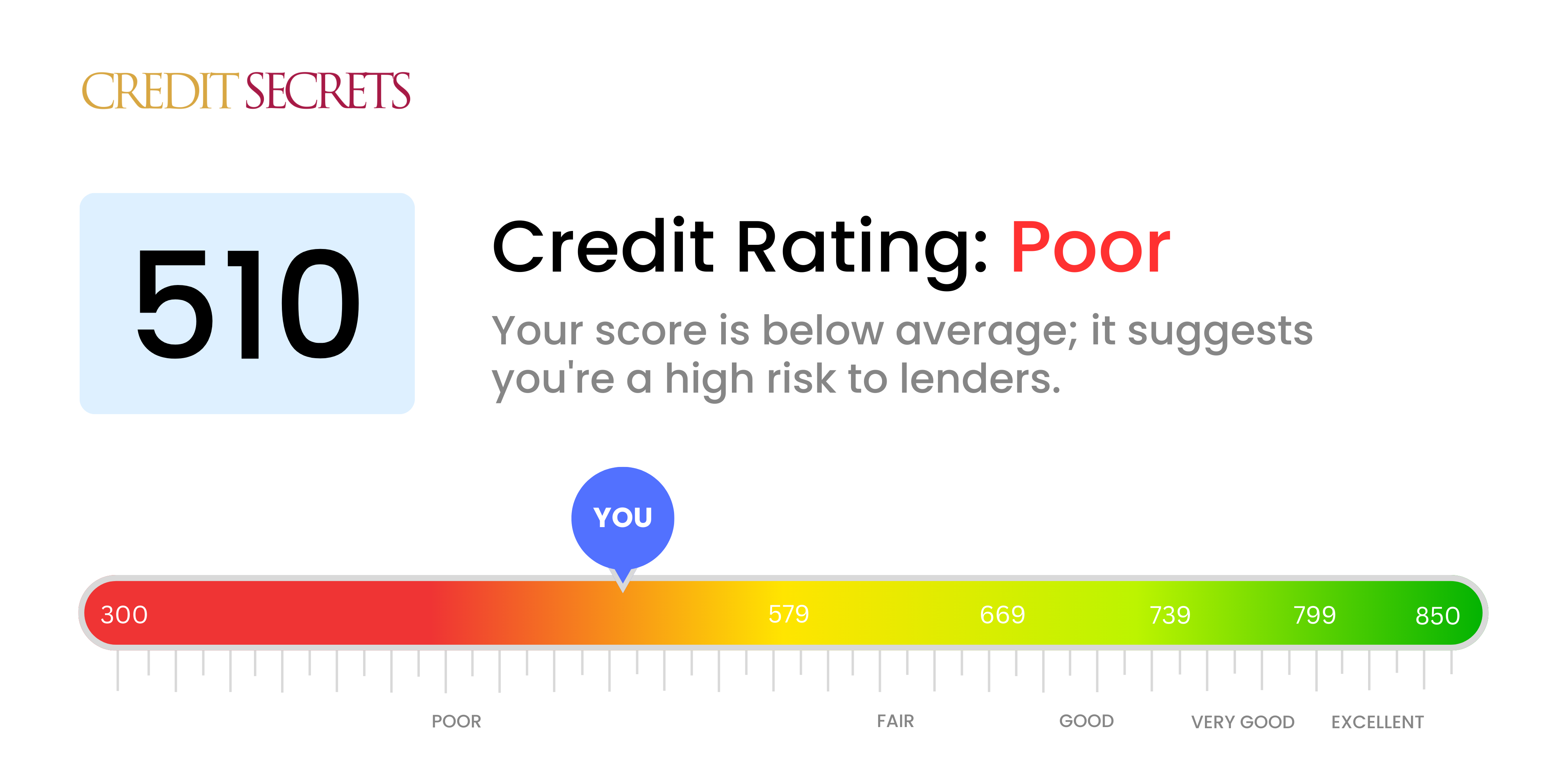

510 Credit Score Personal Loan

Okay, picture this: You're me, except maybe you're wearing slightly less embarrassing socks. You're scrolling through Instagram, and BAM! An ad pops up for the perfect vintage armchair. The price? Ridiculously low. The catch? You need cash, and you need it now. Problem is, your credit score is...let's just say it's not exactly gracing the cover of "Financial Times" magazine. We're talking sub-par, under-the-weather, decidedly 510 credit score territory. Been there? Yeah, me too. That's when the dreaded question hits: can you even get a personal loan with a credit score like that?

