Monthly Payments On 315k Mortgage

Hey friend! Thinking about taking the plunge and buying a house? Exciting times! One of the biggest things swirling around in your head is probably: "Okay, but what's this gonna cost me every month?" Let's break down those potential monthly payments on a $315,000 mortgage. No need for a calculator headache, we'll keep it breezy!

The Big Picture: Principal & Interest (P&I)

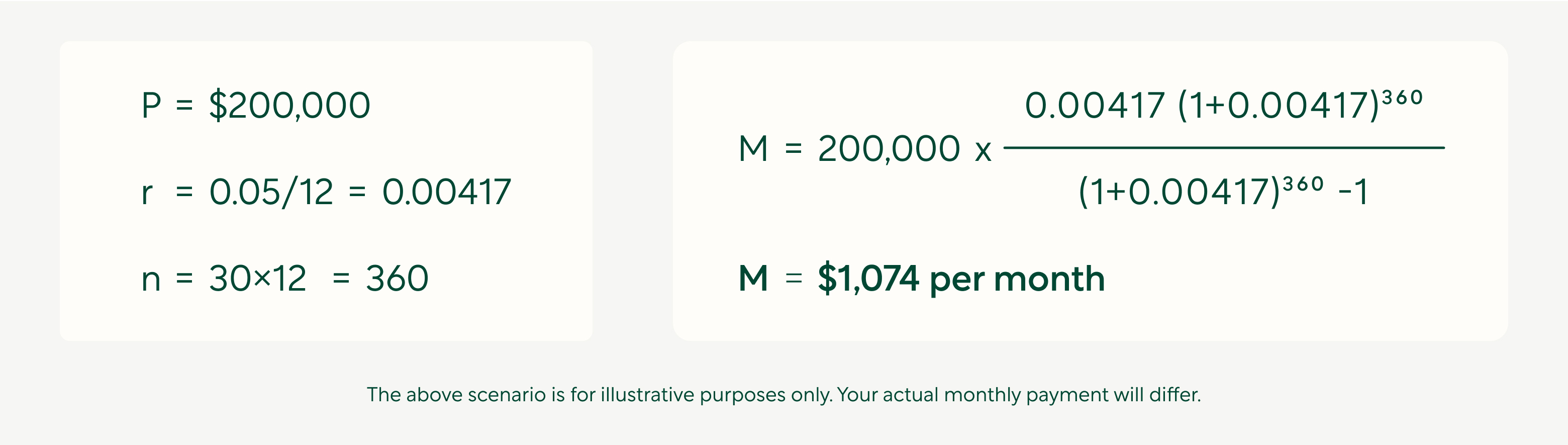

First things first, when people talk about mortgage payments, they often focus on the principal and interest (P&I). This is the core of your loan – the amount you borrowed ($315k in this case) plus the interest you're paying on it. The exact amount of your P&I payment depends primarily on two factors: the interest rate and the loan term.

Interest Rate: Think of this as the "price" of borrowing money. It's expressed as a percentage. Currently, mortgage rates fluctuate quite a bit – think rollercoaster, but hopefully a pleasant one! So, I can't give you an exact number, but we can use some examples. A lower interest rate means a lower monthly payment. Obvious, right? But sometimes the obvious needs saying! Disclaimer: I'm not a financial advisor; get the real deal from a pro!

Must Read

Loan Term: This is how long you have to pay back the loan. The most common is 30 years, but 15-year mortgages are also popular. A shorter term means higher monthly payments, but you'll pay less interest overall. Imagine choosing between slowly savoring a delicious dessert (30 years) or gobbling it down quickly (15 years). Both get you to the same sweet place (owning your home!), but the experience is different.

Crunching the Numbers (Roughly!)

Okay, let's get a little number-y (but still fun!). Let's imagine a few scenarios for that $315,000 mortgage:

Scenario 1: 30-Year Mortgage at 6.5% Interest In this case, your principal and interest payment would be roughly around $1,988. Remember, this is just an estimate! Think of it like a starting point for your calculations.

Scenario 2: 15-Year Mortgage at 6.0% Interest Here, your monthly P&I jumps to about $2,660. A bigger bite each month, but you're free and clear much faster! (And you save a ton on interest over the life of the loan).

See the difference? Interest rates have a huge impact! Even a small difference in the rate can save you a boatload of money over the long haul. Shop around for the best rates! Don't just go with the first lender you find. Treat it like finding the perfect pair of shoes – try on a few!

