How Accurate Is Discover Fico Score

Hey friend! Ever wondered about that little number Discover throws your way, calling it your FICO score? You know, the one you can sneak a peek at without dinging your credit? We're gonna dive into how accurate that thing really is. Think of me as your credit score sherpa, guiding you through the mountains of financial info… except, you know, with less frostbite.

So, What Exactly Is Discover's FICO Score?

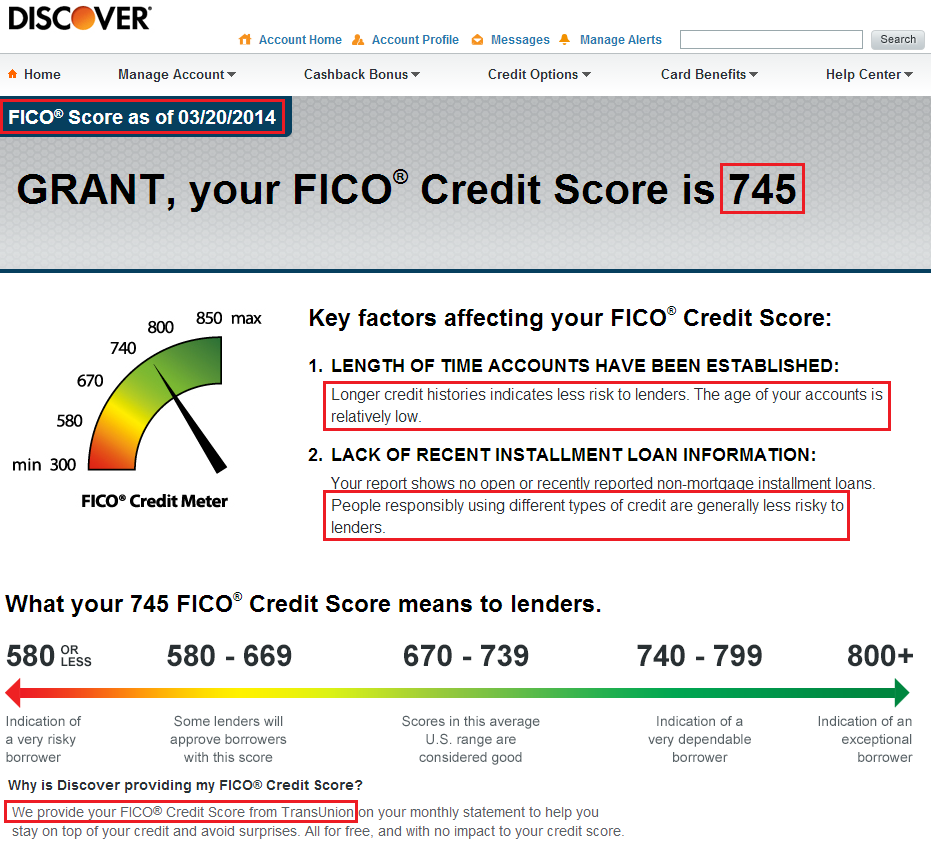

First things first, it's not some voodoo magic. Discover provides you with a FICO score, which is a legitimate credit score calculated using data from your TransUnion credit report. Think of TransUnion as one of the big three credit bureaus, keeping tabs on your creditworthiness. Your FICO score is a snapshot of your credit health at a specific moment in time. So, it's like a selfie, not a lifetime documentary!

Discover uses the FICO Score 8 model (most commonly), which is a pretty standard and widely used version. It’s not some obscure, home-brewed score they invented in their basement (though, wouldn't that be a story?). That's good news, because it means many lenders understand and use this model.

Must Read

The Nitty-Gritty: How Accurate Is It?

Okay, the million-dollar question! The Discover FICO score is generally considered to be accurate. However, and this is a BIG however, it's just one piece of the puzzle. Remember that selfie analogy? You have other angles, lighting, and filters to consider. (Okay, maybe not filters for your credit, but you get the idea!).

Here's why it's accurate but not the only truth:

- It's based on real data: It's pulled directly from your TransUnion credit report, so it reflects your actual credit history.

- It uses a standard model: FICO Score 8 is a reputable and common scoring model.

Here's why it might not be exactly the same as what a lender sees:

- Different bureaus: Lenders might pull your credit report from Equifax or Experian (the other two bureaus) instead of TransUnion. Each bureau can have slightly different information. Think of it as each bureau hearing a slightly different version of the same story.

- Different FICO models: Lenders can use different versions of the FICO score or even use a completely different scoring model altogether (like VantageScore). Some lenders might even have their own proprietary scoring systems. It's like everyone having their own recipe for chili, even though they're all technically chili.

- Timing is everything: Credit scores are dynamic. Your Discover score reflects your credit at a specific point in time. If something changes on your credit report after Discover updates your score, there will be a discrepancy.

So, What Should You Do With This Information?

Don't panic! The Discover FICO score is a fantastic tool for monitoring your credit health. It gives you a general idea of where you stand and helps you track your progress as you work to improve your credit. It's like having a weather forecast – it's not perfect, but it gives you a pretty good idea of what to expect.

Here's how to use it wisely:

- Track your progress: Is your score going up? Down? Stay consistent!

- Identify potential problems: If your score drops suddenly, it's a red flag! Investigate and see if there are any errors on your credit report or signs of fraud.

- Don't obsess over it: Remember, it's just one score. Don't let it stress you out. (Easier said than done, I know!)

The key takeaway? The Discover FICO score is a valuable, accurate-ish tool for managing your credit. Use it to stay informed, track your progress, and spot potential problems. Just don't treat it as the absolute gospel truth about your creditworthiness. It's more like a friendly nudge in the right direction. So go forth, conquer your credit goals, and remember to laugh a little along the way! You've got this!