How Do You Start The Process Of Buying A Home

Alright, gather 'round, folks! Let's talk about buying a home. It's like embarking on a quest, except instead of slaying a dragon, you're slaying paperwork. And instead of gold, you get a mortgage. Which, let’s be honest, feels a bit like the dragon got you after all.

Where do you even start? You're probably thinking, "I need to sell my soul to the bank!" Well, not quite. But close. Here's the lowdown:

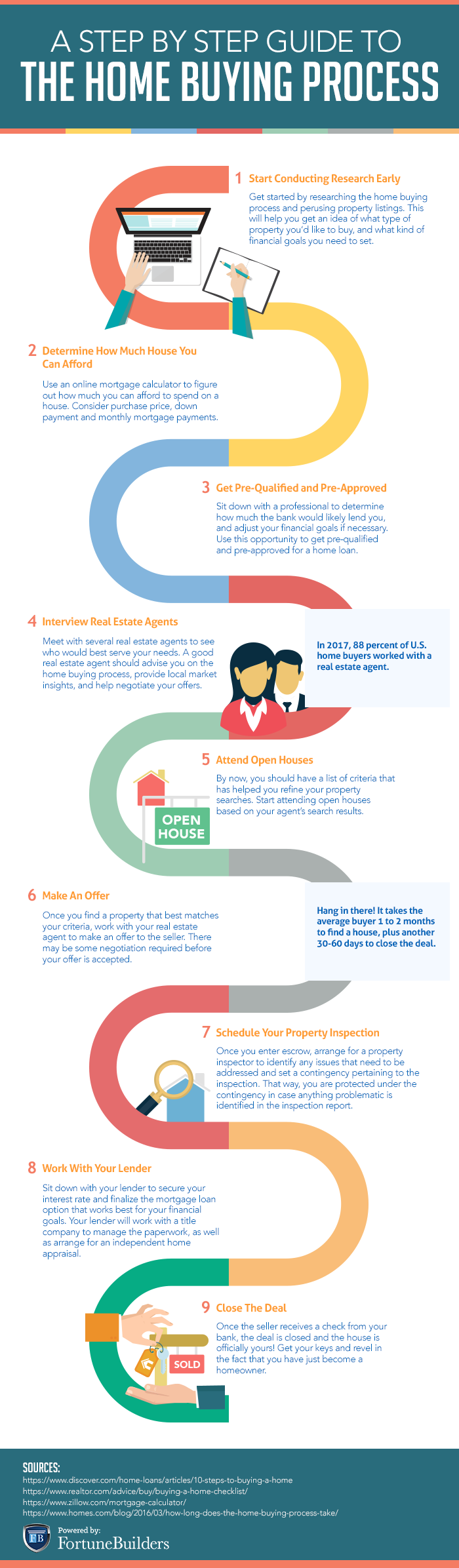

Step 1: Figure Out Your Finances (Before You Fall In Love)

This is the boring part, but trust me, it's like eating your vegetables. You might not like it, but it'll prevent scurvy... or in this case, foreclosure. First, check your credit score. If it looks like it was written by a toddler with crayons, you might have some work to do. Aim for the high 600s, but 700+ is the VIP section.

Must Read

Next, calculate your debt-to-income ratio (DTI). This is how much of your monthly income goes toward debt payments. Lenders love low DTIs. Think of it as showing them you're responsible enough to own a house, and not just spend all your money on avocado toast (guilty!). You calculate it by dividing your total monthly debt payments by your gross monthly income. A good target is below 43%

Now, the down payment. Historically, 20% was the norm. Nowadays? It's more like "whatever you can scrape together." There are loan programs with as little as 3% down, but remember, a smaller down payment means higher monthly payments and potential for private mortgage insurance (PMI), which is basically insurance for the bank in case you decide to elope to Fiji and ditch the mortgage.

Don't forget closing costs! These are all the fees associated with buying a home – appraisal, title insurance, taxes, etc. Budget for 2-5% of the purchase price. Consider it the "Congratulations on Your New Debt!" tax.

