners who rent out their properties for short periods, like through Airbnb or VRBO.

But, and this is a big BUT (and I cannot lie), it's crucial to read the fine print. I know, it's about as appealing as reading a phone book from the 1980s, but understanding the exclusions and limitations of your DP3 policy is vital. Don't just assume everything's covered. Knowledge is power, my friends! And in the world of insurance, knowledge can save you a whole heap of cash (and a lot of headaches).

Consider it your insurance policy's New Year's resolution to be transparent. If you don't understand something, ask your insurance agent! That's what they're there for (besides processing paperwork and trying to sell you more insurance, of course).

The Bottom Line (Because We All Love Bottom Lines)

DP3 insurance is a great option for protecting rental properties. It offers broader coverage than other dwelling property policies, which can be a lifesaver when unexpected events occur. Just remember to carefully review your policy, understand the exclusions, and don't deep-fry turkeys indoors. You'll thank me later. And so will your insurance company.

Now, if you'll excuse me, I'm off to research pigeon-proof roofing materials. You can never be too careful!