Hey there, future millionaire (or at least, someone planning for the future)! Let's talk about something that might sound a bit dry: LIC's New Endowment Plan surrender value. But trust me, we'll make it fun. Think of it as unlocking a secret level in your financial game.

So, you've got an LIC New Endowment Plan, that’s awesome! It's like a responsible adult badge. But sometimes, life throws you curveballs, right? Maybe that dream trip to Bali suddenly needs funding, or you found the *perfect* vintage car (priorities, people!). That’s where understanding the surrender value comes in.

What's a "Surrender Value" Anyway?

Basically, it's the amount of money you get back if you decide to cash out your policy *before* it matures. Think of it like breaking a piggy bank – you get the coins inside, but you might lose out on some potential future interest. It's not ideal, but sometimes, it's necessary.

Now, LIC (Life Insurance Corporation of India, for those playing at home) doesn’t just hand over your entire premium amount if you surrender early. There's a formula, and it involves a bit of wizardry (okay, not really wizardry, but it can feel like it sometimes!).

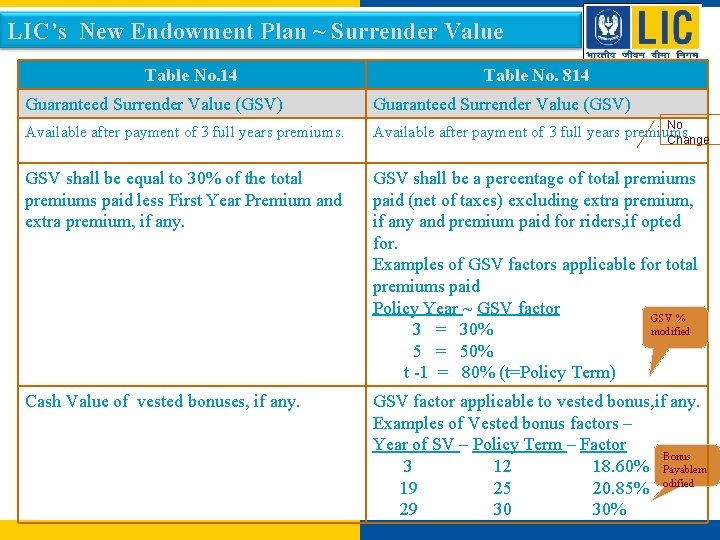

The Two Types of Surrender Values: Guaranteed and Special

There are two main types of surrender values you'll encounter:

- Guaranteed Surrender Value (GSV): This is like the minimum amount you’re *guaranteed* to receive. It's usually a percentage of the total premiums you've paid, minus any bonuses you might have received. Typically, you get this only after paying premiums for at least three full years. Think of it as a "thank you for sticking with us for a bit" kind of deal.

- Special Surrender Value (SSV): This one's a bit trickier. The SSV is usually *higher* than the GSV, especially if you surrender closer to the maturity date. But, and this is a big but, it depends on the policy's performance, the premiums paid, and a bunch of other factors that LIC keeps close to its chest (not really, they're in the fine print!). Calculating this yourself? Good luck! (Just kidding… mostly.)

Important Note: Early surrender almost always means losing money. So, only do it if you *really* need to. Think of it as using your emergency fund – for true emergencies only!

How to Find Out Your Plan's Surrender Value?

Okay, so you're seriously considering surrendering. Here's how to get the numbers:

- Your Policy Document: Dust off that thick policy document! The details about surrender values should be in there, usually in the fine print. Prepare for some serious reading!

- LIC Branch: Head to your nearest LIC branch. The folks there can help you calculate the surrender value based on your specific policy details. Just be prepared to wait in line – bring a good book!

- LIC Website/App: Some policies allow you to check the surrender value online through LIC's website or app. This is usually the easiest and fastest option. Technology for the win!

Pro-Tip: Always, *always* compare the surrender value with the premiums you've already paid. This will give you a clear picture of how much you're potentially losing. It might make you reconsider that vintage car (maybe… maybe not!).

Factors Affecting the Surrender Value

So, what influences how much you get back?

- Policy Term: Longer policies tend to have a lower surrender value in the early years. It's like planting a tree – it takes time for it to grow and bear fruit (or, in this case, financial benefits).

- Premiums Paid: The more premiums you've paid, the higher the surrender value. Seems logical, right?

- Bonuses Declared: If your policy has accumulated bonuses, these will be factored into the SSV. More bonuses, more money!

- Timing of Surrender: Surrendering closer to the maturity date generally results in a higher surrender value (especially the SSV). Patience is a virtue, my friend.

Important Reminder: Surrendering your policy means you lose the life cover that it provides. So, consider if you have alternative insurance arrangements in place before making a decision. Don't leave yourself financially vulnerable!

Before You Surrender: Consider Alternatives!

Look, surrendering should be a last resort. Before you pull the trigger, explore other options:

- Policy Loan: You can often take a loan against your policy. This allows you to access funds without completely surrendering the policy. It's like borrowing from yourself – just remember to pay it back!

- Premium Payment Holiday: Some policies offer a premium payment holiday, where you can temporarily stop paying premiums without losing your policy. Check if your policy allows for this. It's like hitting the pause button on your financial commitments.

Seriously, talk to your LIC agent or financial advisor before surrendering. They can help you explore all your options and make the best decision for your situation. They're there to help, not just sell you stuff!

So, there you have it! The not-so-scary guide to LIC New Endowment Plan surrender values. Remember, knowledge is power, and now you're armed with the information to make informed decisions about your financial future. Go forth and conquer your financial goals (and maybe still get that vintage car… if it's responsible!).