Can Credit Repair Companies Remove Collections

Let's face it, who doesn't dream of a pristine credit report? It's like the ultimate adulting superpower, unlocking lower interest rates on mortgages, car loans, and even credit cards. A good credit score can feel like a golden ticket, opening doors and making life a little bit easier. But what happens when unwelcome guests like collection accounts crash the party and drag your score down? That's when the question arises: Can credit repair companies swoop in and magically erase them?

The appeal of credit repair companies is understandable. They promise to clean up your credit report, removing inaccuracies and potentially boosting your score. The potential benefits are significant. A better credit score translates to lower interest rates, saving you potentially thousands of dollars over the life of a loan. It can also improve your chances of getting approved for apartments, jobs, and even insurance policies. In essence, a good credit score provides financial flexibility and opportunity.

Think of it this way: you want to buy a house. A collection account on your report could mean a higher interest rate on your mortgage, adding significantly to your monthly payments. Removing (or even just disputing) that collection could save you a substantial amount of money. Or imagine you're applying for a job that requires a credit check. A clean report could be the difference between landing your dream job and being passed over.

Must Read

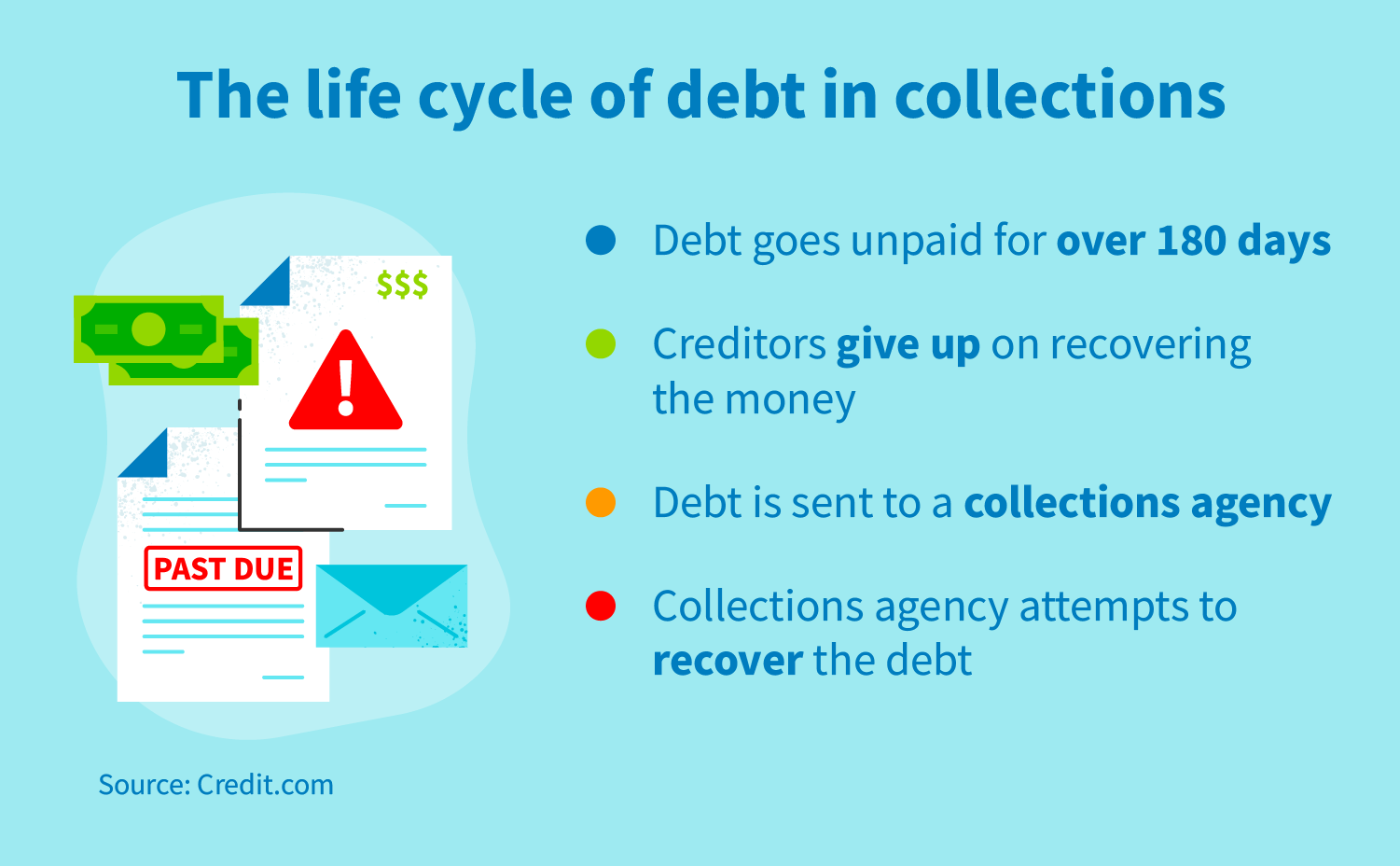

Now, the burning question: can credit repair companies actually remove collections? The answer is… complicated. Legitimate credit repair companies can help you by disputing inaccurate, incomplete, or unverifiable information on your credit report. If a collection account is legitimately yours and the information is accurate, it's unlikely a credit repair company can simply make it disappear. They can't perform magic. They operate within the confines of the Fair Credit Reporting Act (FCRA).

However, here's where they can be helpful: they can handle the tedious process of sending dispute letters to the credit bureaus and collection agencies. They can also help you understand your rights under the FCRA. The key is to understand the limitations. You can do everything a credit repair company does yourself. It just requires time, effort, and a willingness to learn the process.

So, how can you enjoy the benefits of credit repair, whether you do it yourself or hire a company, more effectively? First, get a copy of your credit report from all three major bureaus (Equifax, Experian, and TransUnion). Thoroughly review each report for errors or inaccuracies. If you find something, gather supporting documentation. Then, send a dispute letter to the credit bureau reporting the error. Be patient and persistent. It can take time to see results. And finally, be wary of companies that promise guaranteed results or ask for upfront fees before providing any services. Legitimate companies typically charge after services are rendered.

Ultimately, the best way to "repair" your credit is to practice good financial habits: pay your bills on time, keep your credit card balances low, and avoid taking on more debt than you can handle. Think of it as proactive credit maintenance rather than reactive repair. And remember, while credit repair companies can be helpful in certain situations, they're not a substitute for responsible financial management. A solid financial foundation is the best guarantee of a healthy credit score.