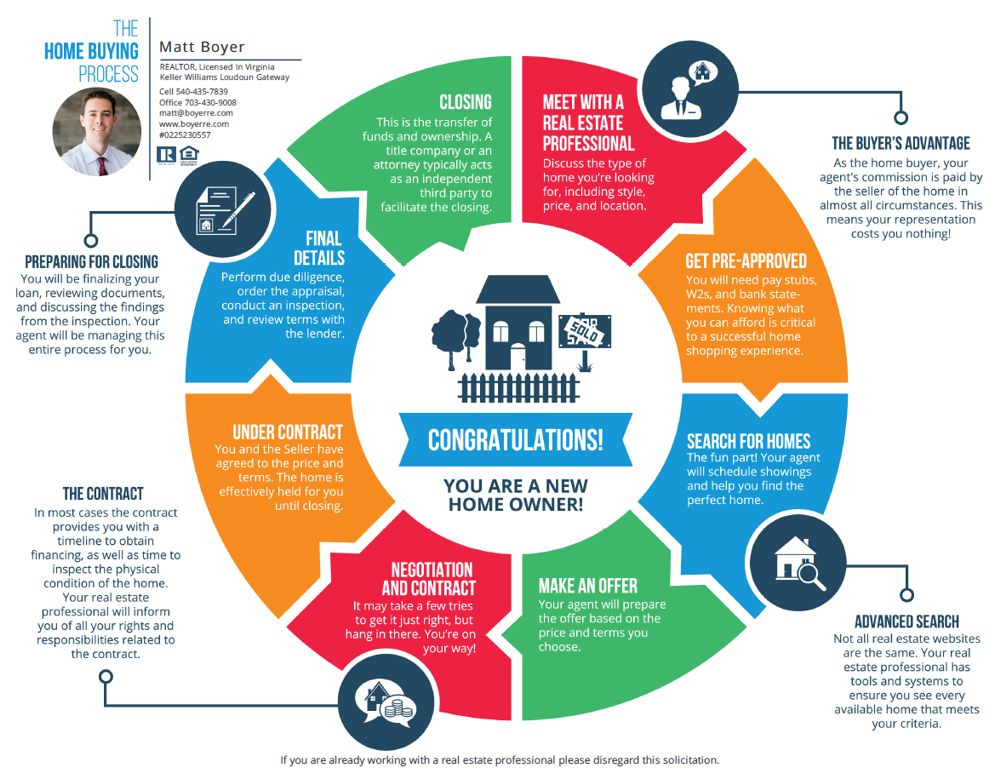

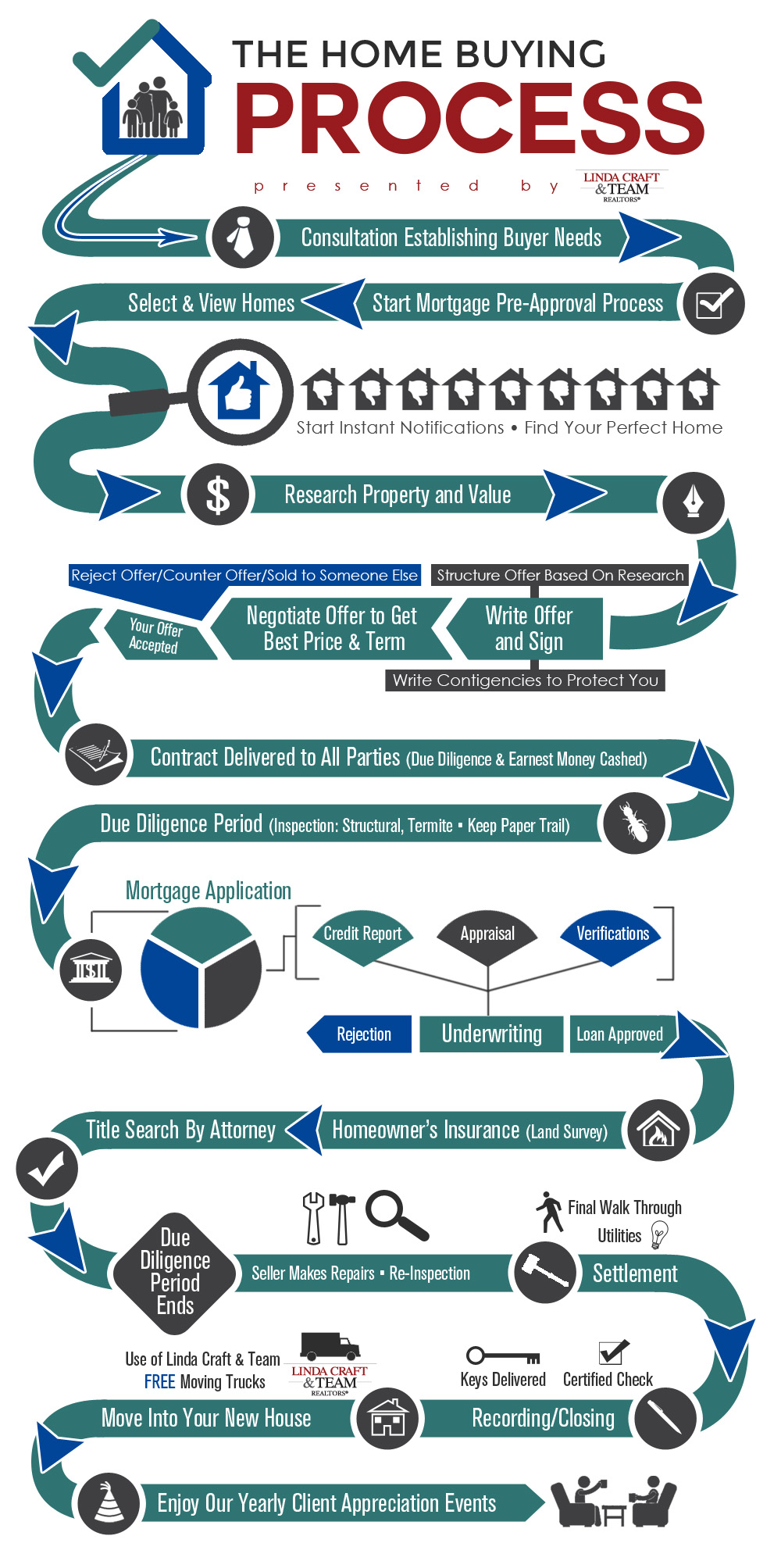

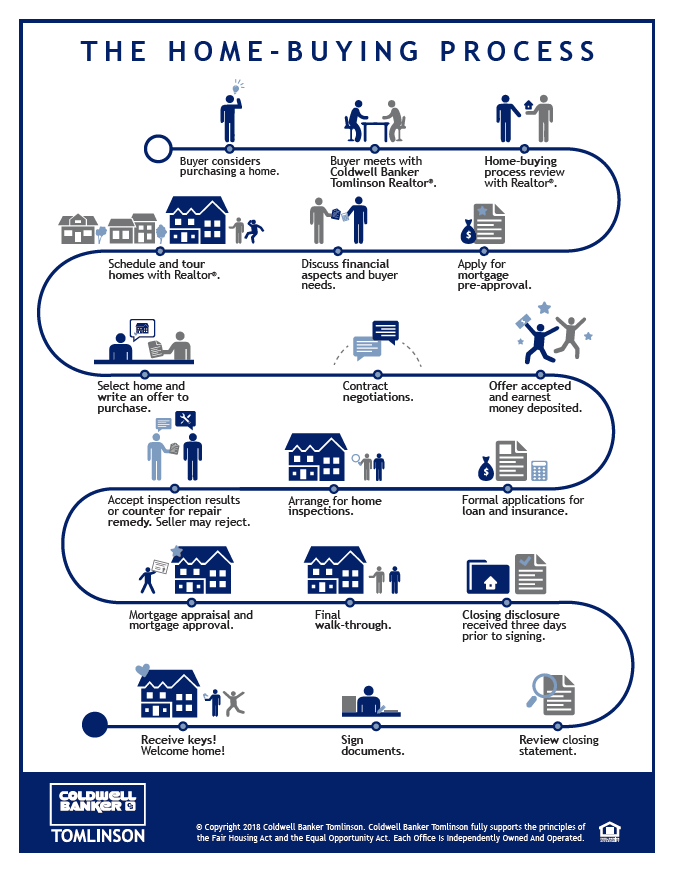

Step 2: Get Pre-Approved (Become a Real Buyer)

Getting pre-approved is like getting a hall pass from the bank. It tells you how much they're willing to lend you. Don't skip this step! Imagine finding the perfect house, picturing yourself sipping lemonade on the porch, only to realize the bank thinks you're about as financially responsible as a squirrel with a credit card.

Shop around for lenders. Banks, credit unions, online lenders – they all offer different rates and terms. It's like dating; don't settle for the first one that calls (unless they're offering, like, 0% interest. Then, maybe...). Getting pre-approved is free, so comparing rates is totally worth it.

Step 3: Find a Real Estate Agent (Your House-Hunting Sherpa)

A good real estate agent is your guide through the house-buying wilderness. They know the market, can spot potential problems, and negotiate on your behalf. Find an agent who actually listens to your needs, not just one who tries to sell you the most expensive house on the block. Ask friends for recommendations and check online reviews. It's like hiring a therapist, but instead of analyzing your childhood, they're analyzing comparable sales.

Step 4: The House Hunt (Embrace the Chaos)

This is where the fun (and the frustration) begins! Start browsing listings online, but be prepared: photos can be deceiving. That "charming cottage" might actually be a dilapidated shack with a raccoon infestation. Go see houses in person with your agent. Don't be afraid to ask questions and poke around. Is the basement damp? Does the roof look like it's about to collapse? These are things you need to know!

