What Do I Need To Buy A House

Ever caught yourself scrolling through dreamy real estate listings, imagining your perfect kitchen or that sun-drenched backyard? It's a fun game, right? But then the little voice in your head pipes up: "Wait, what do I actually need to buy a house?"

For many, the idea of homeownership feels like a giant, mysterious mountain. You know it's there, you know people climb it, but the path seems hidden in the clouds. Well, good news! It's not nearly as intimidating once you break it down. Think of this as your friendly chat over coffee, demystifying the whole thing. We're not talking rocket science here, just some practical steps and a sprinkle of savvy planning.

The Money Stuff: More Than Just the Price Tag

Let's tackle the financial side first, because, let's be honest, that's often the biggest question mark. But don't fret! It's not about being rich; it's about being prepared.

Must Read

First up, the big one: the down payment. This is essentially your initial chunk of money that goes towards the house's purchase price. Think of it like a really big, long-term security deposit. It shows you're serious and reduces how much you need to borrow.

How much do you need? This is where it gets interesting! While the old 20% rule is often touted, it's not the only way. Many conventional loans allow for as little as 3-5% down. And then there are government-backed loans, like FHA loans, which can go as low as 3.5%, or VA and USDA loans which, for eligible buyers, might even offer 0% down! Pretty cool, right? It really opens up possibilities. The more you put down, the less you borrow, which usually means lower monthly payments and potentially less interest over time. But don't let a lower percentage stop you from starting your journey!

Next on the money menu are closing costs. Ah, the "hidden fees" everyone whispers about. These are essentially the administrative and legal fees associated with finalizing your home loan and transferring ownership. They cover things like appraisal fees, title insurance, legal fees, recording fees, and loan origination fees. Think of it like the "setup fee" for joining an exclusive club – your new home! They typically range from 2-5% of the loan amount, and yes, they're paid upfront when you close on the house. So, while you're saving for that down payment, remember to tuck away a little extra for these necessary expenses.

And finally, a crucial but often overlooked component: an emergency fund or buffer. Once you're a homeowner, suddenly that leaky faucet or broken furnace is your problem. Having a cushion of 3-6 months' worth of living expenses is incredibly smart. It's like having spare batteries for your new gadget – you hope you don't need them right away, but you're super glad they're there when you do!

Beyond the Benjamins: Your Financial Fingerprint and VIP Pass

Money isn't the only player in this game. Lenders want to know you're reliable. This is where your financial reputation steps in.

Your credit score is super important. It's like your financial report card, telling lenders how good you are at managing debt. A higher score typically means you're seen as less risky, potentially qualifying you for better interest rates – saving you thousands over the life of your loan! Paying bills on time, keeping credit card balances low, and not opening too many new accounts are all ways to give your score a healthy boost. It's worth a little effort, wouldn't you agree?

