Is 518 A Bad Credit Score

Okay, let's talk credit scores. Specifically, the magic (or maybe not-so-magic) number: 518. Ever wondered what it really means?

Think of your credit score like your financial GPA. It sums up how reliable you are with money. Banks, landlords, even some employers peek at it. Creepy? Maybe. Necessary? Sometimes. But is a 518 GPA an "F" or just a "needs improvement"? Let's find out!

The Credit Score Spectrum: Where Does 518 Land?

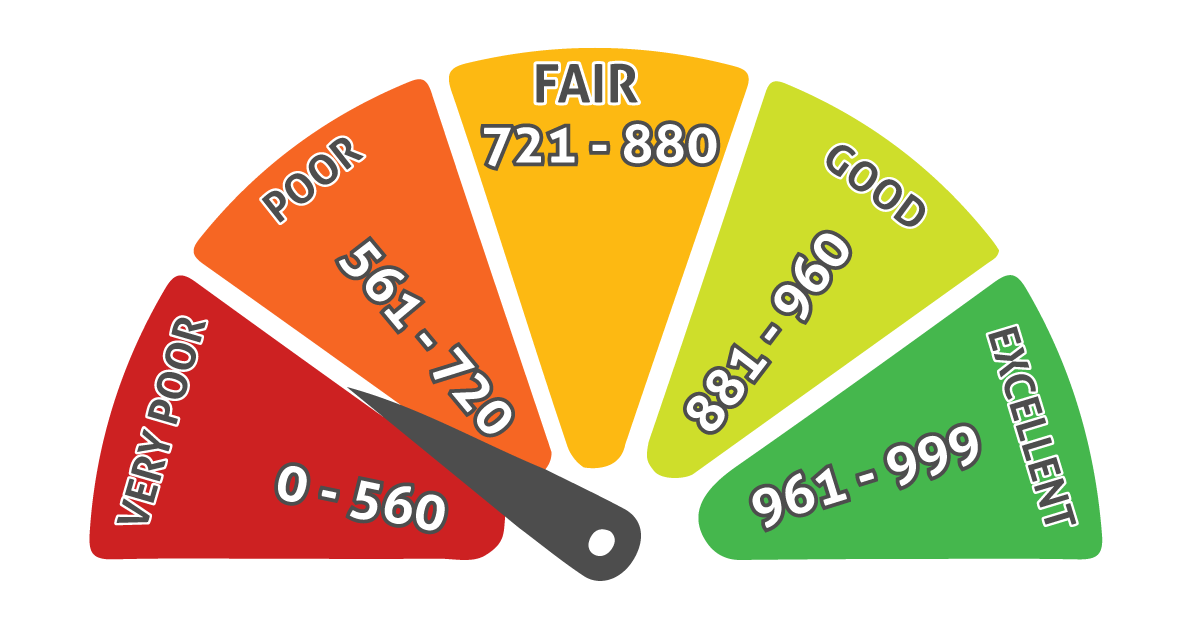

First, let's set the stage. Credit scores, usually FICO scores, range from 300 to 850. 300? Ouch. 850? You're basically a financial superhero. Now, a 518? Well, it's definitely hanging out in the "needs work" zone.

Must Read

Think of it this way: Imagine you're trying to bake a cake. A credit score of 518 is like having all the ingredients, but you accidentally used salt instead of sugar. Edible? Technically. Delicious? Probably not. Requires some serious adjustments.

The general breakdown looks something like this:

- Excellent: 800-850 (You're a financial rockstar!)

- Very Good: 740-799 (Looking good!)

- Good: 670-739 (Solid, dependable.)

- Fair: 580-669 (Room for improvement.)

- Poor: 300-579 (Uh oh. Time for a financial makeover!)

So, yeah. 518? It's firmly in the "poor" category. No sugar-coating it. But hey, at least you now know where you stand! And knowledge is power! (Especially financial power!).

So, Is 518 Bad?

Short answer? Yes. Long answer? Yeeeeessss. It’s not the end of the world, but it’s definitely a red flag waving frantically. Think of it as your credit score screaming, "Help me! I need financial TLC!"

A score of 518 can impact your life in some not-so-fun ways:

- Higher Interest Rates: Want a loan? Get ready to pay more. A lot more. Banks see you as a risk.

- Difficulty Getting Approved: Credit cards, mortgages, even car loans can be tough to snag. Prepare for rejection.

- Rental Woes: Landlords often check credit scores. A low score can mean "no vacancy." Bummer.

- Higher Insurance Premiums: Believe it or not, your credit score can affect how much you pay for insurance. Crazy, right?

But hey! Don't despair. Every financial saga has a turning point. Yours just might be realizing that 518 isn't exactly a winning lottery number.

Why is My Credit Score So Low Anyway?

Time for some detective work! What's dragging your score down? Here are some common culprits:

- Late Payments: The biggest offender. Paying bills late is like throwing financial grenades at your credit score. Ouch.

- High Credit Utilization: Maxing out your credit cards? Not a good look. Try to keep your balances well below your credit limits.

- Defaults and Collections: Ignoring debts? They'll come back to haunt you. Creditors can send unpaid debts to collection agencies. Double ouch.

- Bankruptcy: A serious financial setback that can significantly damage your credit score.

- Too Much Credit Inquiries: Applying for too many credit cards in a short period? Lenders think you're desperate. Take it easy, credit card enthusiast!

Pull your credit report from Experian, Equifax, and TransUnion. You're entitled to a free copy from each bureau annually at AnnualCreditReport.com. Scrutinize it! Find the mistakes! Challenge the inaccuracies!

Okay, I'm Freaking Out. What Can I Do?

Deep breaths! It's fixable! Improving your credit score is like training for a marathon. It takes time, effort, and maybe a few blisters along the way, but you can do it!

Here's your recovery plan:

- Pay Your Bills On Time, Every Time: This is the most important thing. Set reminders. Automate payments. Do whatever it takes!

- Reduce Your Credit Card Balances: Pay them down! Even small payments can make a difference. Think of it as financial weightlifting.

- Don't Close Old Credit Cards: Even if you don't use them, keeping old accounts open can help your credit utilization ratio. Just don't rack up new debt!

- Become an Authorized User: Ask a friend or family member with good credit to add you as an authorized user on their credit card. Instant credit boost! (But make sure they pay their bills on time!)

- Consider a Secured Credit Card: These cards require a security deposit, but they can help you rebuild your credit.

Boosting your credit score isn't a sprint; it's a marathon. It takes dedication and a willingness to change your financial habits. But trust me, that higher score is worth the effort. Imagine finally getting approved for that dream apartment, snagging a low interest rate on a car loan, or simply having the peace of mind that comes with financial security. Sounds pretty good, right?

So, while 518 isn't exactly a reason to celebrate, it is a reason to start planning. Consider this your financial wake-up call. You've got this!