What Do You Need To Get A House

So, you've got that twinkle in your eye, huh? The one that screams, "I want my own four walls, a garden, and maybe a ridiculously oversized dog!" Yeah, I know that feeling. It's exciting, right? But then the panic sets in. "What do I actually need to get a house?" It feels like this mythical quest sometimes, a secret handshake you're not in on. Well, pull up a chair, grab another coffee. Let's spill the beans, friend to friend, about what it really takes.

First Up: The Big Kahuna – Money, Honey!

I know, I know. It's always about the cash. But let's be real, you're not going to magic a house into existence. So, what kind of dough are we talking about?

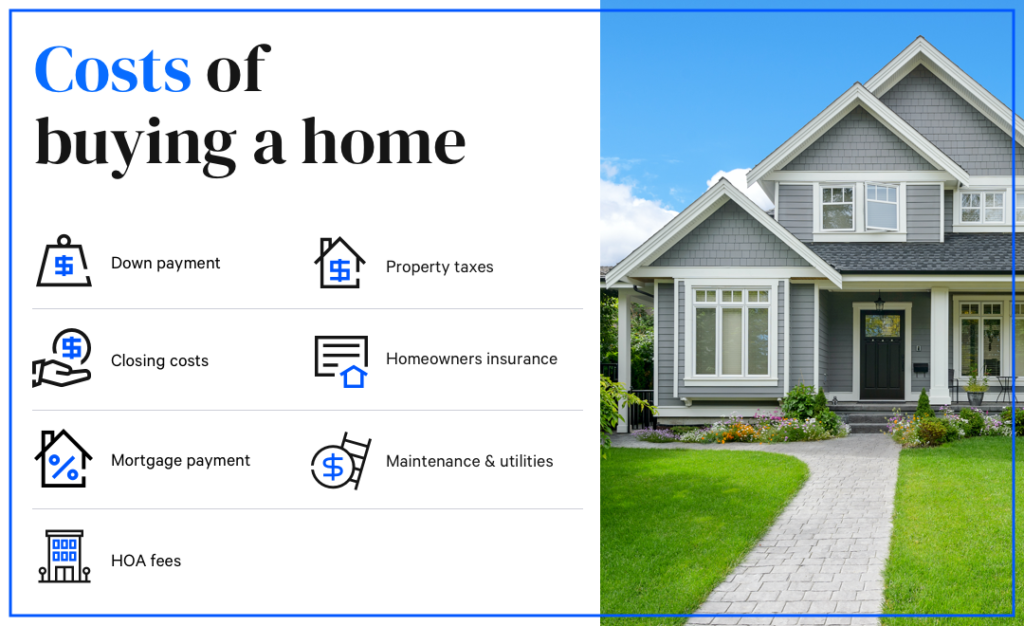

The Down Payment: This is the one everyone stresses about. "You need 20%!" they screech. And sure, 20% is fantastic if you have it. It means lower monthly payments and no private mortgage insurance (PMI). But guess what? It's not always mandatory! There are programs out there for 3.5%, 5%, even 0% down for certain loans (hello, VA and USDA!). So, don't let that 20% myth scare you off before you even start looking. Just remember, the more you put down, the better off you'll be.

Must Read

Closing Costs: Oh, the sneaky little devils! These are the fees you pay at the very end of the process, for all the legal stuff, appraisals, title insurance, and a bunch of other things that make your head spin. They can add up to 2-5% of the loan amount! So, if you're buying a $300,000 house, we're talking another $6,000 to $15,000. Don't forget to budget for these! They often catch people by surprise.

An Emergency Fund (Post-Purchase): This is crucial, my friend. Once you're in, things will break. Your water heater will decide to retire early, the dishwasher will stage a protest. Trust me on this. Having at least three to six months of living expenses stashed away after you close is a lifesaver. It’s your "oh crap" fund, and it prevents you from instantly regretting your new homeowner status.

A Realistic Budget: Before you even dream of granite countertops, sit down and figure out what you can actually afford each month. Utilities, maintenance, potential HOA fees, property taxes – it's more than just the mortgage payment. Be brutally honest with yourself. This isn't the time for wishful thinking!

The Paper Trail Tango: Documents & Decisions

Alright, money checked. Now for the paper mountain. Yes, it feels like a mountain, but it's manageable.

A Sparkling Credit Score: This is your financial report card, and lenders love a good one. A higher score means you qualify for better interest rates, which can save you tens of thousands over the life of the loan. So, pay your bills on time, keep credit card balances low, and maybe lay off opening a bunch of new credit lines right before you apply for a mortgage. Good credit equals better deals!

Loan Pre-Approval (Get This EARLY!): Seriously, this isn't just a suggestion; it's a non-negotiable first step. It shows sellers you're a serious buyer, not just a window shopper. A lender will look at your finances and tell you exactly how much they're willing to lend you. This means you know your budget, and you won't fall in love with a house you can't afford. It's like having a golden ticket in your hand!

All The Documents: Get ready to share your life story through paper. Pay stubs, W-2s, tax returns from the last two years, bank statements, investment account statements... you name it, they'll want it. Start gathering these things now to save yourself some stress later.

Your Home-Buying Dream Team

You don't have to do this alone! In fact, please don't. You need some pros on your side.

A Kick-Ass Real Estate Agent: This person is your guide, your negotiator, your therapist, and your local market guru all rolled into one. Find someone you trust, who understands what you're looking for, and who isn't afraid to fight for you. They're usually paid by the seller, so it costs you nothing as a buyer! Choose wisely, they are your champion!

A Savvy Mortgage Lender or Broker: This is the person who actually gets you the loan. They'll walk you through all the options, explain the rates, and help you navigate the financial maze. Shop around for this one! Different lenders offer different rates and fees. Find someone who explains things clearly and has your best interests at heart.

A Thorough Home Inspector: Once you find "the one," this person swoops in to make sure it's not actually "the lemon." They'll check the roof, the foundation, the plumbing, the electrics – basically, everything you probably wouldn't think to look at. Their report is invaluable, potentially saving you from huge headaches (and costs!) down the line. Don't skip the inspection!

Finally: Patience and a Good Attitude!

Look, buying a house is a big deal. It's often stressful, sometimes frustrating, and occasionally exhilarating. Things will probably go wrong, or at least not exactly as planned. That's okay! Take a deep breath.

Patience is a Virtue: It's not a sprint; it's a marathon with lots of paperwork obstacles. Be prepared for things to take time. The right house will come along. The right loan will get approved. Trust the process (and your team).

Flexibility: You might not get every single thing on your wish list, and that's totally fine. Be open to compromises. A slightly smaller yard for a better kitchen? A different neighborhood for a lower price? Keep an open mind!

So, there you have it. It’s not a secret formula, just a combination of financial readiness, a little bit of paperwork stamina, and a great team. You absolutely can do this! Now go forth and conquer that housing market. And maybe invite me over for that housewarming party, okay?