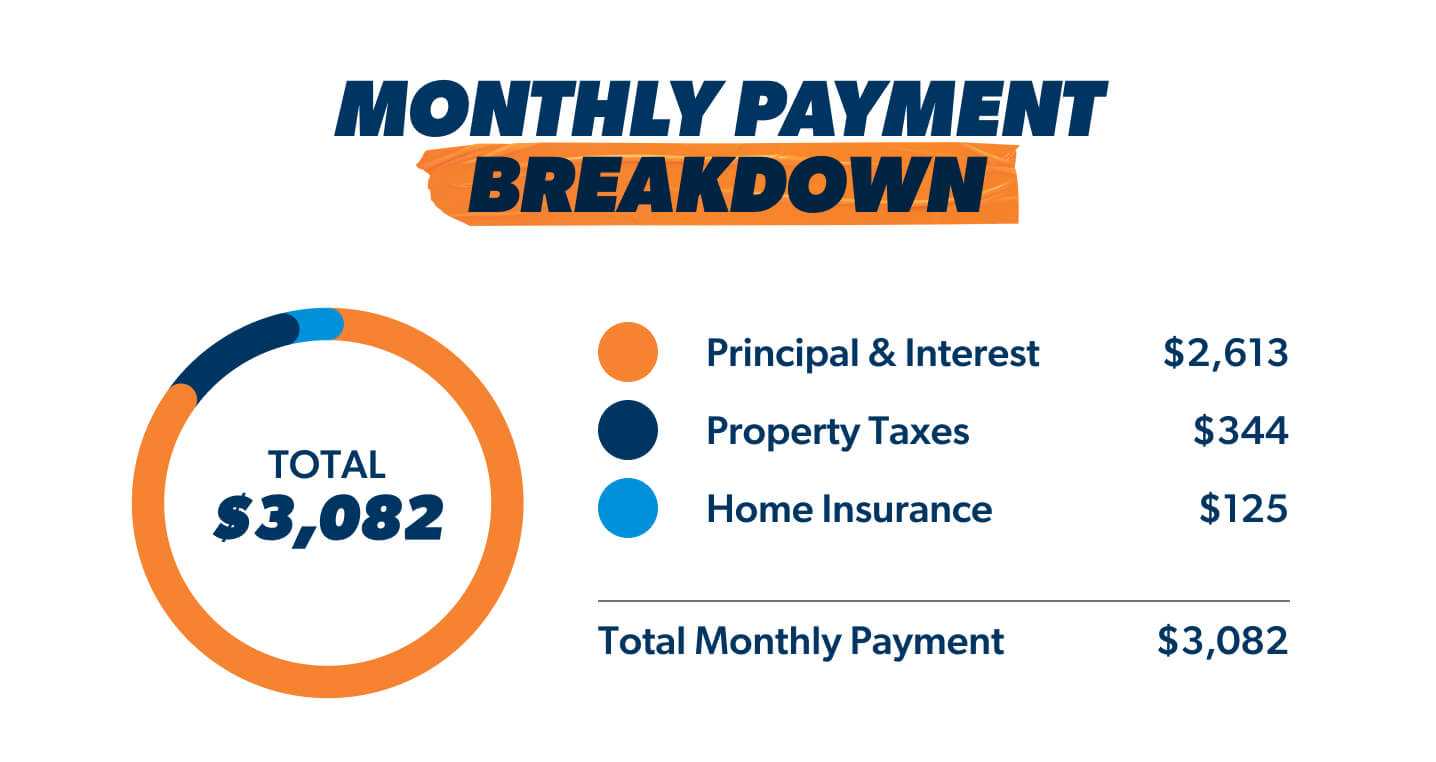

Beyond P&I: The "Extras" (Escrow Account)

Hold on, there's more to the story! Your total monthly mortgage payment usually includes more than just principal and interest. It often includes:

Property Taxes: The government wants its cut! These vary wildly depending on where you live. Could be a few hundred bucks, could be much more. Find out what they are in your target area!

Homeowner's Insurance: Protects your investment in case of fire, storms, or other disasters. It's a must-have. Get quotes from different insurers – they can vary quite a bit too.

Private Mortgage Insurance (PMI): If you put less than 20% down on the house, you'll likely have to pay PMI. This protects the lender if you default on the loan. Once you reach 20% equity in your home, you can usually get rid of PMI. It's like training wheels – helpful at first, but you ditch them once you're confident!

These "extras" are usually bundled together into an escrow account. Your lender collects a portion of these costs each month and pays them on your behalf when they're due. This makes budgeting a little easier and ensures these important bills get paid.

