Can You File Bankruptcy On Personal Loans

Okay, let's talk about something nobody really wants to talk about: personal loans. And the B-word. Bankruptcy. Shhh! Don't say it too loud! The financial gods might smite us.

We've all been there, right? Maybe you needed a new fridge. Or perhaps your car decided to stage a dramatic (and expensive) breakdown. Enter the trusty personal loan. It swoops in, a knight in slightly tarnished armor, promising financial relief. Until, well, it doesn't.

The question is: can you actually declare bankruptcy on those little loan knights that became financial dragons? The short answer? Usually, yes. But isn't life always more complicated than a simple "yes" or "no"?

Must Read

The Bankruptcy Breakdown (Simplified!)

Think of bankruptcy as hitting the financial reset button. It's like that emergency lever you pull when your life (or, more accurately, your budget) is spiraling out of control. There are different types of bankruptcy, the two most common being Chapter 7 and Chapter 13.

Chapter 7 is the "liquidation" option. You sell off some of your assets (with exemptions, of course – they're not going to leave you homeless!) to pay off creditors. Chapter 13 is more of a repayment plan. You agree to pay back some (or all) of your debt over a period of three to five years.

Now, the nitty-gritty. Generally, unsecured debts are dischargeable in bankruptcy. Personal loans? They're usually unsecured. Meaning, there’s no specific asset, like your house or car, guaranteeing the loan. If you don't pay, they can't repossess your couch (unless it’s really fancy).

The Catch (Because There's Always a Catch)

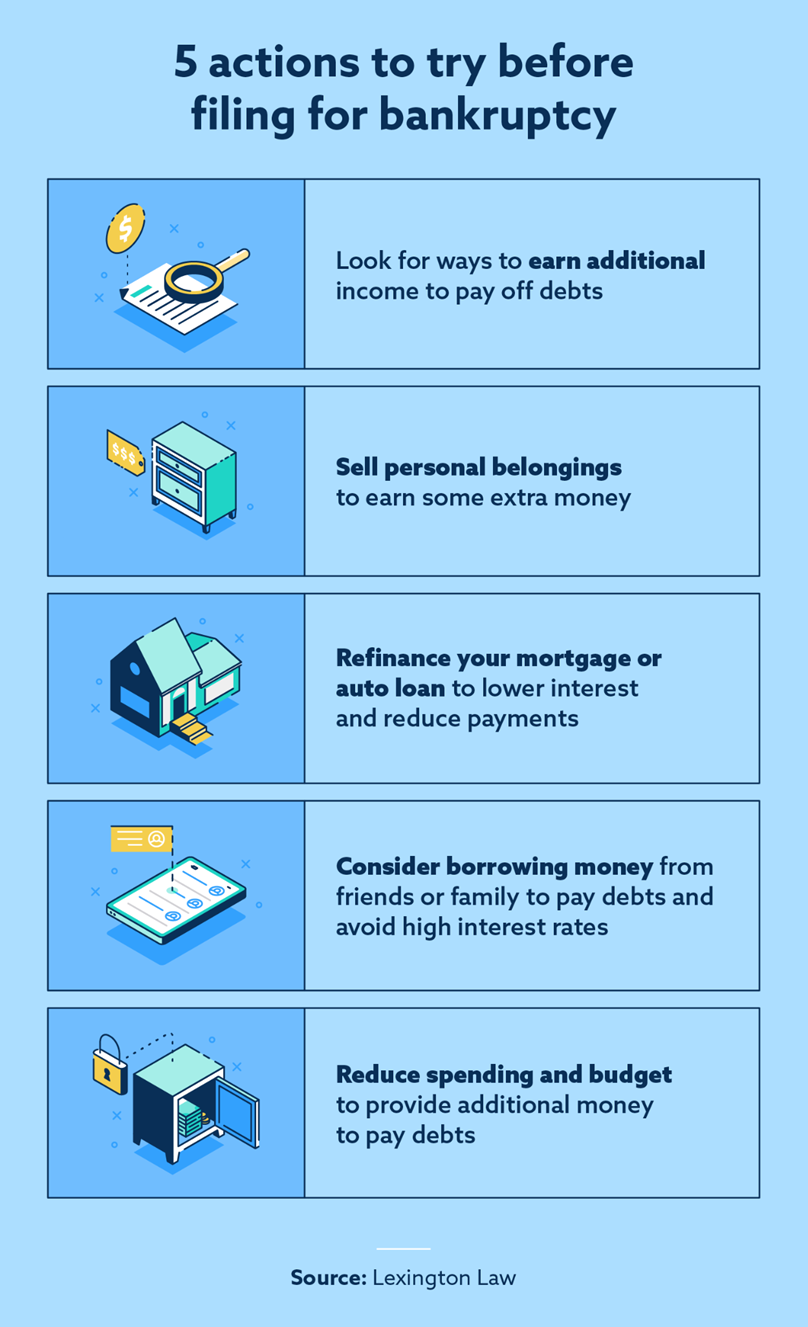

So, you’re thinking, “Hallelujah! Bankruptcy is the answer!” Hold your horses, partner. There are a few things that could throw a wrench in your grand plan.

For example, if you committed fraud when obtaining the loan (like, say, you lied about your income), the court might decide the debt isn't dischargeable. Nobody likes a liar, especially bankruptcy judges.

Also, if you’ve recently racked up a ton of debt right before filing, the court might raise an eyebrow. They might think you're just trying to game the system. And nobody likes a gamer, especially bankruptcy judges.

And here's a bit of an unpopular opinion: sometimes, bankruptcy isn't the best answer. I know, heresy! But seriously, consider the long-term consequences. Bankruptcy stays on your credit report for up to ten years. That can make it tough to get a mortgage, a car loan, or even a credit card. It's a big deal.

My Unpopular Opinion: Personal Loans Should Be Harder to Get

Look, I get it. Life happens. But I'm just saying, maybe, just maybe, it should be a little harder to get a personal loan in the first place. Make people really think about whether they need that new jet ski. (Okay, maybe not a jet ski, but you get my drift.)

Think about it. We're bombarded with ads promising instant gratification, easy money, and the ability to buy now, pay later. It's a dangerous cocktail! Wouldn't it be better if lenders were a little more cautious, a little more responsible? Maybe then, fewer people would find themselves drowning in debt and contemplating the B-word.

So, can you file bankruptcy on personal loans? Probably. But should you rush into it? That's a question only you can answer. Talk to a qualified bankruptcy attorney (they're the real pros here!). Explore all your options. And maybe, just maybe, try to resist the urge to buy that third pair of shoes you don't need.

Remember, financial responsibility is sexy. Okay, maybe not sexy, but definitely… admirable. Yeah, let's go with admirable.

And if all else fails, blame Dave Ramsey. Just kidding! (Mostly.)