Spoiler alert: it's not going to be a walk in the park. But despair not, dear reader! We're going to dive deep into the world of personal loans for those of us with… shall we say, evolving credit histories. Let's get started!

What Exactly IS a 510 Credit Score Loan?

Alright, first things first. A "510 credit score loan" isn't actually a specific loan product labeled as such. It simply means you're trying to get a personal loan with a credit score hovering around the 510 mark. This falls squarely into the "poor" or "very poor" credit range. Ouch.

Must Read

Now, lenders use your credit score as a key indicator of how likely you are to repay the loan. A lower score suggests a higher risk. Think of it like this: they're essentially betting on you, and a 510 score is like betting on a horse that's currently facing the wrong way. It's not impossible, but it's definitely riskier for them. (And potentially expensive for you!)

The Challenges of Getting Approved

So, what are the actual hurdles you'll face? Be prepared for a few potential roadblocks:

- Higher Interest Rates: This is the big one. Lenders will charge you significantly higher interest rates to compensate for the increased risk. We're talking potentially eye-watering APRs here. Do the math carefully before you commit!

- Smaller Loan Amounts: Don't expect to get a massive loan. Lenders are likely to offer smaller amounts to minimize their potential losses. That vintage armchair might have to wait.

- Stricter Terms: You might face shorter repayment periods or other restrictions. Always read the fine print! Like, really read it.

- More Scrutiny: Lenders will likely scrutinize your income and employment history more closely to ensure you can actually repay the loan. Be prepared to provide documentation.

Think of it like this: you're basically asking someone to loan you money after admitting you're not the best at paying it back. They're going to want some serious reassurance.

Where Can You Look for Loans?

Okay, enough doom and gloom. Where can you actually find lenders willing to work with you? Here are a few options:

- Online Lenders: Many online lenders specialize in loans for people with bad credit. These often have less stringent requirements than traditional banks. Look for reputable companies and compare offers carefully. (Don't fall for anything that sounds too good to be true - it probably is!)

- Credit Unions: Credit unions are often more flexible than banks and may be willing to work with you, especially if you're already a member. It's worth checking!

- Secured Loans: Consider a secured loan, where you put up collateral (like your car) to back the loan. This reduces the lender's risk and can increase your chances of approval. (Just make sure you can actually repay the loan, or you could lose your collateral!)

- Payday Loans (Proceed with EXTREME Caution!): These are short-term, high-interest loans that should be an absolute last resort. The interest rates are often astronomical, and they can easily trap you in a cycle of debt. Seriously, explore all other options first.

- Ask Friends or Family: While potentially awkward, borrowing from friends or family can be a lower-cost alternative. Just make sure you have a clear agreement in writing and stick to it to avoid damaging relationships.

Remember: Shop around! Compare offers from multiple lenders to find the best terms and interest rates. Don't just jump at the first offer you see. It's like dating – you want to see what else is out there!

The Better Option: Focus on Improving Your Credit Score

Honestly, getting a loan with a 510 credit score is generally not the best long-term solution. The high interest rates can make it difficult to repay the loan, and you might end up digging yourself into a deeper financial hole. A far better strategy is to focus on improving your credit score.

How? Here are a few quick tips:

- Pay your bills on time, every time. This is the single most important factor in your credit score. Set reminders, automate payments, do whatever it takes!

- Reduce your credit card balances. Aim to keep your credit utilization (the amount of credit you're using compared to your total credit limit) below 30%.

- Dispute any errors on your credit report. Get a free copy of your credit report from AnnualCreditReport.com and check for any inaccuracies.

- Become an authorized user on someone else's credit card (with their permission, of course!). Their good credit habits can help boost your score.

Raising your credit score takes time and effort, but it's an investment that will pay off in the long run. Think of it as planting a financial tree – it might take a while to grow, but eventually, you'll reap the rewards.

So, back to that vintage armchair. Maybe it's not in the cards right now. But with a little effort and some smart financial decisions, you can get your credit score up and get that armchair (and a whole lot more!) on much better terms. You got this!