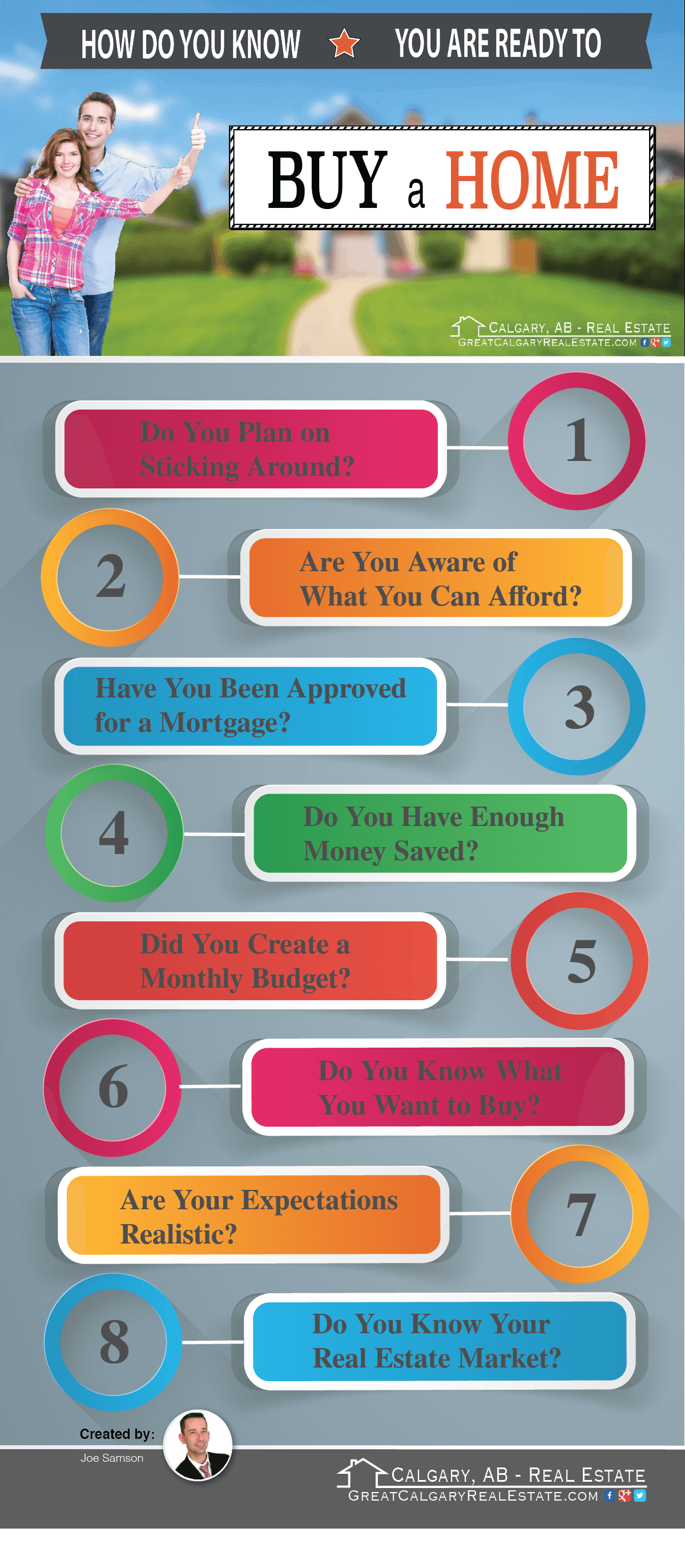

What You Need To Buy A House

So, you’ve decided you want to buy a house. Congratulations! It’s a huge, exciting step, like graduating from renting a tiny apartment to finally having a place where you can paint a wall without a landlord having a conniption. You’re picturing backyard BBQs, maybe a little garden, or just enough space to finally spread out all your mismatched hobbies. Ah, the dream! But before you start picking out throw pillows, let’s talk about the nitty-gritty: what you actually need to buy this magical abode.