Be prepared for a bidding war, especially in a hot market. It can be emotionally draining. Don't get so caught up in the frenzy that you overpay or waive important contingencies. Remember, you're buying a home, not winning the lottery. Stick to your budget, and don't be afraid to walk away.

Step 5: Make an Offer (Hold Your Breath and Hit "Send")

Once you find a house you love (and can afford), it's time to make an offer. Your agent will help you prepare the paperwork, including the price, contingencies (like a home inspection), and closing date. Then, you hold your breath and hope the seller accepts. It's like asking someone on a date, but with way more money involved.

Step 6: The Home Inspection (Uncover the Secrets)

If your offer is accepted, congratulations! But don't break out the champagne just yet. The home inspection is crucial. A qualified inspector will assess the property for structural problems, pest infestations, and other issues. This is your chance to renegotiate the price or ask the seller to make repairs. Imagine it as a medical check-up for your future home.

Step 7: Closing (Sign, Sign, Everywhere a Sign!)

Once everything is clear, it's time to close the deal. This involves signing a mountain of paperwork. You'll need to bring a cashier's check for the down payment and closing costs. Then, you get the keys! Congratulations, you're a homeowner! Now, go celebrate… after you’ve unpacked the boxes.

Buying a home is a big decision, but with a little planning and a sense of humor, you can survive the process and find your dream home. Just remember, it's not a sprint, it's a marathon… a marathon where you're constantly running out of money and questioning your life choices. But hey, at least you'll have a roof over your head!