Closing Costs On 1.2 Million Dollar Home

Okay, picture this: you're at a swanky cocktail party, sipping something bubbly, and the conversation turns to… real estate. Naturally. Someone throws out the phrase "closing costs" like it's a fun party game. Everyone nods sagely, but you're secretly thinking, "Wait, what exactly are we talking about here?" Especially when you're picturing a place that costs, oh, I don't know... maybe $1.2 million?

Yeah, that cocktail party moment is what inspired this little deep dive. We're gonna break down the mystery of closing costs on a $1.2 million home. Because let's be honest, nobody wants surprise expenses popping up after you've already committed to a mortgage that's probably bigger than your car (or maybe even your first house!).

The Closing Costs Rundown: It's a Party, But You're Paying

First, let's get this out of the way: closing costs are basically all the fees and expenses you pay on top of the actual price of the house. Think of it as the "processing fee" for the privilege of owning a fabulous new place. And spoiler alert: they're not exactly pocket change.

Must Read

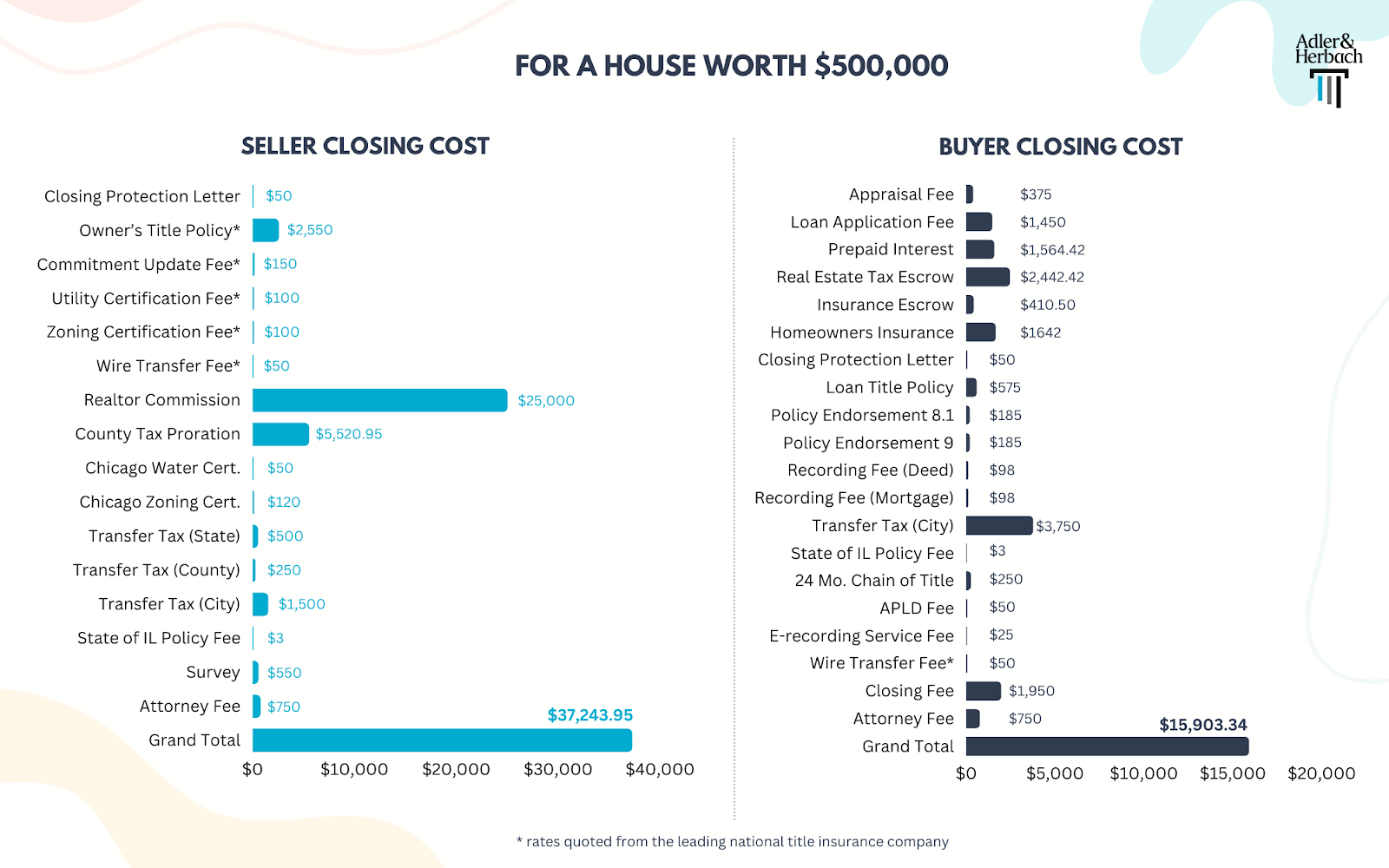

Generally, closing costs range from 2% to 5% of the home's purchase price. So, for our hypothetical $1.2 million dream home, we're looking at a potential range of $24,000 to $60,000. Whoa. That's like a small car, a very nice vacation, or a substantial down payment on… something else entirely.

Now, where does all that money actually go?

The Usual Suspects: Who Gets Your Money?