The Big Kahuna: Your Down Payment

This is the Everest of house-buying finances. It’s the chunk of cash that tells the bank, "Hey, I’m serious about this!" Think of it like buying a really, really expensive concert ticket – but for a house that lasts decades, not just two hours. Traditionally, it's 20% of the home's price, which, let’s be real, can feel like saving up for a small yacht. But don't fret! There are programs out there for smaller down payments, sometimes as low as 3.5%. Just remember, the less you put down, the more you usually pay in interest over time, and you might have to pay for something called Private Mortgage Insurance (PMI) – which is essentially a fee for having less equity. So, start squirreling away those pennies like a chipmunk preparing for an apocalypse!

The Sneaky Ninjas: Closing Costs

Ah, closing costs. These are the fees that sneak up on you like a rogue sock in the laundry. You thought you budgeted for the house, right? Nope! These are the "oh, by the way" charges that pop up at the end, often amounting to 2-5% of the loan amount. It’s like buying a brand new car and then, just as you’re about to drive it off the lot, they hit you with "dealer prep fee," "document fee," and "air freshener placement fee." These can include everything from lender fees, title insurance (because you want to make sure no one else secretly owns your new castle!), escrow fees, and recording fees. It’s a laundry list of things you never knew existed until you bought a house. Always ask for an estimate early!

Must Read

The Safety Net: An Emergency Fund

You’ve got the down payment, you’ve got the closing costs, you’re practically a homeowner! But hold your horses. What happens when, two months in, the water heater decides it’s had enough and bursts like a sad, rusty piñata? Or when that charming old oak tree in the front yard drops a branch right through your brand new roof? Owning a home means you’re the landlord, the handyman, and the emergency plumber all rolled into one. Having an emergency fund post-purchase is crucial. Think of it as your grown-up "break glass in case of emergency" fund for your house. Aim for at least 3-6 months of living expenses, especially since unexpected home repairs can hit harder than a rogue golf ball.

The Gatekeepers: Inspection & Appraisal Fees

Before you commit to your new home, you'll need to pay for a couple of important check-ups. First, the home inspection. This is where a professional goes through the house with a fine-tooth comb, looking for hidden horrors like faulty wiring, leaky pipes, or foundations that look like they’ve had a rough night out. It's like getting a full physical for your house – and it can save you from buying a money pit. Then there’s the appraisal fee. The bank wants to make sure the house is actually worth what you’re paying for it. They're not going to lend you a huge sum if the house is secretly a cardboard cut-out. These fees might feel like extra hurdles, but they’re vital for protecting your investment.

The Shield: Homeowner’s Insurance

Once you own your slice of heaven, you’ll need to protect it. Homeowner’s insurance is your shield against everything from fires and floods (depending on your policy) to that rogue squirrel who somehow makes a home in your attic. Most lenders won’t even give you a mortgage without proof of insurance, and for good reason. It’s peace of mind, knowing that if disaster strikes, you won’t be starting from scratch. Think of it like putting a really good, heavy-duty case on your expensive new smartphone – you hope you never drop it, but if you do, you’re covered.

The Logistics: Moving & Initial Setup

You’ve bought the house, signed a million papers, and probably eaten way too many free pens. Now, you actually have to move into it! Whether you’re bribing friends with pizza and beer or hiring professional movers, there’s a cost involved. Then there are those initial setup costs: changing the locks (definitely do this!), maybe a fresh coat of paint, new curtains because the previous owner’s taste was… vibrant, and all those little things that turn a house into your home. Don’t forget about setting up utilities – electricity, water, internet – which often come with activation fees. It all adds up faster than you can say, "Honey, where did we put the box with the toaster?"

The Non-Monetary Essentials: Patience and A Good Team

While not a direct financial cost, these are priceless. Buying a house is a marathon, not a sprint. There will be paperwork, waiting, maybe a few bumps in the road, and moments when you want to scream into a pillow. You’ll need patience, a good real estate agent who understands your quirks, a responsive lender who answers your frantic calls, and maybe a supportive partner or friend to remind you to breathe. It’s a journey, but standing in your very own space, knowing it’s all yours, is one of the most rewarding feelings there is. You’ll get there, and it will be absolutely worth every single penny and every moment of frantic searching for "the one."