How To Report Utility Payments To Credit Bureaus

Okay, so you’re the responsible adult type. You pay your bills – rent, utilities, that subscription box you swore you’d cancel six months ago – pretty much on time. High five! But here’s a thought: are you getting any credit for being so darn responsible?

See, traditionally, only things like credit cards and loans get reported to the credit bureaus. Paying your electric bill? Nada. It’s like being a silent champion, running marathons of responsibility, but nobody’s handing out participation trophies (or a better credit score, which is basically the grown-up version of a trophy).

The good news? You can get your utility payments reported. It’s a little like convincing your pet hamster that its treadmill is a worthwhile investment – it takes some effort, but the potential payoff is worth it. Especially if you're trying to boost your credit score. Think of it as adding sprinkles to your already pretty good financial sundae!

Must Read

Why Bother? (Besides Bragging Rights, Obviously)

Why go through the hassle? Well, a solid credit score is like having a golden ticket to financial freedom. It affects everything from the interest rates you get on loans (car, mortgage, etc.) to whether you can even rent an apartment. A good score can save you thousands of dollars over your lifetime. Plus, it makes you look super impressive at dinner parties. (Okay, maybe not, but you'll feel good about it!)

Reporting utility payments can especially help those with thin credit files, meaning they don’t have a lot of credit history. It’s like finally having evidence to show you're not a financial gremlin!

How To Actually Do This Thing

Alright, let’s get down to brass tacks. This is where things can get a little… involved. Buckle up.

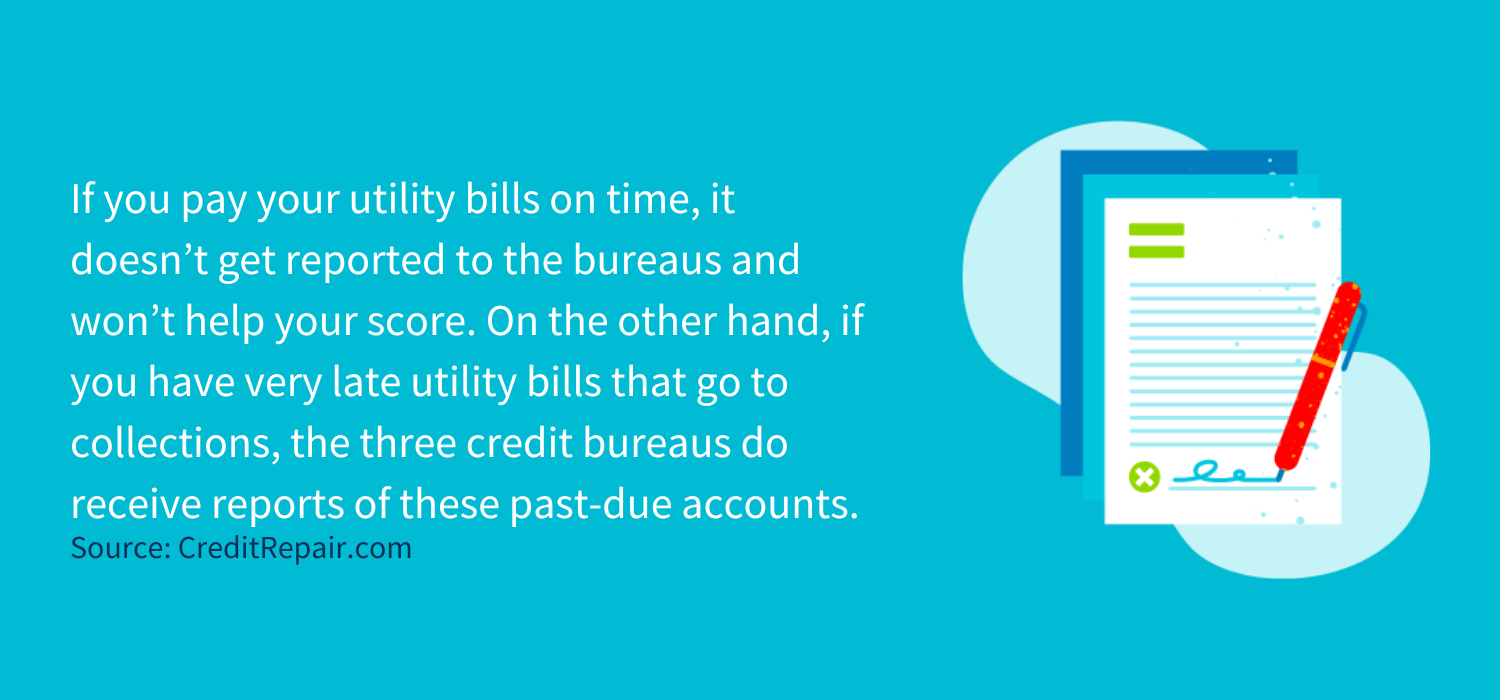

1. Check If Your Utility Company Reports: This is the first hurdle. Most utility companies don’t automatically report to the big three credit bureaus (Equifax, Experian, and TransUnion). It's like expecting your cat to automatically refill its food bowl – it just doesn't happen. So, you'll need to do some digging. Call your utility company and ask directly. Don’t be shy! Channel your inner investigative reporter.

2. Use a Third-Party Reporting Service: If your utility company is a no-go (which is likely), don't despair! This is where third-party services come in. These are companies that specialize in reporting things like rent and utility payments to the credit bureaus. Some popular options include Experian Boost and Self Lender. These services essentially act as a middleman, verifying your payments and reporting them to the credit bureaus. Think of it as hiring a financial translator to speak the credit bureau's language for you.

3. Experian Boost: Experian Boost is a popular and relatively easy option. It links to your bank accounts and identifies recurring utility payments. Then, with your permission, it adds those payments to your Experian credit report. It's kind of like giving Experian permission to snoop through your financial closet, but in a helpful way.

4. Other Services: There are other services out there too, so do your research. Some may charge a fee, while others are free. Be sure to read the fine print and understand what you're signing up for. You don’t want to accidentally subscribe to a service that sends you monthly newsletters about the history of plumbing (unless you’re into that sort of thing).

Important Considerations (The Fine Print Blues)

Before you jump in headfirst, there are a few things to keep in mind:

- Reporting can take time. Don't expect your credit score to magically jump overnight. It takes time for the information to be processed and reflected on your credit report. Patience, young grasshopper.

- Not all payments are created equal. The impact of utility payments on your credit score may not be as significant as, say, paying off a credit card balance. But every little bit helps! Think of it as adding pebbles to a mountain – eventually, you'll have a mountain of good credit.

- Make sure you're paying on time! Late payments will be reported and can hurt your credit score. This is like accidentally setting your alarm for 3 AM instead of 7 AM – a very unpleasant surprise.

So, there you have it. Reporting utility payments to credit bureaus isn't the most glamorous task, but it can be a worthwhile way to give your credit score a little boost. And who knows, maybe someday you'll be able to brag about your stellar credit at that dinner party after all!