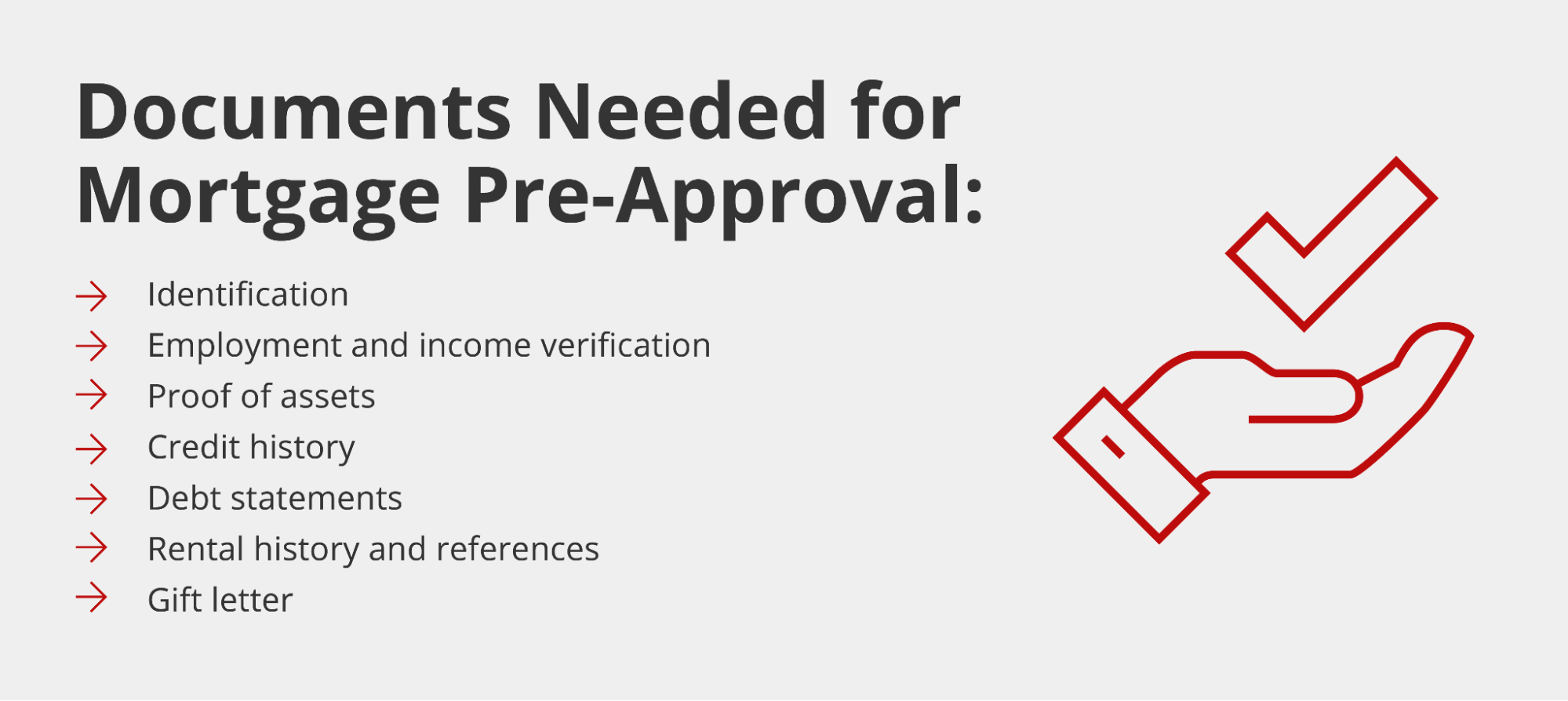

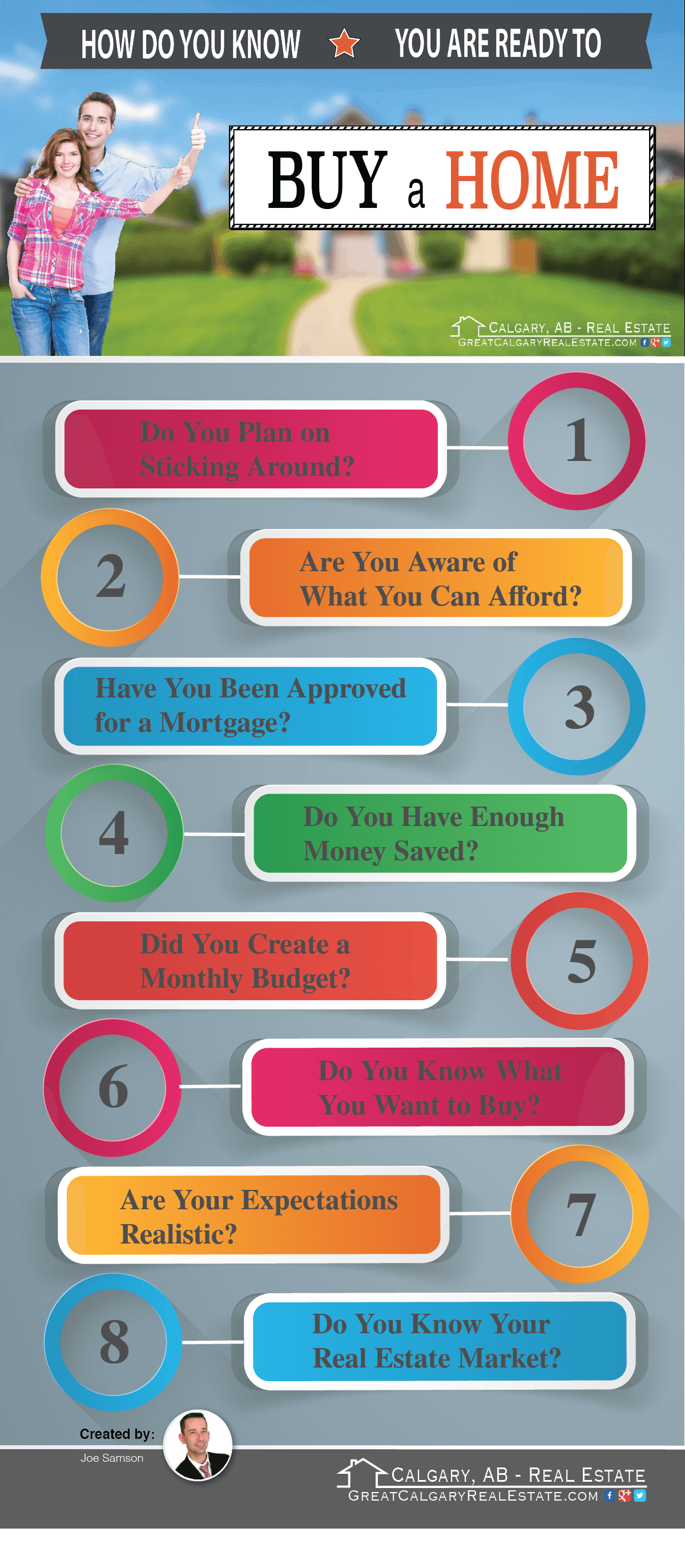

Once your finances are looking good, you'll want to get a mortgage pre-approval letter. This isn't just a fancy piece of paper; it's your VIP pass to serious house hunting! A lender will review your income, assets, and credit to give you an official estimate of how much they're willing to lend you. This shows sellers you're a serious, qualified buyer, giving you a competitive edge in today's market. Imagine walking into an open house already knowing you can afford it – pretty empowering, right?

The Soft Skills: Patience, Perseverance, and a Little Fun

Buying a house isn't always a straight line from A to B. There might be bumps, bidding wars, or just the sheer volume of choices. That's why patience and perseverance are your best friends.

Don't get discouraged if the first few houses aren't "the one." Enjoy the process! Think of it as an adventure. What truly matters to you? Is it proximity to parks, a certain school district, or simply a cozy fireplace? Envision yourself living there, hosting friends, or just relaxing after a long day. This is a journey to finding your personal sanctuary, not just a transaction.

Ultimately, buying a house is a big step, but it's a completely achievable one for many. It requires some planning, some saving, and a little bit of homework. But knowing what you need to buy a house transforms that intimidating mountain into a clear, exciting path. So, go ahead, keep scrolling those listings. Now you've got a better idea of how to turn that dream into a reality!