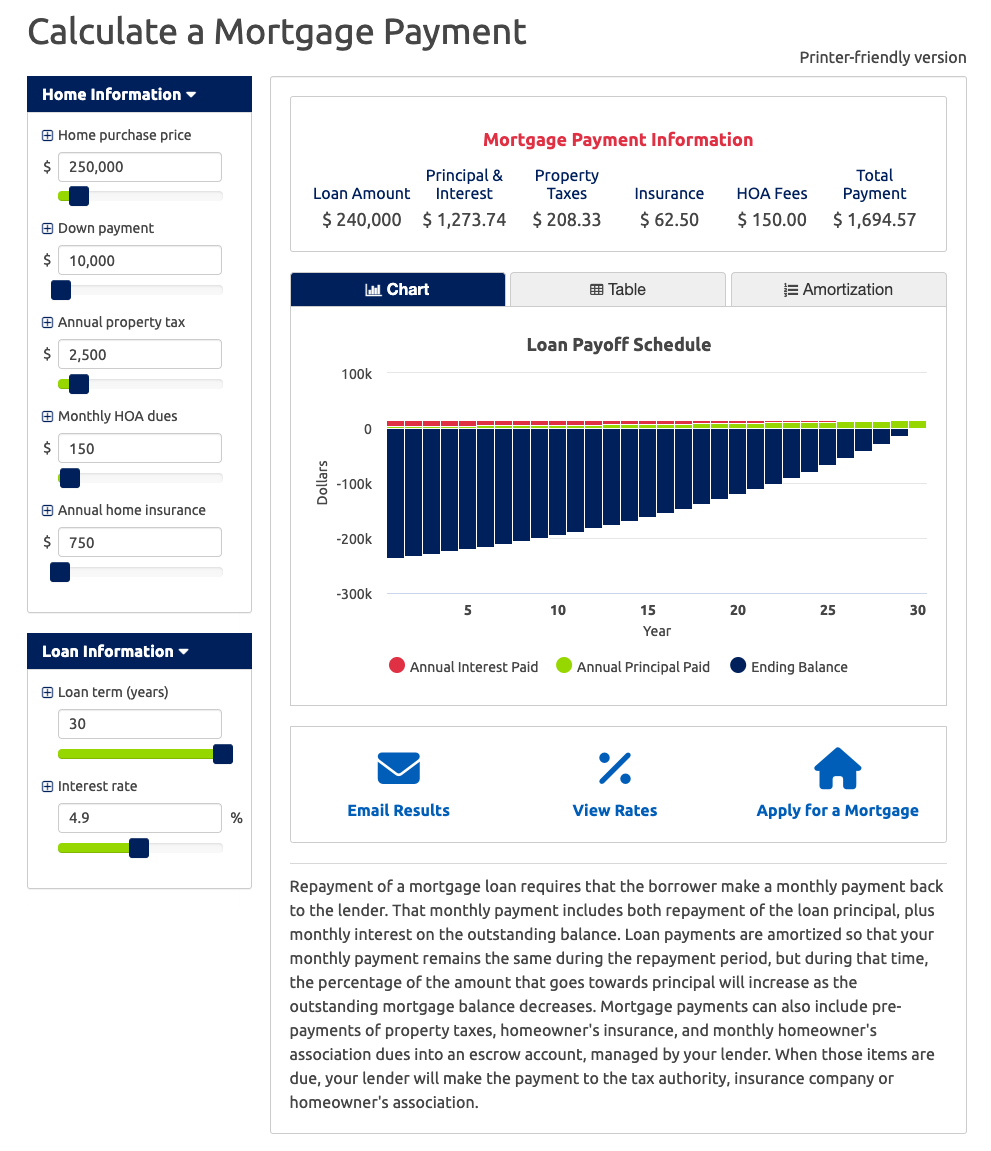

Adding It All Up: So, to get a truly accurate estimate of your monthly payment on a $315,000 mortgage, you need to factor in those property taxes, homeowner's insurance, and potentially PMI. Talk to a lender or use an online mortgage calculator that includes these costs.

Don't Panic! You Got This!

Okay, I know all these numbers can be a little overwhelming. But don't worry! Take a deep breath. Homeownership is a big decision, but it's also incredibly rewarding. With a little planning and research, you can confidently navigate the mortgage process and find a payment that fits your budget. Remember to shop around for the best interest rates, consider different loan terms, and factor in those extra costs like property taxes and insurance.

And hey, even if the numbers seem a little daunting at first, keep in mind that your salary will (hopefully!) increase over time, and you'll build equity in your home. It's a long-term investment, and it's totally achievable! Now go forth and conquer that real estate dream! You’ve got this! And when you get the keys, invite me over for pizza, okay?