Does A Returned Check Affect Credit

Okay, so picture this: Last month, I was feeling all responsible, paying my rent a whole week early. Proud adulting moment, right? WRONG. Turns out, I miscalculated something (don't ask!), and a few days later, BAM! Returned check notice slapped on my door. My first thought? "Oh great, another fee." My second thought? "Wait... is my credit about to tank because of this?" Hence, the burning question we're tackling today: Does a returned check actually affect your credit score?

Let's get right to it. The simple answer? Directly, no. A returned check itself usually won't cause a ding on your credit report. Phew! But before you breathe a sigh of relief and go write another rubber check (please don't!), there's a BIG asterisk here. Think of it like this: the returned check is the symptom, not the disease. The disease? Well, that's the unpaid debt that caused the check to bounce in the first place.

The Real Danger Zone: Unpaid Debts

Must Read

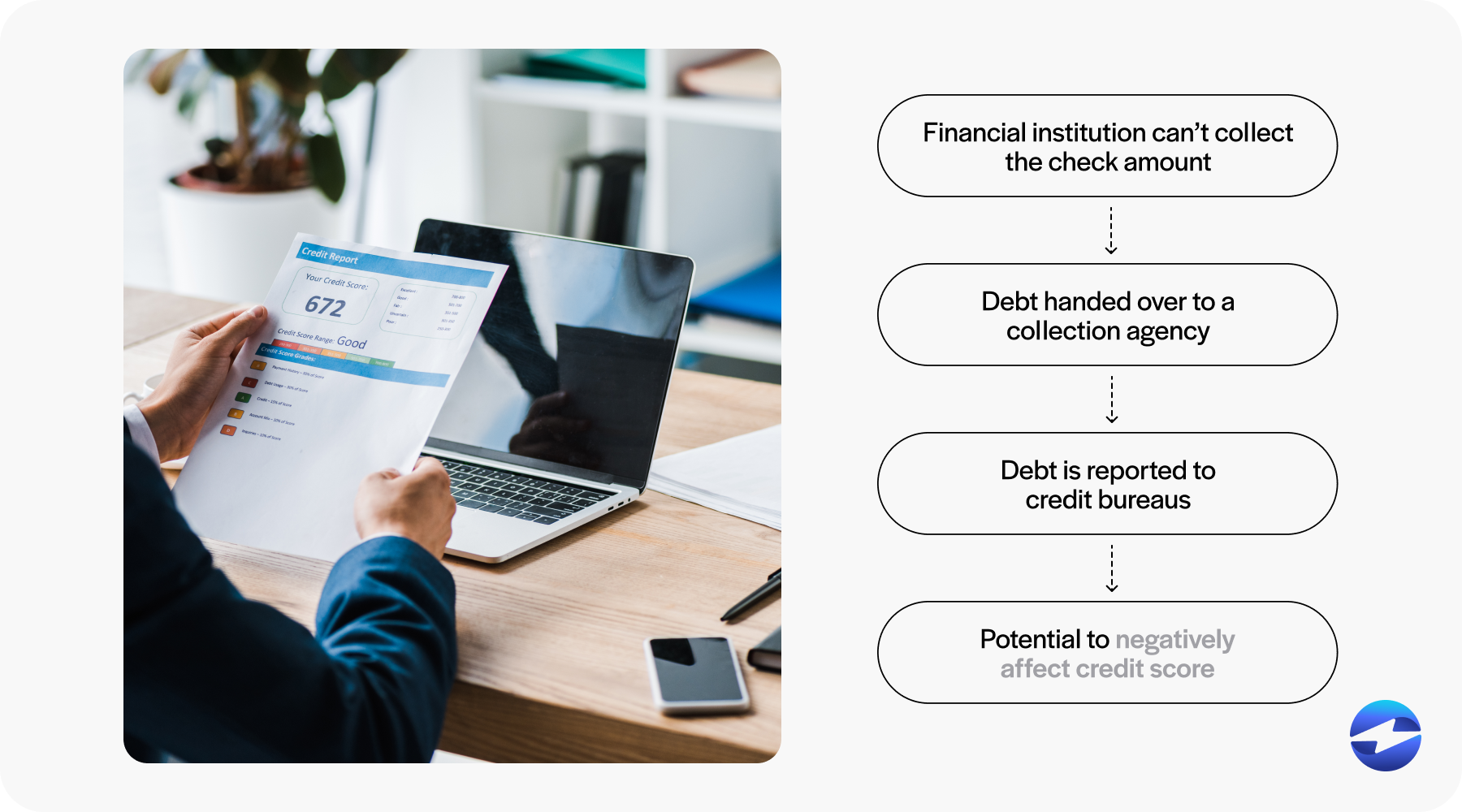

The key takeaway is this: if you don't resolve the underlying issue that caused the check to bounce, that's when things can go south, credit-wise. How? Glad you asked!

Imagine you wrote that check for your credit card bill. It bounces. Now you've got the original bill amount plus a bounced check fee from your bank, plus a late fee from the credit card company. See how quickly that escalates? If you ignore the situation, the credit card company might eventually report the delinquent account to the credit bureaus. And that, my friends, is a direct hit to your credit score.

Think of it like dominoes. The returned check knocks over the "unpaid debt" domino, which then knocks over the "negative credit report" domino. You want to stop the chain reaction before it reaches your credit score.

So, What Should You Do If a Check Bounces?

First, don't panic. We all make mistakes (yes, even responsible-seeming adults like myself!).

Second, act fast. Contact the person or company you wrote the check to immediately. Explain the situation, apologize (sincerity goes a long way!), and ask about their preferred method of payment. Offer to pay the original amount, plus any fees they incurred.

Pro Tip: Offer to pay with a method that guarantees instant payment, like a debit card or a money order. This shows you're serious about resolving the issue and avoids any further delays.

Third, check your bank account balance religiously. Seriously. Avoid future "oops" moments by keeping a close eye on your funds. Set up low-balance alerts so you're notified if your account dips below a certain level. (Your future self will thank you!)

Fourth, communicate with your bank. They may be able to reverse fees or offer a payment plan if you're facing temporary financial difficulties. It never hurts to ask!

The Bottom Line

While a returned check itself isn't a credit score killer, ignoring the underlying debt definitely is. Treat a bounced check as a wake-up call to address your finances promptly. By taking swift action and communicating with the affected parties, you can prevent a minor mishap from turning into a major credit score disaster. Remember, proactive management is key to maintaining a healthy credit history. Nobody wants their rent payment faux pas haunting them for years to come!

And hey, we've all been there. Mistakes happen. Just learn from them, fix them, and keep on adulting!