Is A New Roof A Tax Deduction

Alright, settle in, grab another imaginary coffee (or a real one, I won't judge), because we're about to tackle a question that haunts many a homeowner's dreams, usually around the same time they're staring at an estimate with more zeros than a lottery jackpot: "Is a new roof a tax deduction?"

Oh, the glorious fantasy! Imagine waving that receipt for thousands of dollars at the IRS, expecting a grateful nod and a fat check back. Wouldn't that be just peachy?

The Cold, Hard (and Slightly Humorous) Truth

Let's not beat around the bush. For most of us, living in our primary residence, the answer is a resounding, soul-crushing... no. I know, I know. It stings. It feels like the universe, and specifically the taxman, is conspiring against your perfectly reasonable desire to not have rain fall directly onto your artisanal sourdough starter.

Must Read

The IRS, in its infinite wisdom, views a new roof not as a mere expense, but as a capital improvement. What does that mean in plain English? It means they see it as something that adds significant value to your home, prolongs its useful life, or adapts it to a new use. Basically, it makes your house better, and therefore, it's not just a "cost of living" deduction like, say, medical expenses (which, side note, rarely includes new roofs unless your doctor prescribed a specific shingle type for your debilitating roof-induced anxiety, but more on that in a sec).

Think of it this way: replacing a broken window? Maintenance. Adding a whole new sunroom? Capital improvement. A new roof falls firmly into the latter camp. It's an investment, darling, not a deduction. My condolences.

But Wait! What If My Roof Has a Ph.D. in Energy Efficiency?