Here's a breakdown of some of the most common closing costs you'll encounter. Prepare yourself, it's a bit of a laundry list:

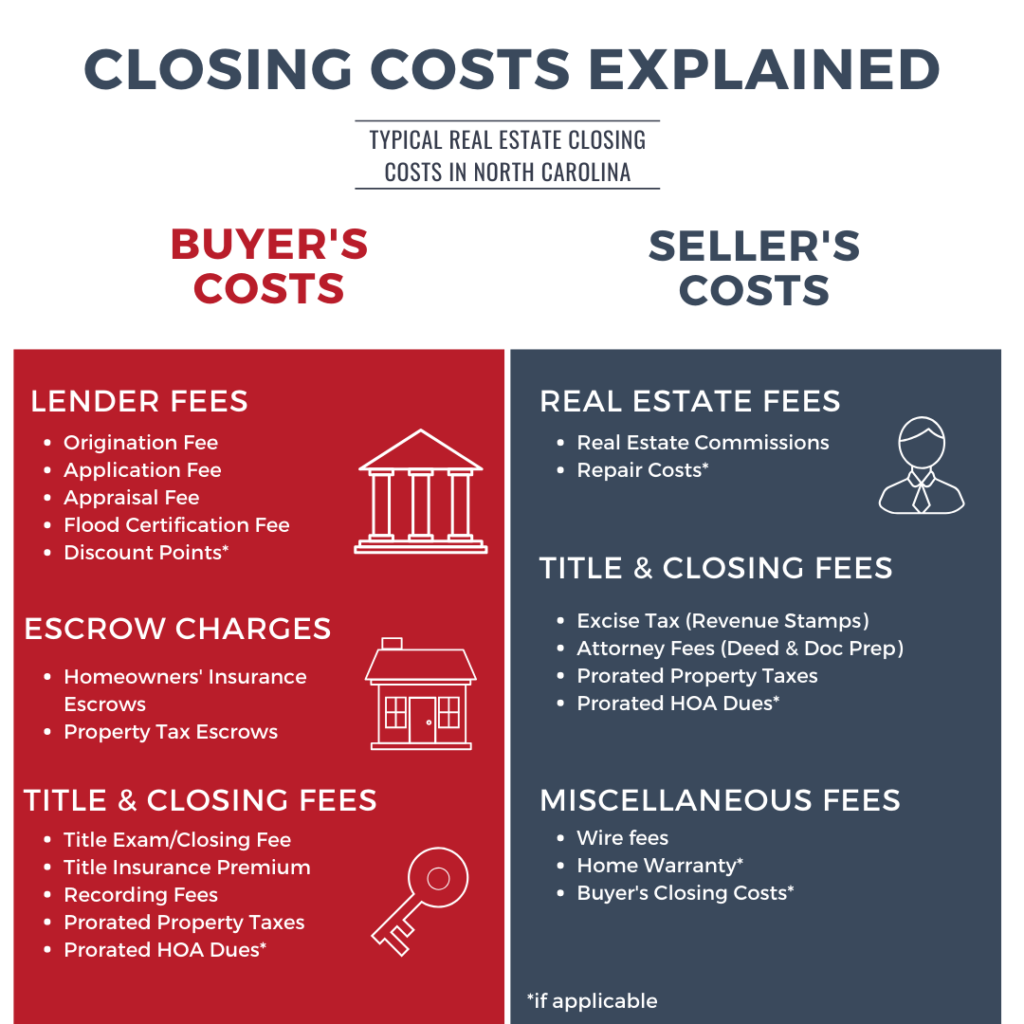

- Lender Fees: This includes things like the loan origination fee (basically, the bank's fee for processing your loan), appraisal fees (to determine the house's market value – because they don't just take your word for it!), and credit report fees. They need to make sure you're good for the money!

- Title-Related Fees: This is where things get a little… technical. Title insurance protects you (and the lender) in case there are any issues with the property's title (like someone else claiming ownership). You'll also pay for a title search to make sure the title is clean in the first place. Think of it as a background check for your house.

- Taxes and Government Fees: You can't escape them! This includes things like recording fees (to officially register the deed with the local government) and transfer taxes (a tax on the transfer of property ownership). These vary wildly by location, so definitely do your homework!

- Escrow Fees: If you're setting up an escrow account to pay your property taxes and homeowners insurance, you'll likely have some initial escrow fees.

- Home Inspection: Okay, this one isn't technically required, but it's insanely important. A home inspection will reveal any potential problems with the house before you close the deal, saving you from costly surprises down the road. Consider it an investment in your peace of mind. Don't skip this. Seriously.

Location, Location, Location: It Matters (A Lot!)

Remember that 2% to 5% range we talked about earlier? Well, that range can vary significantly depending on where you're buying. Some states and cities have higher transfer taxes or other fees than others. For instance, buying a $1.2 million property in New York City will likely have much higher closing costs than buying a similar property in, say, rural Montana. (No offense to Montana – it's lovely! But the real estate landscape is, shall we say, different.)

Pro Tip: Talk to a local real estate agent or attorney to get a more accurate estimate of closing costs in your specific area. They'll have the inside scoop on all the local fees and taxes.

Negotiate, Negotiate, Negotiate: It's Not a Fixed Price

Here's the good news: some closing costs are negotiable! You can try to negotiate with the seller to cover some of the costs (especially if you're in a buyer's market), or you can shop around for different lenders to get better rates on things like loan origination fees. Don't be afraid to haggle! It's your money, after all. Remember to get everything in writing.

So, there you have it: a (hopefully) less-intimidating overview of closing costs on a $1.2 million home. It's a significant chunk of change, but understanding what you're paying for can help you budget accordingly and avoid any unpleasant surprises. Now, go forth and conquer that real estate dream… just remember to factor in those pesky closing costs!

![Las Vegas Real Estate - FACTS ABOUT CLOSING COSTS [INFOGRAPHIC] | Love](https://files.keepingcurrentmatters.com/content/images/20230330/Facts-About-Closing-Costs-MEM.png)