Do Utility Companies Report To Credit Bureaus

Hey! So, you wanna know if those pesky utility companies—you know, the ones that keep the lights on (literally!)—report to credit bureaus? Let's spill the tea, shall we?

The short answer? It's kinda...complicated. Like, dating in the modern age complicated. Buckle up!

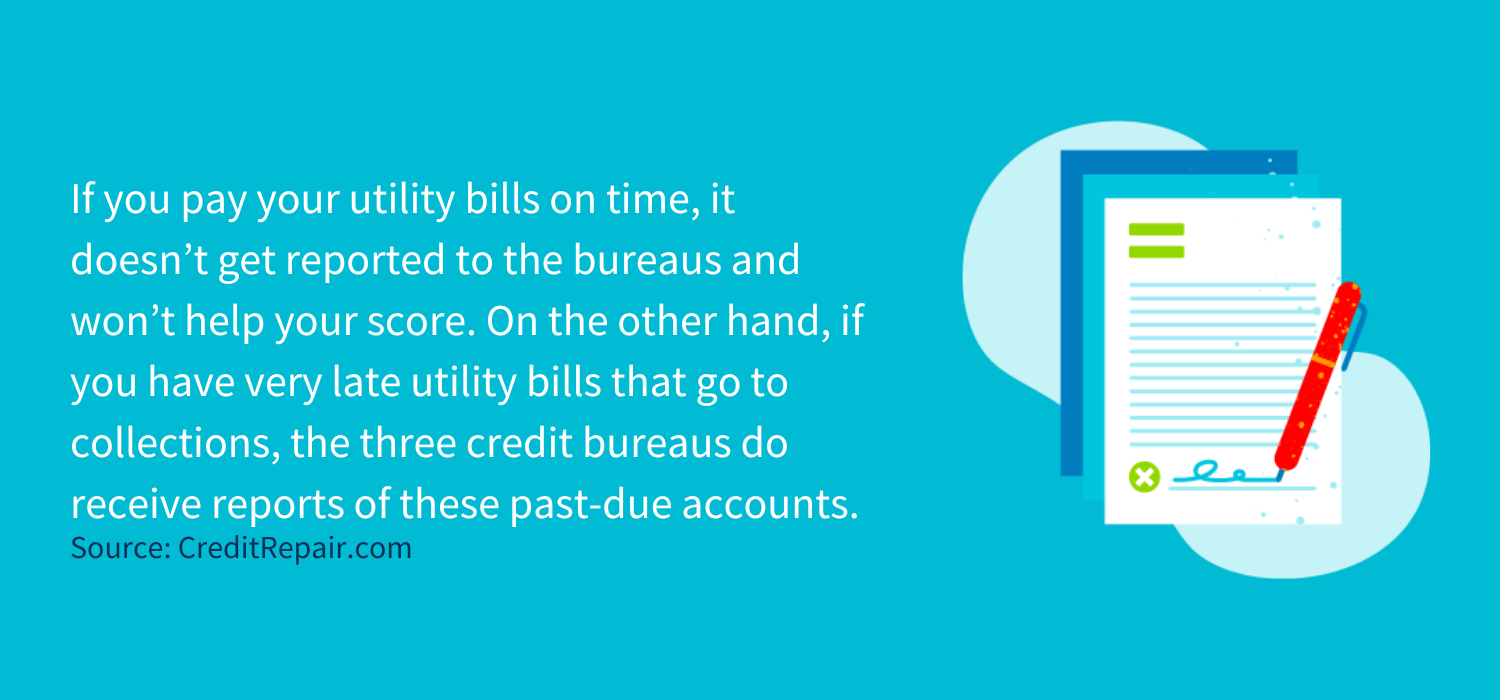

The Simple Truth (Mostly): Most utility companies don't routinely report your on-time payments to the big credit bureaus (Experian, Equifax, and TransUnion). Bummer, right? Imagine all those perfect payment histories just sitting there, unloved and unacknowledged! Seriously, the injustice!

Must Read

Think about it. Paying your electricity bill on time for years? You're a responsible adult! Giving yourself a pat on the back should be worth, like, +50 points on your credit score! Alas, it often doesn't work that way.

BUT! (There's always a "but," isn't there?) Just because they don't routinely report, doesn't mean they never do. Ah-ha! Gotcha!

When Utilities Can Affect Your Credit Score

Okay, so here's the kicker. While your consistent, on-time payments are often ignored (rude!), a late or unpaid utility bill? Oh, honey, that can absolutely ding your credit. It's like they only notice you when you mess up. So unfair!

How does this happen, you ask? Glad you did! If you fail to pay your utility bill for a significant period (think months, not just a few days - we all forget sometimes!), the utility company might send your debt to a collection agency.

And guess what? Collection agencies absolutely report to credit bureaus. Cue the dramatic music! A collection account on your credit report? Not good. It's like showing up to a fancy party in your pajamas. Not the vibe.

So, the process usually looks like this: You miss a payment (oops!). You miss another (getting serious now!). You ignore the scary letters (don't do this!). The utility company gets fed up and sells your debt to a collection agency (uh oh!). The collection agency reports it to the credit bureaus (credit score: going down, down, down!).

Think of it like this: On-time payments are invisible ninjas. Late payments are blaring sirens with flashing lights. Which one do you think is going to get noticed?

What Can You Do?

Alright, alright, enough doom and gloom! What can you actually do to make sure your utility payments aren't silently sabotaging your credit?

1. Pay On Time (Duh!): Okay, this one's obvious, but seriously. Set up autopay! It's a lifesaver. Think of your future self thanking you. Future you will be SO proud.

2. Credit Reporting Services: There are now services popping up that allow you to report your utility payments to credit bureaus. Think of it as finally getting credit for being responsible! Do some research and see if one of these is right for you. They may charge a small monthly fee, but it could be worth it if you are building your credit!

3. Communicate!: If you're struggling to pay, contact the utility company immediately. They might have payment plans or assistance programs available. Ignoring the problem won't make it go away, trust me. It'll just fester like that week-old broccoli in the back of your fridge.

4. Regularly Check Your Credit Report: Seriously, do this! At least once a year. You're entitled to a free credit report from each of the three major bureaus annually. Catching errors early can save you a major headache (and potentially boost your credit score!).

5. Experian BoostTM: Experian offers a program called BoostTM that allows you to link your bank accounts and get credit for paying certain bills (including utilities!) on time. It's worth looking into if you want that extra credit score bump! It's like a little cheat code for your credit score!

So, there you have it! The somewhat murky world of utilities and credit scores. The key takeaway? Always pay your bills on time, communicate if you're struggling, and keep an eye on your credit report. Now go forth and conquer your financial goals! And maybe treat yourself to a celebratory latte. You deserve it!

Disclaimer: I'm just your friendly neighborhood internet advice-giver, not a financial expert. Always consult with a qualified professional for personalized financial advice.