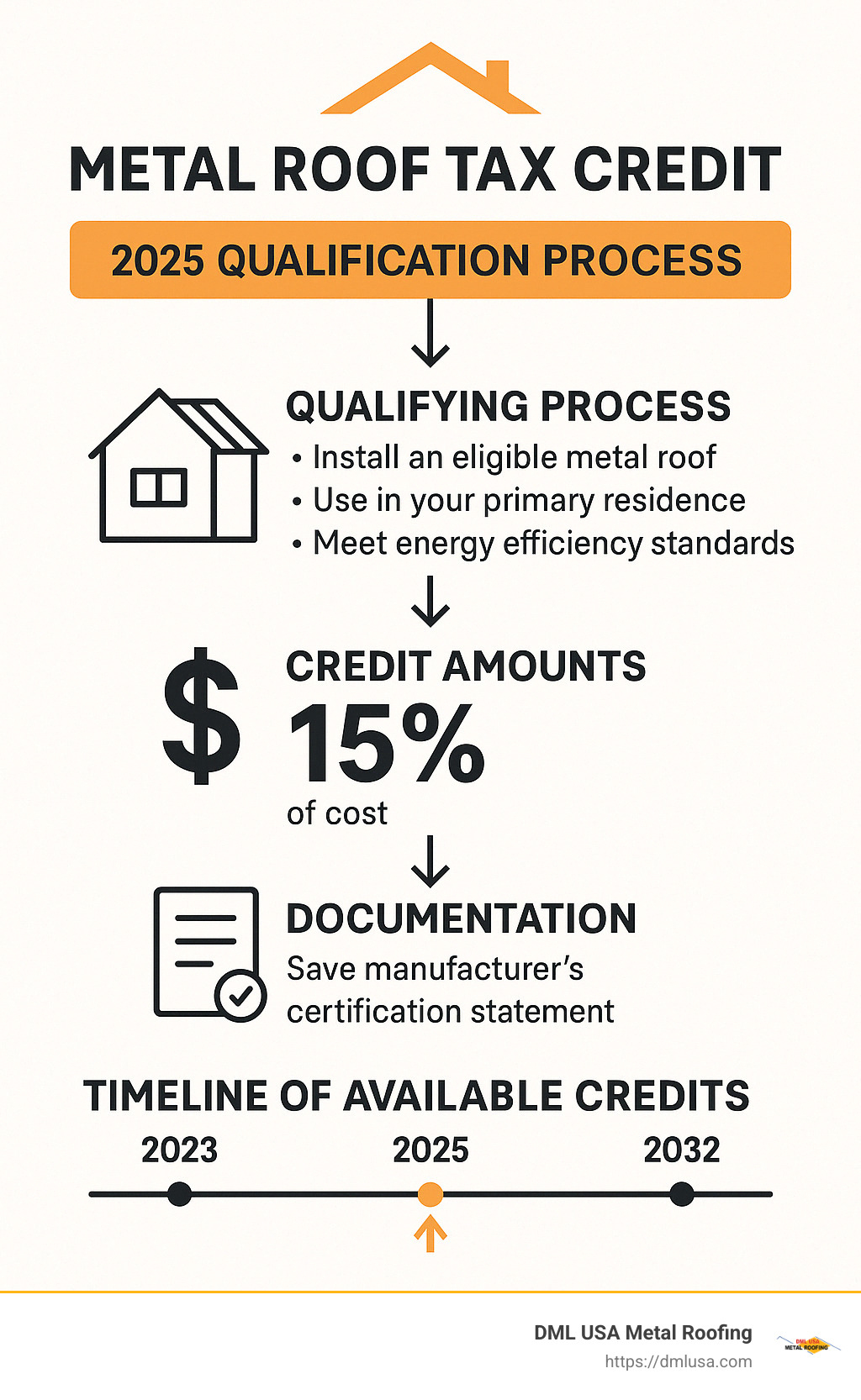

Okay, here's where things get a little less depressing. While the roof itself might not be a direct deduction, certain aspects or types of roofs might qualify for other goodies. We're talking about those lovely energy efficiency tax credits. If your new roof includes things like:

- Solar panels: Ding, ding, ding! Solar energy property is often eligible for federal tax credits.

- Specific cool roof materials: These reflect sunlight and reduce heat absorption, and might qualify for certain residential energy credits if they meet specific energy efficiency standards. But this is for the materials, not the whole shebang.

It's crucial to check the specific requirements for these credits, as they can change, and they often apply to the components that make your home more energy-efficient, rather than the entire structural replacement. It's not a deduction for the roof, but for its super-powered eco-features.

The "Unless It's a Business" Clause (Cue Angelic Choir)

Now, if your home isn't just your personal sanctuary, but also a bustling hub of commerce – say, a rental property or you run a legitimate, IRS-approved home office out of a significant portion of it – then the tax gods smile upon you!

For rental properties, a new roof is considered an improvement that can be depreciated over its useful life (typically 27.5 years for residential rental property). This means you get to deduct a portion of the cost each year. Similarly, if your home office is a dedicated space and meets the IRS criteria, a portion of that new roof's cost could be depreciated as a business expense.

Suddenly, the leaky roof isn't just a headache; it's a business asset! Who knew shingles could be so financially stimulating?

The Catastrophic Caveat: When Disaster Strikes

Did a rogue meteorite mistake your roof for a landing strip? Or perhaps a hurricane decided your shingles were a particularly delicious snack? We're talking about casualty losses. In the past, if your roof was damaged by a sudden, unexpected, or unusual event (not just old age and neglect), you might have been able to deduct the unreimbursed loss.

However, thanks to the Tax Cuts and Jobs Act of 2017, casualty losses for personal property (like your home) are now generally limited to those occurring in a federally declared disaster area. So, unless your roof decided to perform an unscheduled demolition during an actual FEMA-designated emergency, this avenue is pretty much closed for most folks. Bummer, I know. It's like asking for a tax break because your cat decided to play Jenga with your gutters.

The "Basis" of the Situation: A Future Payoff

Even if you can't deduct your new roof now for your primary residence, it's not entirely forgotten by the tax gods. A capital improvement like a new roof adds to your home's cost basis.

Think of your cost basis as your starting price for your home, plus the cost of any significant improvements you've made over the years. When you eventually sell your house (perhaps after it tries to eat you whole with rising maintenance costs), that higher basis means a lower capital gain. A lower capital gain means less tax on the profit from your sale.

It's not a deduction today, but it's like saving dessert for later. A very, very long later, potentially. But hey, a future tax break is still a tax break, right?

So, What Have We Learned From Our Little Café Chat?

In summary:

- For your personal residence, a new roof is generally not a direct tax deduction. Sorry!

- But, energy-efficient components might snag you some tax credits.

- If it's for a rental property or a legitimate home office, you can likely depreciate it! Hooray for landlords and WFH warriors!

- Casualty losses are now largely restricted to federally declared disaster areas.

- And remember, it always increases your cost basis, potentially reducing future capital gains tax.

My final, utterly serious, piece of advice: The tax code is trickier than assembling flat-pack furniture with a missing screw. So, when in doubt, consult a qualified tax professional. They're like the superheroes of spreadsheets, ready to navigate the labyrinthine world of IRS rules so you don't accidentally turn your dream home into a tax nightmare. Now, about that second coffee...