Consolidated Statement Of Operations Vs Income Statement

Alright, let's talk about something that might sound intimidating, but trust me, it's actually quite useful – understanding the difference between a Consolidated Statement of Operations and a regular Income Statement. Now, I know what you're thinking: "Finance? Fun?" But stick with me! Knowing this stuff can be surprisingly empowering, whether you're trying to understand a company's performance, managing your family budget like a pro, or even just keeping track of your side hustle's profits.

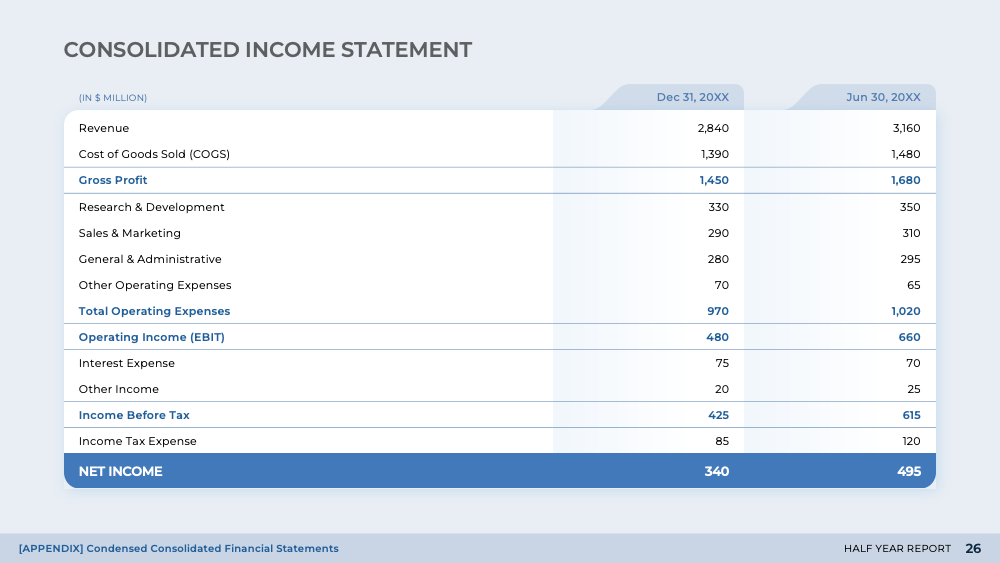

So, what are these statements, and why should you care? At its core, both the Consolidated Statement of Operations and the Income Statement show a company's financial performance over a specific period, usually a quarter or a year. They both tell you how much revenue the company generated, how much it cost to generate that revenue, and ultimately, how much profit (or loss) the company made. They both follow a similar formula: Revenue - Expenses = Profit (or Loss). The goal is to see that bottom line! They provide a snapshot of profitability.

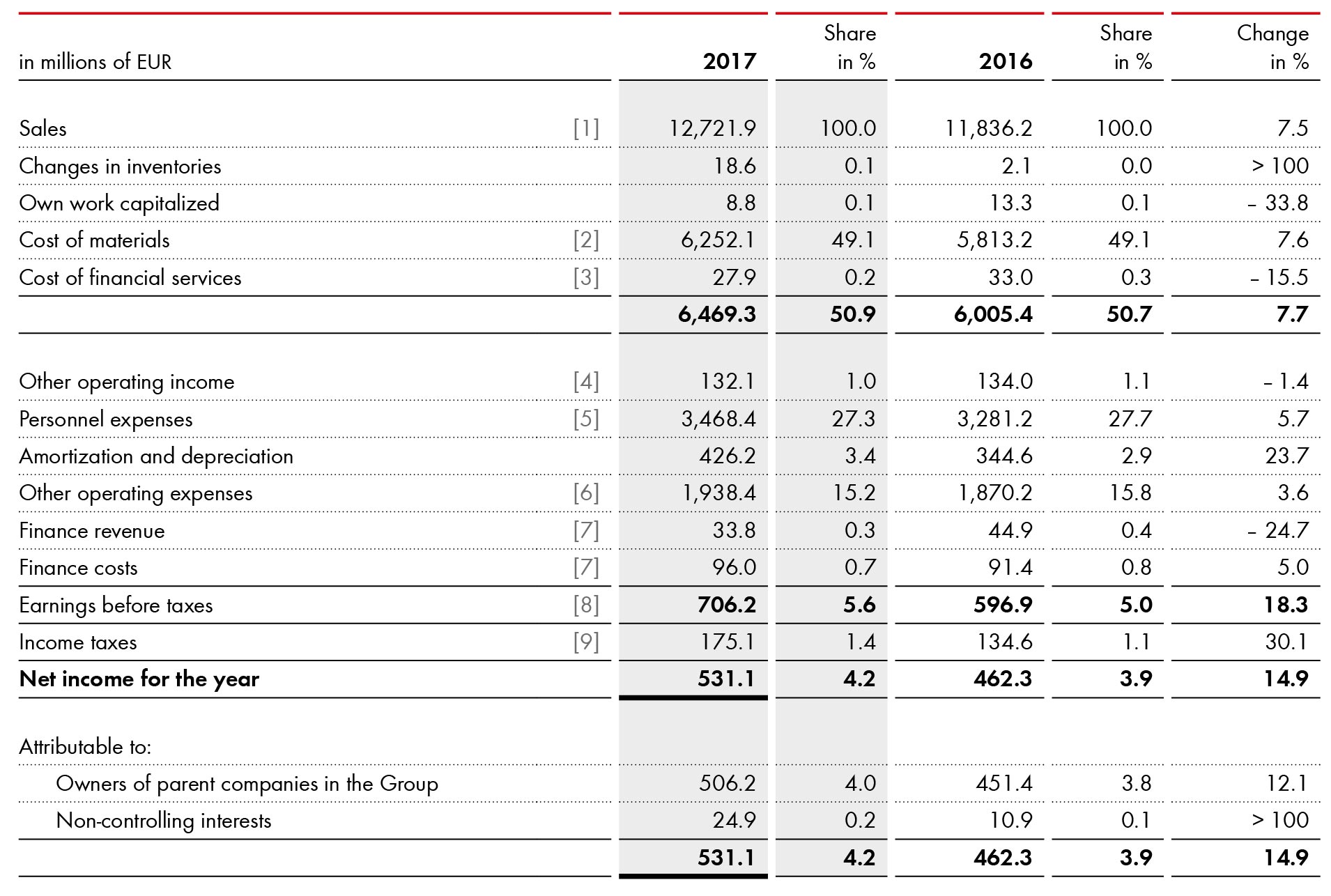

The key difference lies in the word "Consolidated." A regular Income Statement focuses on a single, individual company. A Consolidated Statement of Operations, on the other hand, shows the financial performance of a parent company and all its subsidiaries as if they were one big entity. Think of it like this: If Disney just had the one theme park in California, their income statement would show only those revenues and expenses. But Disney owns Pixar, Marvel, ABC, ESPN, and many other companies. Their Consolidated Statement of Operations shows the combined performance of all of these, giving investors a complete picture of the entire Disney empire.

Must Read

Why is this important for different audiences? For beginners learning about finance, understanding the basic Income Statement is crucial. It's the foundation for understanding more complex financial reports. For families trying to manage their budget, think of your household as a small company. Tracking your income (salary, investments) and expenses (rent, groceries, entertainment) in a simple income statement format can reveal areas where you can save money. For hobbyists with side hustles, like selling crafts online or offering freelance services, creating a basic income statement helps you track your profitability and see if your hobby is actually making you money or just costing you more in supplies.

Examples and Variations: A simplified income statement might just show total revenue and total expenses. A more detailed one might break down revenues by product line and expenses by category (cost of goods sold, marketing, administrative costs). The consolidated statement will also need to include an important item called non-controlling interest which is the portion of a subsidiary's equity not owned by the parent company. For example, let's say Disney acquired Marvel for 90% ownership. The remaining 10% is non-controlling interest.

Practical Tips for Getting Started: Don't be afraid to start small. You can easily create a simple income statement in a spreadsheet program like Excel or Google Sheets. Just create columns for income, expenses, and profit/loss. For larger companies, you'll find their financial statements on their investor relations website or the SEC's EDGAR database. If you're analyzing a company, pay attention to trends over time. Is revenue growing? Are expenses under control? For families, there are many budgeting apps that automate the process.

Ultimately, understanding these statements isn't just about numbers; it's about gaining control and making informed decisions. Whether it's figuring out if your side hustle is viable, optimizing your family budget, or evaluating a potential investment, a little financial literacy can go a long way. So, dive in, explore the numbers, and unlock the power of understanding your financial landscape! It's more rewarding than you might think!